Page 1 of 15

On February 12, 2024, the IRS released Rev. Proc. 2024-14 to provide the adjusted excise tax amounts under the Affordable Care Act’s Employer Shared Responsibility provisions (also known as the ACA Pay or Play Penalty) for 2025.

For background, employers with more than 50 full-time employees (including full-time equivalent employees) are subject to the ACA Pay or Play Penalty under Section 4980H of the Internal Revenue Code (the “Code”). Employers subject to ACA Pay or Play may be liable for a penalty if they do not offer minimum essential coverage to a sufficient number of full-time employees, or if minimum essential coverage is offered to the required number of full-time employees, but that coverage is not affordable.

2025 Adjusted Penalty Amounts

The Internal Revenue Service (IRS) recently released draft instructions for preparing, distributing and filing 2023 Forms 1094-B/C and 1095-B/C. These instructions largely mirror guidance the IRS has published in previous years, except that the electronic filing threshold has been reduced from 250 forms to 10 forms aggregate.

For 2022 filing, employers could mail their Forms 1094 and 1095 to the IRS if their submission included fewer than 250 forms. For ACA filing for 2023 and future years, employers that cumulatively submit at least 10 forms to the IRS, including W-2s, 1099s, ACA forms 1094/1095, and other common form series, the employer must now file all of those forms electronically.

For example– if you are an employer who issues five Forms W-2 for 2023, four 1095-B forms for 2023, and one 1094-B Form for 2023, this is a sum collectively of 10 total forms and this employer must file all of these forms electronically with the IRS when its due in 2024.

This change result from a final regulation the IRS issued earlier this year that officially reduced the electronic filing threshold for many forms.

Employers that have historically submitted their Forms 1094/1095 to the IRS by paper will need to consider overall how many forms they will be filing with the IRS (not just Forms 1094/1095) in 2024 to determine whether they can continue to file via paper. Even if your carrier prepares you with paper copies of your 1094/1095 forms as a courtesy for submission to the IRS, you will still need to evaluate if you need to file those electronically in 2024.

Ultimately the 10 form aggregate threshold will necessitate electronic filing for nearly every employer. Anyone who has traditionally paper filed their ACA forms to consider contracting with a vendor or speak with their payroll company to see if they can confidentially e-File on their behalf in 2024.

The IRS guidance regarding the filing threshold is available online at https://www.govinfo.gov/content/pkg/FR-2023-02-23/pdf/2023-03710.pdf

The IRS has released Revenue Procedure 2023-34 confirming that for plan years beginning on or after January 1, 2024, the health FSA salary reduction contribution limit will increase to $3,200.

The adjustment for 2024 represents a $150 increase to the current $3,050 health FSA salary reduction contribution limit in 2023.

What About the Carryover Limit into 2025?

The indexed carryover limit for plan years starting in calendar year 2024 to a new plan year starting in calendar year 2025 will increase to $640.

Other Notable 2024 Health and Welfare Employee Benefit Amounts

The IRS recently issued Revenue Procedure 2023-29, which significantly decreases the affordability threshold for ACA employer mandate purposes to 8.39% for plan years beginning in 2024. The new 8.39% level marks by far the lowest affordability percentage to date.

The affordability percentages apply for plan years beginning in the listed year. A calendar plan year will therefore have the 8.39% affordability threshold for the plan year beginning January 1, 2024.

The ACA employer mandate rules apply to employers that are “Applicable Large Employers,” or “ALEs.” In general, an employer is an ALE if it (along with any members in its controlled group) employed an average of at least 50 full-time employees, including full-time equivalent employees, on business days during the preceding calendar year.

There are two potential ACA employer mandate penalties that can impact ALEs:

a) IRC §4980H(a)—The “A Penalty”

The first is the §4980H(a) penalty—frequently referred to as the “A Penalty” or the “Sledge Hammer Penalty.” This penalty applies where the ALE fails to offer minimum essential coverage to at least 95% of its full-time employees in any given calendar month.

The 2024 A Penalty is $2,970 annualized multiplied by all full-time employees (reduced by the first 30). It is triggered by at least one full-time employee who was not offered minimum essential coverage enrolling in subsidized coverage on the Exchange.

The “A Penalty” liability is focused on whether the employer offered a major medical plan to a sufficient percentage of full-time employees—not whether that offer was affordable (or provided minimum value).

b) IRC §4980H(b)—The “B Penalty”

The second is the §4980H(b) penalty—frequently referred to as the “B Penalty or the “Tack Hammer Penalty.” This penalty applies where the ALE is not subject to the A Penalty (i.e., the ALE offers coverage to at least 95% of full-time employees).

The B Penalty applies for each full-time employee who was:

Only those full-time employees who enroll in subsidized coverage on the Exchange will trigger the B Penalty. Unlike the A Penalty, the B Penalty is not multiplied by all full-time employees.

In other words, an ALE who offers minimum essential coverage to a full-time employee will be subject to the B Penalty if:

The 2024 B Penalty is $4,460 annualized per full-time employee receiving subsidized coverage on the Exchange.

On February 21, 2023, the IRS released Final Rules amending the existing requirements related to mandatory e-filing of information returns, including Forms 1094-C and 1095-C, among others. The final rules are effective for all applicable returns due on or after January 1, 2024. While the final rule requires electronic filing for a number of different information returns, such as Forms W-2 and 1099, which were previously allowed to be paper filed by employers of a certain size, this alert addresses the changes applicable to Forms 1094 and 1095, which must be filed by applicable large employers (ALEs) as well as non-ALEs that sponsor self-funded health plans.

Under the final rules, employers filing 10 or more returns must file Forms 1094 and 1095 (and their other applicable returns) electronically. The 10-form threshold is determined based on the total number of forms the employer must file with the IRS, including the Forms 1094 and 1095, as well as other information returns, such as Forms W-2 and Forms 1099, income tax returns, excise tax returns, and employment tax returns, including those that are not required to be e-filed, such as forms 940 and 941. Previously, employers that filed less than 250 of the same ACA reporting forms were allowed to choose whether to file their applicable Forms 1094 and 1095 (either the B or C forms, as applicable) by paper or electronically.

The final rules allow employers to seek a waiver in cases of undue hardship. Per the final rules, a key factor in determining whether hardship exists is whether the cost for filing the returns electronically exceeds the cost of filing the return on paper. Entities seeking a waiver must specify the type of filing to which the waiver applies, the period to which it applies, and the entity must follow any applicable procedures, publications, forms, instructions, or other guidance, including postings to the IRS.gov website, when requesting the waiver. Further, the final rules allow the IRS to grant exemptions from the requirements in certain instances.

All ALEs and many non-ALEs (that report due to sponsoring a self-funded health plan) will be impacted by these changes and will be required to file their tax year 2023 Forms 1094 and 1095 electronically unless they seek and are granted a hardship exception by the IRS. Impacted entities should take the time between now and next year to engage a filing vendor that can assist them with their electronic filing obligations.

On February 23, 2023, the Departments of Labor, Health and Human Services and the Treasury (Departments) issued FAQs on the prohibition of gag clauses under the transparency provisions of the Consolidated Appropriations Act, 2021 (CAA). These FAQs require health plans and health insurance issuers to submit their first attestation of compliance with the CAA’s prohibition on gag clauses by December 31, 2023.

Effective December 27, 2020, the CAA forbids health plans and issuers from entering into contracts with health care providers, third-party administrators (TPAs) or other service providers that would restrict the plan or issuer from providing, accessing or sharing certain information about provider price and quality and deidentified claims.

Plans and issuers must annually submit an attestation of compliance with these requirements to the Departments. The first attestation is due by December 31, 2023, covering the period beginning December 27, 2020, through the date of attestation. Subsequent attestations, covering the period since the last attestation, are due by December 31 of each following year.

Employers should ensure any contracts with TPAs or other health plan service providers offering access to a network of providers do not violate the CAA’s prohibition of gag clauses. Additionally, employers with fully insured or self-insured health plans should prepare to provide the compliance attestation by December 31, 2023. If the issuer for a fully insured health plan provides the attestation, the plan does not also need to provide an attestation. Also, employers with self-insured health plans can enter into written agreements with their TPAs to provide the attestation, but the legal responsibility remains with the health plan.

A gag clause is a contractual term that directly or indirectly restricts specific data and information that a health plan or issuer can make available to another party. Effective December 27, 2020, the CAA generally prohibits group health plans and issuers offering group health insurance from entering into agreements with health care providers, TPAs or other service providers that include certain gag clause language. Specifically, these contracts cannot restrict a plan or issuer from:

For example, if a contract between a TPA and a health plan provides that the plan sponsor’s access to provider-specific cost and quality-of-care information is only at the discretion of the TPA, that contractual provision would be considered a prohibited gag clause.

Plans and issuers must ensure their agreements with health care providers, networks or associations of providers, TPAs or other service providers offering access to a network of providers do not contain provisions that violate the CAA’s prohibition on gag clauses.

Health plans and issuers must annually submit an attestation of their compliance with the CAA’s prohibition on gag clauses to the Departments. The first attestation must be submitted no later than December 31, 2023, covering the period beginning December 27, 2020, through the date of the attestation. Subsequent attestations are due by December 31 of each following year, covering the period since the last attestation.

According to the Departments’ FAQs, health plans and issuers that do not submit their attestations by the deadline may be subject to enforcement action.

The attestation requirement applies to fully insured and self-insured group health plans, including ERISA plans, non-federal governmental plans and church plans. Additionally, this requirement applies regardless of whether a plan is considered “grandfathered” under the ACA. However, plans that only provide excepted benefits and account-based plans, such as health reimbursement arrangements (HRAs), are not required to submit an attestation.

With respect to fully insured group health plans, the health plan and the issuer are each required to submit a gag clause compliance attestation annually. However, when the issuer of a fully insured group health plan submits a gag clause compliance attestation on behalf of the plan, the Departments will consider the plan and issuer to have satisfied the attestation submission requirement.

Employers with self-insured health plans can satisfy the gag clause compliance attestation requirement by entering into a written agreement under which the plan’s service provider, such as a TPA, will provide the attestation on the plan’s behalf. However, even if this type of agreement is in place, the legal requirement to provide a timely attestation remains with the health plan.

The Departments launched a website through the Centers for Medicare and Medicaid Services for health plans and issuers to submit their gag clause compliance attestations. The Departments have also provided instructions for submitting the attestation, a system user manual, and a reporting entity Excel template for plans and issuers to submit the required attestation, all of which are available here.

On October 11, 2022, the IRS released a final rule that changes the way health insurance affordability is determined for members of an employee’s family, beginning with Plan Year (PY) 2023 coverage. Beginning in 2023, if a employee has an offer of employer-sponsored coverage that extends to the employee’s family members, the affordability of that offer of coverage for the family members will be based on the family premium amount, not the amount the employee must pay for self-only coverage, when purchasing coverage in the marketplace.

To view the final rule, visit: https://www.federalregister.gov/public-inspection/2022-22184/affordability-of-employer-coverage-for-family-members-of-employees

There are two potential ACA employer mandate penalties that can impact ALEs:

a) IRC §4980H(a)—The “A Penalty”

The first is the §4980H(a) penalty—frequently referred to as the “A Penalty” or the “Sledge Hammer Penalty.” This penalty applies where the ALE fails to offer minimum essential coverage to at least 95% of its full-time employees in any given calendar month.

The 2022 A Penalty is $229.17/month ($2,750 annualized) multiplied by all full-time employees (reduced by the first 30). It is triggered by at least one full-time employee who was not offered minimum essential coverage enrolling in subsidized coverage on the Exchange. Note: The IRS has not yet released the 2023 A Penalty increase.

The “A Penalty” liability is focused on whether the employer offered a major medical plan to a sufficient percentage of full-time employees—not whether that offer was affordable (or provided minimum value).

b) IRC §4980H(b)—The “B Penalty”

The second is the §4980H(b) penalty—frequently referred to as the “B Penalty or the “Tack Hammer Penalty.” This penalty applies where the ALE is not subject to the A Penalty (i.e., the ALE offers coverage to at least 95% of full-time employees).

The B Penalty applies for each full-time employee who was:

Only those full-time employees who enroll in subsidized coverage on the Exchange will trigger the B Penalty. Unlike the A Penalty, the B Penalty is not multiplied by all full-time employees.

In other words, an ALE who offers minimum essential coverage to a full-time employee will be subject to the B Penalty if:

The 2022 B Penalty is $343.33/month ($4,120 annualized) per full-time employee receiving subsidized coverage on the Exchange. Note: The IRS has not yet released the 2023 B Penalty increase.

Transparency in Coverage mandates and COVID-19 considerations continue to dominate the discussion in the employee benefits compliance space this summer, but an “old faithful” reporting requirement looms soon: the Patient-Centered Outcomes Research Institute (PCORI) filing and fee. The Affordable Care Act imposes this annual per-enrollee fee on insurers and sponsors of self-funded medical plans to fund research into the comparative effectiveness of various medical treatment options.

The typical due date for the PCORI fee is July 31, but because that date falls on a Sunday in 2022, the effective due date is pushed to the next business day, which is Aug. 1.

The filing and payment due by Aug. 1, 2022, is required for policy and plan years that ended during the 2021 calendar year. For plan years that ended Jan. 1, 2021 – Sept. 30, 2021, the fee is $2.66 per covered life. For plan years that ended Oct. 1, 2021 – Dec. 31, 2021 (including calendar year plans that ended Dec. 31, 2021), the fee is calculated at $2.79 per covered life.

Insurers report on and pay the fee for fully insured group medical plans. For self-funded plans, the employer or plan sponsor submits the fee and accompanying paperwork to the IRS. Third-party reporting and payment of the fee (for example, by the self-insured plan sponsor’s third-party claim payor) is not permitted.

An employer that sponsors a self-insured health reimbursement arrangement (HRA) along with a fully insured medical plan must pay PCORI fees based on the number of employees (dependents are not included in this count) participating in the HRA, while the insurer pays the PCORI fee on the individuals (including dependents) covered under the insured plan. Where an employer maintains an HRA along with a self-funded medical plan and both have the same plan year, the employer pays a single PCORI fee based on the number of covered lives in the self-funded medical plan and the HRA is disregarded.

The IRS collects the fee from the insurer or, in the case of self-funded plans, the plan sponsor in the same way many other excise taxes are collected. Although the PCORI fee is paid annually, it is reported (and paid) with the Form 720 filing for the second calendar quarter (the quarter ending June 30). Again, the filing and payment is typically due by July 31 of the year following the last day of the plan year to which the payment relates, but this year the due date pushes to Aug. 1.

IRS regulations provide three options for determining the average number of covered lives: actual count, snapshot and Form 5500 method.

Actual count: The average daily number of covered lives during the plan year. The plan sponsor takes the sum of covered lives on each day of the plan year and divides the number by the days in the plan year.

Snapshot: The sum of the number of covered lives on a single day (or multiple days, at the plan sponsor’s election) within each quarter of the plan year, divided by the number of snapshot days for the year. Here, the sponsor may calculate the actual number of covered lives, or it may take the sum of (i) individuals with self-only coverage, and (ii) the number of enrollees with coverage other than self-only (employee-plus one, employee-plus family, etc.), and multiply by 2.35. Further, final rules allow the dates used in the second, third and fourth calendar quarters to fall within three days of the date used for the first quarter (in order to account for weekends and holidays). The 30th and 31st days of the month are both treated as the last day of the month when determining the corresponding snapshot day in a month that has fewer than 31 days.

Form 5500: If the plan offers family coverage, the sponsor simply reports and pays the fee on the sum of the participants as of the first and last days of the year (recall that dependents are not reflected in the participant count on the Form 5500). There is no averaging. In short, the sponsor is multiplying its participant count by two, to roughly account for covered dependents.

The U.S. Department of Labor says the PCORI fee cannot be paid from ERISA plan assets, except in the case of union-affiliated multiemployer plans. In other words, the PCORI fee must be paid by the plan sponsor; it cannot be paid in whole or part by participant contributions or from a trust holding ERISA plan assets. The PCORI expense should not be included in the plan’s cost when computing the plan’s COBRA premium. The IRS has indicated the fee is, however, a tax-deductible business expense for sponsors of self-funded plans.

Although the DOL’s position relates to ERISA plans, please note the PCORI fee applies to non-ERISA plans as well and to plans to which the ACA’s market reform rules don’t apply, like retiree-only plans.

The filing and remittance process to the IRS is straightforward and unchanged from last year. On Page 2 of Form 720, under Part II, the employer designates the average number of covered lives under its “applicable self-insured plan.” As described above, the number of covered lives is multiplied by the applicable per-covered-life rate (depending on when in 2021 the plan year ended) to determine the total fee owed to the IRS.

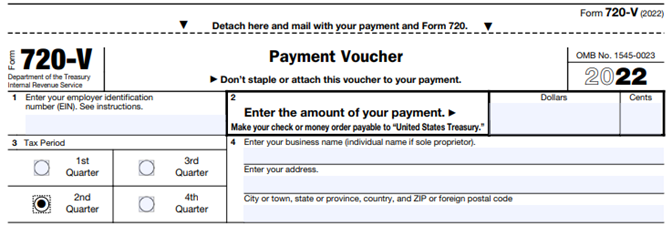

The Payment Voucher (720-V) should indicate the tax period for the fee is “2nd Quarter.”

Failure to properly designate “2nd Quarter” on the voucher will result in the IRS’ software generating a tardy filing notice, with all the incumbent aggravation on the employer to correct the matter with IRS.

An employer that overlooks reporting and payment of the PCORI fee by its due date should immediately, upon realizing the oversight, file Form 720 and pay the fee (or file a corrected Form 720 to report and pay the fee, if the employer timely filed the form for other reasons but neglected to report and pay the PCORI fee). Remember to use the Form 720 for the appropriate tax year to ensure that the appropriate fee per covered life is noted.

The IRS might levy interest and penalties for a late filing and payment, but it has the authority to waive penalties for good cause. The IRS’s penalties for failure to file or pay are described here.

The IRS has specifically audited employers for PCORI fee payment and filing obligations. Be sure, if you are filing with respect to a self-funded program, to retain documentation establishing how you determined the amount payable and how you calculated the participant count for the applicable plan year.

On April 19, 2022, the Departments of Labor, Health and Human Services, and the Treasury issued additional guidance under the Transparency in Coverage Final Rules issued in 2020. The guidance, FAQs About Affordable Care Act Implementation Part 53, provides a safe harbor for disclosing in-network healthcare costs that cannot be expressed as a dollar amount. They also serve as a timely reminder of the pending July 1, 2022, deadline to begin enforcing the Final Rules.

Background

The Final Rules require non-grandfathered health plans and health insurance issuers to post information about the cost to participants, beneficiaries, and enrollees for in-network and out-of-network healthcare services through machine-readable files posted on a public website. The Final Rules for this requirement are effective for plan years beginning on or after January 1, 2022 (an additional requirement for disclosing information about pharmacy benefits and drug costs is delayed pending further guidance). The Final Rules require that all costs be expressed as a dollar amount. After the Final Rules were published, plans and issuers pointed out that under some alternative reimbursement arrangements in-network costs are calculated as a percentage of billed charges. In those cases, dollar amounts cannot be determined in advance.

FAQ Safe Harbor

The FAQs provide a safe harbor for disclosing costs under a contractual arrangement where the plan or issuer agrees to pay an in-network provider a percentage of billed charges and cannot assign a dollar amount before delivering services. Under this kind of arrangement, they may report the percentage number instead of a dollar amount. The FAQs also provide that where the nature of the contractual arrangement requires the submission of additional information to describe the nature of the negotiated rate, plans and issuers may describe the formula, variables, methodology, or other information necessary to understand the arrangement in an open text field. This is only permitted if the current technical specifications do not support the disclosure via the machine-readable files.

Public Website Requirement

This guidance is pretty narrow and of most interest to plans, issuers, and third-party administrators responsible for the technical aspects of the disclosure. Still, it is a helpful reminder to plan sponsors that the July 1st enforcement deadline for these requirements is rapidly approaching. As a reminder, for fully insured plans the plan sponsor is considered the insurance carrier. However, for self or level funded medical plans the plan sponsor is the employer so they will be the one responsible making sure they are meeting the transparency disclosure requirements. Plans sponsors should remember that these machine-readable files must be posted on a public website. The Final Rules clearly state that the files must be accessible for free, without having to establish a user account, password, or other credentials and without submitting any personal identifying information such as a name, email address, or telephone number. If a third-party website hosts the files, the plan or issuer must post a link to the file’s location on its own public website. Simply posting the files on an individual plan website or the Plan Sponsor’s company intranet falls short of these requirements. Regardless of how a plan opts to comply, The July 1st deadline is right around the corner.