Page 2 of 2

The IRS and the Treasury Department issued a notice on the so-called “Cadillac Tax”—a 40 percent excise tax to be imposed on high-cost employer-sponsored health plans beginning in 2018 under the Affordable Care Act (ACA).

Notice 2015-16, released on Feb. 23, 2015, discusses a number of issues concerning the tax and requests comments on the possible approaches that ultimately could be incorporated in proposed regulations. Specifically, the guidance states that the agencies anticipate that pretax salary reduction contributions made by employees to health savings accounts (HSAs) will be subject to the Cadillac tax.

Background

In 2018, the ACA provides that a nondeductible 40 percent excise tax be imposed on “applicable employer-sponsored coverage” in excess of statutory thresholds (in 2018, $10,200 for self-only, $27,500 for family). As 2018 approaches, the benefit community has long awaited guidance on this tax. While many employers have actively managed their plan offerings and costs in anticipation of the impact of the tax, those efforts have been hampered by the lack of guidance. Among other things, employers are uncertain what health coverage is subject to the tax and how the tax is calculated.

Particularly, Notice 2015-16 addresses:

The agencies are requesting comments on issues

discussed in this notice by May 15, 2015. They intend to issue another notice

that will address other areas of the excise tax and anticipates issuing

proposed regulations after considering public comments on both notices.

Applicable Coverage

Of most immediate interest to plan sponsors is the specific type of coverage (i.e., “applicable coverage”) that will be subject to the excise tax, particularly where the statute is unclear.

Employee Pretax HSA

Contributions

The ACA statute provides that employer contributions to an HSA are subject to

the excise tax, but did not specifically address the treatment of employee

pretax HSA contributions. The notice says that the agencies “anticipate that

future proposed regulations will provide that (1) employer contributions to

HSAs, including salary reduction contributions to HSAs, are included in

applicable coverage, and (2) employee after-tax contributions to HSAs are

excluded from applicable coverage.”

Note: This anticipated treatment of employee pretax contributions to HSAs will have a significant impact on HSA programs. If implemented as the agencies anticipate, it could mean many employer plans that provide for HSA contributions will be subject to the excise tax as early as 2018, unless the employer limits the amount an employee can contribute on a pretax basis.

Self-Insured Dental

and Vision Plans

The ACA statutory language specifically excludes fully insured dental and

vision plans from the excise tax. The treatment of self-insured dental and

vision plans was not clear. The notice states that the agencies will consider

exercising their “regulatory authority” to exclude self-insured plans that

qualify as excepted benefits from the excise tax.

Employee Assistance

Programs

The agencies are also considering whether to exclude excepted-benefit employee

assistance programs (EAPs) from the excise tax.

Onsite Medical Clinics

The notice discusses the exclusion of certain onsite medical clinics that offer

only de

minimis care to employees,

citing a provision in the COBRA regulations, and anticipates excluding such

clinics from applicable coverage. Under the COBRA regulations an onsite clinic

is not considered a group health plan if:

The agencies are also asking for comment on

the treatment of clinics that provide certain services in addition to first

aid:

In Closing

With the release of this initial guidance, plan sponsors can gain some insight into the direction the government is likely to take in proposed regulations and can better address potential plan design strategie

Last week, the IRS issued its “final” versions of the forms 1094-B,1094-C, 1095-B and 1095-C along with instructions for the “B” forms and instructions for the “C” forms. The good news is that the forms are pretty much the same from the drafts released in mid 2014. What has changed is that the revised instructions have filled in some gaps about reporting, some of which are highlighted below:

1. Employers with 50-99 FTEs who were exempt from compliance in 2015 must still file these forms for the 2015 tax year.

2. For employers that cover non-employees (COBRA beneficiaries or retirees being most common), they can use forms 1094-B and 1095-B instead of filing out 1095-C Part III to report for those individuals.

3. With respect to reporting for employees who work for more than one employer member of a controlled group aggregated “ALE”, the employee may receive a report from each separate employer. However, the employer for whom he or she works the most hours in a given month should report for that month.

4. Under the final instructions, a full-time employee of a self-insured employer that accepts a qualifying offer and enrolls in coverage, the employer must provide that employee a 1095-C. The previous draft indicated that it would be enough to simply provide an employee a statement about the offer rather than an actual form

5. For plans that exclude spouses covered or offered health coverage through their own employers, the definition of “offer of health coverage” now provides that an offer to a spouse subject to a reasonable, objective condition is treated as an offer of coverage for reporting purposes.

6. There are some changes with respect to what days can be used to measure the “count” for reporting purposes. Employers are allowed to use the first day of the first payroll period of each month or the last day of the first payroll period of each month, as long as the last day is in the same month as when the payroll period starts. Also, an employer can report offering coverage for a month only if the employer offers coverage for every day of that month. Mid-month eligibilities would presumably be counted as being covered on the first day of the next month. However, in the case of terminations of employment mid-month, the coverage can be treated as offered for the entire month if, but for the termination, the coverage would have continued for the full month.

Now as a refresher about what needs to be filed:

Bear in mind that there is a considerable amount of time between now and the final filing obligation so there may be additional revisions to these instructions, or at least some further clarification. But in the meantime, read the instructions and familiarize yourself with the reporting obligations as well as beginning the steps to collecting the necessary data to make completing the forms next year easier.

Beginning January 1, 2015, employers have new reporting obligations for health plan coverage, to allow the government to administer the “pay or play” penalties to be assessed against employers that do not offer compliant coverage to their full-time employees.

Even though the penalties only apply if there are 100 or more employees for 2015, employers with 50 or more full-time equivalent employees are required to report for 2015. Also, note this reporting is required even if the employer does not maintain any health plan.

Employers that provide self-funded group health coverage also have reporting obligations, to allow the government to administer the “individual mandate” which results in a tax on individuals who do not maintain health coverage.

These reporting obligations will be difficult for most employers to implement. Penalties for non-compliance are high, so employers need to begin now with developing a plan on how they will track and file the required information.

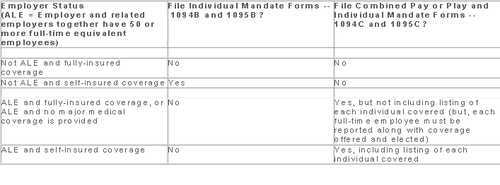

Pay or Play Reporting. Applicable large employers (ALEs) must report health coverage offered to employees for each month of 2015 in an annual information return due early in 2016. ALEs are employers with 50 or more full-time equivalent (FTE) employees. Employees who average 30 hours are counted as one, and those who average less than 30 hours are combined into an equivalent number of 30 hour employees to determine if there are 50 or more FTE employees. All employees of controlled group, or 80% commonly owned employers, are also combined to determine if the 50 FTE threshold is met.

Individual Mandate Reporting. Self-funded employers, including both ALEs and small employers that are not ALEs, must report each individual covered for each month of the calendar year. For fully-insured coverage, the insurance carrier must report individual month by month coverage. The individual mandate reporting is due early in 2016 for each month of 2015.

Which Form? ALE employers have one set of forms to report both the pay or play and the individual mandate information – Forms 1094C and 1095C. Insurers and self-insured employers that are not ALEs use Forms 1094B and 1095B to report the individual mandate information. Information about employee and individual coverage provided on these forms must also be reported by the employer to its employees as well as to COBRA and retiree participants. Forms 1095B and 1095C can be used to provide this information, or employers can provide the information in a different format.

The following chart summaries which returns are filed by employers:

Who Reports? While ALE status is determined on a controlled group basis, each ALE must file separate reports. Employers will need to provide insurance carriers, and third party administrators who process claims for self-funded coverage (if they will assist the employer with reporting), accurate data on the employer for whom each covered employee works. If an employee works for more than one ALE in a controlled group, the employer for whom the highest number of hours is worked does the reporting for that employee.

Due Date for Filing. The due date of the forms matches the due dates of Forms W-2, and employers may provide the required employee statements along with the W-2. Employee reporting is due January 31st and reporting to the IRS is due each February 28th, although the date is extended until March 31st if the forms are filed electronically. If the employer files 250 or more returns, the returns must be filed electronically. Reporting to employees can only be made electronically if the employee has specifically consented to receiving these reports electronically.

Penalties. Failure to file penalties can total $200 per individual for whom information must be reported, subject to a maximum of $3 million per year. Penalties will not be assessed for employers who make a good faith effort to file correct returns for 2015.

What Information is Required? For the pay or play reporting, each ALE must file a Form 1094C reporting the number of its full-time employees (averaging 30 hours) and total employees for each calendar month, whether the ALE is in a “aggregated” (controlled) group, a listing of the name and EIN of the top 30 other entities in the controlled group (ranked by number of full-time employees), and any special transition rules being used for pay or play penalties. ALE’s must also file a 1095C for each employee who was a full-time employee during any calendar month of the year. The 1095C includes the employee’s name, address and SSN, and month by month reporting of whether coverage was offered to the employee, spouse and dependents, the lowest premium for employee only coverage, and identification of the safe-harbor used to determine affordability. This information is used to determine pay or play penalty taxes and to verify the individuals’ eligibility for subsidies toward coverage costs on the Federal and state exchanges.

If the ALE provides self-funded coverage, the ALE must also report on the 1095C the name and SSN of each individual provided coverage for each calendar month. If an employer is not an ALE, but is self-funded, the name and SSN of each covered individual is reported on the 1095B and the 1094B is used to transmit the forms 1095B to the IRS.

A chart is available that sets out what data must be reported on each form, to help employers determine what information they need to track. Click here to access the chart.

Next Steps. Employers will need to determine how much help their insurance carrier or TPA can provide with the reporting, and then the employer’s HR, payroll and IT functions will need to work together to be sure the necessary information is being tracked and can be produced for reporting in January 2016.

The Affordable Care Act will require Applicable Large Employers (i.e. large employers subject to the employer mandate) and employers sponsoring self-insured plans to comply with new annual IRS reporting requirements. The first reporting deadline will be February 28, 2016 as to the data employers collect during the 2015 calendar year. The reporting provides the IRS with information it needs to enforce the Individual Mandate (i.e. individuals are penalized for not having health coverage) and the Employer Mandate (i.e. large employers are penalized for not offering health coverage to full-time employees). The IRS will also require employers who offer self-insured plans to report on covered individuals.

Large employers and coverage providers must also provide a written statement to each employee or responsible individual (i.e. one who enrolls one or more individuals) identifying the reported information. The written statement can be a copy of the Form.

The IRS recently released draft Forms 1094-C and 1095-C and draft Forms 1094-B and 1095-B, along with draft instructions for each form.

Which Forms Do I File?

When?

Statements to employees and responsible individuals are due annually by January 31. The first statements are due January 31, 2016.

Forms 1094-B, 1095-B, 1094-C and 1095-C are due annually by February 28 (or by March 31, if filing electronically). The first filing is due by February 28, 2016 (or March 31, 2016, if filing electronically).

Even though the forms are not due until 2016, the annual reporting will be based on data from the prior year. Employers need to plan ahead now to collect data for 2015. Many employers have adopted the Look Back Measurement Method Safe Harbor (“Safe Harbor”) to identify full-time employees under the ACA. The Safe Harbor allows employers to “look back” on the hours of service of its employees during 2014 or another measurement period. There are specific legal restrictions regarding the timing and length of the periods under the Safe Harbor, so employers cannot just pick random dates. Employers also must follow various rules to calculate hours of service under the Safe Harbor. The hours of service during the measurement period (which is likely to include most of 2014) will determine whether a particular employee is full-time under the ACA during the 2015 stability period. The stability period is the time during which the status of the employee, as full-time or non-full-time, is locked in. In 2016, employers must report their employees’ full-time status during the calendar year of 2015. Therefore, even though the IRS forms are not due until 2016, an employee’s hours of service in 2014 will determine how an employer reports that employee during each month of 2015. Employers who have not adopted the Safe Harbor should consider doing so because it allows an employer to average hours of service over a 12-month period to determine the full-time status of an employee. If an employer does not adopt the Safe Harbor, the IRS will require the employer to make a monthly determination, which is likely to increase an employer’s potential exposure to penalties.

What Must the Employer Report?

Form 1095-C

There are three parts to Form 1095-C. An applicable large employer must file one Form 1095-C for each full-time employee. If the applicable large employer sponsors self-insured health plans, it must also file Form 1095-C for any employee who enrolls in coverage regardless of the full-time status of that employee.

Form 1095-C requires the employer to identify the type of health coverage offered to a full-time employee for each calendar month, including whether that coverage offered minimum value and was affordable for that employee. Employers must use a code to identify the type of health coverage offered and applicable transition relief.

Employers that offer self-insured health plans also must report information about each individual enrolled in the self-insured health plan, including any full-time employee, non-full-time employee, employee family members, and others.

Form 1094-C

Applicable large employers use Form 1094-C as a transmittal to report employer summary information and transmit its Forms 1095-C to the IRS. Form 1094-C requires employers to enter the name and contact information of the employer and the total number of Forms 1095-C it submits. It also requires information about whether the employer offered minimum essential coverage under an eligible employer-sponsored plan to at least 95% of its full-time employees and their dependents for the entire calendar year, the number of full-time employees for each month, and the total number of employees (full-time or non-full-time) for each month.

Form 1095-B

Employers offering self-insured coverage use Form 1095-B to report information to the IRS about individuals who are covered by minimum essential coverage and therefore are not liable for the individual shared responsibility payment. These employers must file a Form 1095-B for eachindividual who was covered for any part of the calendar year. The employer must make reasonable efforts to collect social security numbers for covered individuals.

Form 1094-B

Employers who file Form 1095-B will use Form 1094-B as a transmittal form. It asks for the name of the employer, the employer’s EIN, and the name, telephone number, and address of the employer’s contact person.

Failure to Report – What Happens?

The IRS will impose penalties for failure to timely provide correct written statements to employees. The IRS will also impose penalties for failure to timely file a correct return. For the 2016 reporting on 2015 data, the IRS will not impose a penalty for good faith compliance. However, the IRS specified that good faith compliance requires that employers provide the statements and file the returns.

Small businesses may participate in several federally facilitated Small Business Health Option Program (SHOP) exchanges – for example, if an employer has offices in different states – but each small employer is limited to establishing one FF-SHOP account per state.

If an employer has worksites in several states, it may (1) establish an account in each state where the company has a primary work location for workers; or (2) it may establish an account in one state and use that to provide health insurance for all members of the group. If it does establish accounts in several states, it must submit a separate report on the participation rate to each FF-SHOP.

An employer is considered to be a small employer eligible for SHOP coverage if its average number of employees is 50 or fewer. Employers participating in the FF-SHOP must offer coverage to all full-time employees, defined as those working 30 or more hours per week on average.

The SHOP system is a way for employers to help satisfy health reform’s mandate for individuals to obtain coverage or pay extra taxes. Furthermore, most (34 out of 50, not including the District of Columbia) states will house (but not run) FF-SHOP exchanges.

In March 2013, the CMS released final rules that described the 70% participation requirement for small employers. Under those rules, insurers may deny coverage to small employers that fail to meet the minimum participation requirements.

Minimum Participation

Insurers may impose a 70% workforce participation requirement for small employers to partake in FF-SHOP coverage. In the first open enrollment period (Nov. 15 through Dec. 15, 2013), however, workers can obtain coverage on an interim basis even if an employer falls below the minimum participation amount, according to CMS. On renewal one year later, however, insurers will be able to invoke the participation requirement. State law may impose a different minimum participation requirement. Small employers are required to keep records of coverage held by workers to substantiate minimum participation and to ensure that workers do not have double coverage.

Other Highlights

Here are a few other policies small employers will want to know when considering group coverage with an FF-SHOP:

On June 26, 2013, the US Supreme Court declared the Defense of Marriage Act (DOMA) as unconstitutional. DOMA had previously established the federal definition of marriage as a legal union only between one man and one woman. The extinction of DOMA already has HR departments thinking how this will impact the future of the Family and Medical Leave Act (FMLA) as well as other benefits.

How FMLA is Impacted

As we know, the FMLA allows otherwise eligible employees to take leave to care for a family member with a serious health condition. “Family member” includes the employee’s spouse, which, under the FMLA regulations, is defined as:

a husband or wife as defined or recognized under State law for purposes of marriage in the State where the employee resides, including common law marriage in States where it is recognized. 29 C.F.R. 825.102

Initially, this seems to suggest that the DOL would look to state law to define “spouse”…but not so fast. According to a 1998 Department of Labor opinion letter, the DOL acknowledged that the FMLA was bound by DOMA’s definition that “spouse” could only be a person of the opposite sex who is a husband or wife. Thus, the DOL has taken the position that only DOMA’s definitions could be recognized for FMLA leave purposes. As a result, FMLA leave has not been made available to same-sex spouses.

That changes yesterday, at least in part.

What’s Clear about FMLA After the Ruling

In striking down a significant part of DOMA, the Supreme Court cleared the way for each state to decide its own definition of “spouse”. Thus, if an employee is married to a same-sex partner and lives in a state that recognizes same-sex marriage, the employee will be entitled to take FMLA leave to care for his/her spouse who is suffering from a serious health condition, for military caregiver leave, or to take leave for a qualifying exigency when a same-sex spouse is called to active duty in a foreign country while in the military.

What’s Unclear about FMLA After the Ruling

But what about employees who live in a state that does not recognize same-sex marriage? Are they entitled to FMLA leave to care for their spouses?

As an initial matter, the regulations look to the employee’s “place of domicile” (aka state of primary residence) to determine whether a person is a spouse for purposes of FMLA. Therefore, even if the employee formerly lived or was married in a state that recognized the same-sex marriage, he/she is unlikely to be considered a spouse in the “new” state for purposes of FMLA if the state does not recognize the marriage. This is no small issue, since 30+ states currently do not recognize same-sex marriage and some don’t go all the way (e.g. Illinois, which recognizes same-sex unions, not marriages).

Surely, some might argue that the U.S. Constitution requires other states to recognize the marriage; however, this issue is far from settled. Clearly employers need some help from the DOL. It is speculated that the DOL may draft regulations on how employers can administer FMLA in situations where the employee’s spouse is not recognized under state law. This would give life to concepts such as a “State of Celebration” rule, in which a spousal status is determined based on the law of the State where the employee was married and not where they reside. However, without more guidance, it is still too early to tell how the DOL will handle this.

Other Key Benefits Affected by the DOMA Decision

FMLA is not the only federal law impacted by the fall of DOMA. If federal regulations follow through, some of the notable federal laws and benefits impacted may include:

A provision of Health Care Reform requires employers to provide a notice to all employees regarding the availability of health coverage options through the state-based exchanges. The Department of Labor delayed the original requirement that the notice be distributed by March 1, 2013, as it was determined that there was not enough information regarding exchange availability.

The DOL recently issued temporary guidance along with a model notice. The DOL has issued the model notice early so employers can begin informing their employees now about the upcoming coverage options through the marketplace.

Two model notices were released by the DOL. One is for employers who currently offer medical coverage and the other is for those who do not offer medical coverage.

Employers are required to issue the exchange coverage notice no later than October 1, 2013. This will coincide with the beginning of the open enrollment period for the marketplace.

The notice must be provided to all employees, regardless of their enrollment on the group health plan. It must be provided to both full time and part time employees as well. Employers are not required to provide a separate notice to dependents. Employers will need to provide the notice to each new employee (regardless of their status) who are hired on or after October 1, 2013 within 14 days of their hire.

An exchange coverage notice must include –

The DOL also modified its model COBRA election notice to include information about the availability of exchange coverage options and eliminate certain obsolete language in the earlier model.

Please contact our office for a copy of the model notice(s).