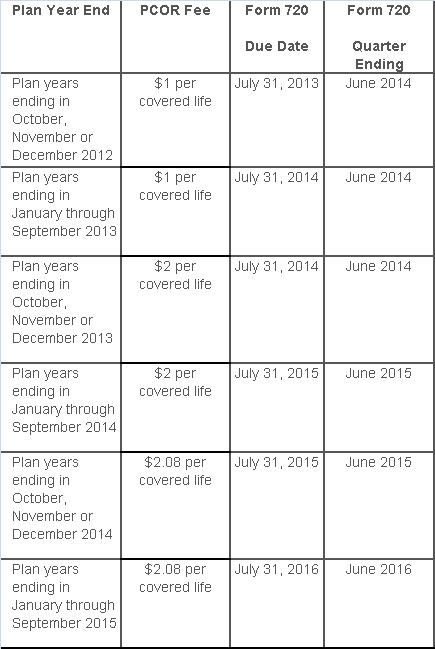

The Affordable Care Act added a patient-centered outcomes research (PCOR) fee on health plans to support clinical effectiveness research. The PCOR fee applies to plan years ending on or after Oct. 1, 2012, and before Oct. 1, 2019. The PCOR fee is due by July 31 of the calendar year following the close of the plan year. For plan years ending in 2014, the fee is due by July 31, 2015.

PCOR fees are required to be reported annually on Form 720, Quarterly Federal Excise Tax Return, for the second quarter of the calendar year. The due date of the return is July 31. Plan sponsors and insurers subject to PCOR fees but not other types of excise taxes should file Form 720 only for the second quarter, and no filings are needed for the other quarters. The PCOR fee can be paid electronically or mailed to the IRS with the Form 720 using a Form 720-V payment voucher for the second quarter. According to the IRS, the fee is tax-deductible as a business expense.

The PCOR fee is assessed based on the number of employees, spouses and dependents that are covered by the plan. The fee is $1 per covered life for plan years ending before Oct. 1, 2013, and $2 per covered life thereafter, subject to adjustment by the government. For plan years ending between Oct. 1, 2014, and Sept. 30, 2015, the fee is $2.08. The Form 720 instructions are expected to be updated soon to reflect this increased fee.

This chart summarizes the fee schedule based on the plan year end and shows the Form 720 due date. It also contains the quarter ending date that should be reported on the first page of the Form 720 (month and year only per IRS instructions). The plan year end date is not reported on the Form 720.

For insured plans, the insurance company is responsible for filing Form 720 and paying the PCOR fee. Therefore, employers with only fully- insured health plans have no filing requirement.

If an employer sponsors a self-insured health plan, the employer must file Form 720 and pay the PCOR fee. For self-insured plans with multiple employers, the named plan sponsor is generally required to file Form 720. A self-insured health plan is any plan providing accident or health coverage if any portion of such coverage is provided other than through an insurance policy.

Since the fee is a tax assessed against the plan sponsor and not the plan, most funded plans subject to ERISA must not pay the fee using plan assets since doing so would be considered a prohibited transaction by the U.S. Department of Labor (DOL). The DOL has provided some limited exceptions to this rule for plans with multiple employers if the plan sponsor exists solely for the purpose of sponsoring and administering the plan and has no source of funding independent of plan assets.

Plans sponsored by all types of employers, including tax-exempt organizations and governmental entities, are subject to the PCOR fee. Most health plans, including major medical plans, prescription drug plans and retiree-only plans, are subject to the PCOR fee, regardless of the number of plan participants. The special rules that apply to Health Reimbursement Accounts (HRAs) and Health Flexible Spending Accounts (FSAs) are discussed below.

Plans exempt from the fee include:

If a plan sponsor maintains more than one self-insured plan, the plans can be treated as a single plan if they have the same plan year. For example, if an employer has a self-insured medical plan and a separate self-insured prescription drug plan with the same plan year, each employee, spouse and dependent covered under both plans is only counted once for purposes of the PCOR fee.

The IRS has created a helpful chart showing how the PCOR fee applies to common types of health plans.

Health Reimbursement Accounts (HRAs) - Nearly all HRAs are subject to the PCOR fee because they do not meet the conditions for exemption. An HRA will be exempt from the PCOR fee if it provides benefits only for dental or vision expenses, or it meets the following three conditions:

Health Flexible Spending Accounts (FSAs) - A health FSA is exempt from the PCOR fee if it satisfies an availability condition and a maximum benefit condition.

Additional special rules for HRAs and FSAs . Once an employer determines that its HRA or FSA is subject to the PCOR fee, the employer should consider the following special rules:

The IRS provides different rules for determining the average number of covered lives (i.e., employees, spouses and dependents) under insured plans versus self-insured plans. The same method must be used consistently for the duration of any policy or plan year. However, the insurer or sponsor is not required to use the same method from one year to the next.

A plan sponsor of a self-insured plan may use any of the following three

methods to determine the number of covered lives for a plan year:

1. Actual count method. Count the covered lives on each day of the plan year and divide by the number of days in the plan year.

Example: An employer has 900 covered lives on Jan. 1, 901 on Jan. 2, 890 on

Jan. 3, etc., and the sum of the lives covered under the plan on each day of

the plan year is 328,500. The average number of covered lives is 900 (328,500 ÷

365 days).

2. Snapshot method. Count the covered lives on a single day in each quarter (or more than one day) and divide the total by the number of dates on which a count was made. The date or dates must be consistent for each quarter. For example, if the last day of the first quarter is chosen, then the last day of the second, third and fourth quarters should be used as well.

Example: An employer has 900 covered lives on Jan. 15, 910 on April 15, 890 on

July 15, and 880 on Oct. 15. The average number of covered lives is 895 [(900 +

910+ 890+ 880) ÷ 4 days].

As an alternative to counting actual lives, an employer can count the number of

employees with self-only coverage on the designated dates, plus the number of

employees with other than self-only coverage multiplied by 2.35.

3. Form 5500 method. If a Form 5500 for a plan is filed before the due date of the Form 720 for that year, the plan sponsor can determine the number of covered lives based on the Form 5500. If the plan offers just self-only coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) and divides by 2. If the plan also offers family or dependent coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) without dividing by 2.

Example: An employer offers single and family coverage with a plan year ending

on Dec. 31. The 2013 Form 5500 is filed on June 5, 2014, and reports 132

participants on line 5 and 148 participants on line 6d. The number of covered

lives is 280 (132 + 148).

To evaluate liability for PCOR fees, plan sponsors should identify all of their plans that provide medical benefits and determine if each plan is insured or self-insured. If any plan is self-insured, the plan sponsor should take the following actions:

While the rest of us were enjoying our Memorial Day holiday, the Department of Labor was busy posting the new model FMLA notices and medical certification forms… with an expiration date of May 31, 2018!

No more month-to-month extensions or lost sleep over when the long-awaited forms would be released.

That said, it couldn’t have taken DOL a whole lot of time to draft the updated forms. After a relatively close review of the new forms, the notable change is a reference to the Genetic Information Nondiscrimination Act (GINA). In the instructions to the health care provider on the certification for an employee’s serious health condition, the DOL has added the following simple instruction:

Do not provide information about genetic tests, as defined in 29 C.F.R. § 1635.3(f), genetic services, as defined in 29 C.F.R. § 1635.3(e), or the manifestation of disease or disorder in the employee’s family members, 29 C.F.R. § 1635.3(b).

The DOL added similar language to the other medical certification forms as well. For years, employers have included GINA disclaimers in their FMLA paperwork, and those disclaimers typically have been far more robust (and reader-friendly) than the cryptic one the DOL used above.

For easy reference, here are the links to the new FMLA forms:

The forms also can be accessed from this DOL web page.

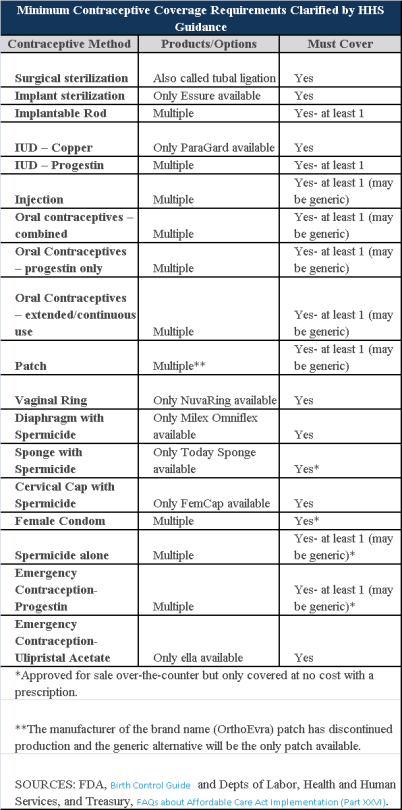

Plans and insurers must cover all 18 contraception methods approved by the U.S. Food and Drug Administration, according to a new set of questions and answers on the Affordable Care Act’s preventive care coverage requirements.

“Reasonable medical management” still may be used to steer members to specific products within those methods of contraception. A plan or insurer may impose cost-sharing on non-preferred items within a given method, as long as at least one form of contraception in each method is covered without cost-sharing.

However, an individual’s physician must be allowed to override the plan’s drug management techniques if the physician finds it medically necessary to cover without cost-sharing an item that a given plan or insurer has classified as non-preferred, according to one of the frequently asked questions from the U.S. Departments of Labor, Health and Human Services and the Treasury.

The ACA mandated all plans and insurers to cover preventive care items, as defined by the Public Health Service Act, without cost-sharing. Eighteen forms of female contraception are included under the preventive care list. The individual FAQs on contraception clarified the following requirements.

The FAQ comes just weeks after reports and news coverage detailed health plan violations of the women coverage provisions of the ACA.

Testing and Dependent Care Answers

In questions separate from contraception, plans and insurers were told they must cover breast cancer susceptibility (BRCA-1 or BRCA-2) testing without cost-sharing. The test identifies whether the woman has genetic mutations that make her more susceptible to BRCA-related breast cancer.

Another question stated that if colonoscopies are performed as preventive screening without cost-sharing, then plans could not impose cost-sharing on the anesthesia component of that service.

The Department of Labor has issued a final rule that will allow an employee to takeFMLA leave to care for a same-sex spouse, regardless of whether the employee lives in a state that recognizes their marital status. This rule change will impact the manner in which employers administer FMLA leave.

Where We Were

The FMLA regulations have guided us since their inception that the term “spouse” was to be defined according to the law of the state in which an employee resides, as opposed to the jurisdiction where the marriage was entered. This distinction became particularly significant after the U.S. Supreme Court’s decision in United States v. Windsor, which struck down Section 3 of the Defense of Marriage Act (DOMA) as unconstitutional. Before Windsor, that section restricted the definition of marriage for purposes of federal law to opposite-sex marriages. Consequently, federal FMLA leave was generally not available to same-sex married couples even in states that recognized gay marriage. Windsor effectively extended FMLA rights to same-sex married couples, but only if they resided in a state that recognized same-sex marriages, even if they were legally married in another state.

After the Windsor decision, President Obama instructed federal agencies such as the DOL to review all relevant federal statutes to implement the decision and, as expected, the DOL took it as an opportunity to apply Windsor to the FMLA regulations. In June 2014, the DOL adopted a proposed “state of celebration” rule, in which a spousal status for purposes of FMLA is determined not on the state in which the employee currently resides (as currently stated in the FMLA regulations), but based on the law of the state where the employee was married. Thus, if two individuals of the same sex get married in a state that recognizes same-sex marriage, they are considered to be married for federal FMLA purposes even if the state in which they live and work does not currently recognize same-sex marriage. For example, if the employee was married in New York, but now resides with his same-sex spouse in Texas, the employee will enjoy FMLA rights to care for his spouse as if he had resided in New York, since they were married in New York and that state recognizes the right of same-sex couples to marry.

Where We Are Now

After issuing its proposed rule in 2014, the agency now has announced that, on February 25, 2015, it will issue a new final rule (to take effect March 27, 2015) providing that the definition of “spouse” indeed is determined by the state in which a marriage is entered (i.e., the “state of celebration”). As the DOL points out, a place of celebration rule “allows all legally married couples, whether opposite-sex or same-sex, or married under common law, to have consistent federal family leave rights regardless of where they live.” The DOL notes that, as of February 13, 2015, 32 states and the District of Columbia (as well as 18 countries) extend the right to marry to both same- and opposite-sex partners.

A copy of the DOL’s fact sheet on the final rule can be accessed here.

What Does This Mean for Employers?

Here’s what employers need to know and do:

1. As an initial matter, determine whether the FMLA applies to you. If so, you should:

2. Whether or not FMLA applies to you, you should determine whether any state leave law applies to you. These laws may differ on their definitions of same-sex marriage, civil unions and domestic partnerships, and may offer different leave rights depending on the protected category.

3. Keep in mind two particular FAQs on This New DOL Rule (taken, in part, from of the DOL Final Rule FAQs):

Q. Can employers require documentation to verify that a same-sex or common law marriage is valid?

A. The Final Rule makes no changes to the manner in which employers may require employees who take leave to care for a family member to provide reasonable documentation for purposes of confirming a family relationship. An employee may satisfy this requirement either by providing documentation such as a marriage license or a court document, or by providing a simple statement asserting that the requisite family relationship exists. 29 C.F.R. § 825.122(k)

Here’s the catch: It is the employee’s choice to provide a simple statement or another type of document. And DOL has us in a trick bag as to when we can and should ask for reasonable documentation. On one hand, the agency tells us in the final rule, “Employers have the option to request documentation of a family relationship but are not required to do so in all instances.” It also rejected calls for instituting a standard in which employers would be required to show that they requested this documentation in a consistent, non-discriminatory manner. Yet, on the other hand, the DOL is quick to point out that employers “may not use a request for confirmation of a family relationship in a manner that interferes with an employee’s exercise or attempt to exercise his or her FMLA rights.”

Thus, from a practical standpoint, shouldn’t employers institute a consistently-applied, non-discriminatory policy when asking for confirmation that a family relationship exists? In a word, yes. Otherwise, employers risk a claim that they are treating certain employees in a discriminatory manner, thereby interfering with their FMLA rights.

One thing is clear: If an employee has already submitted proof of marriage to the employer for another purpose, such as in electing health care benefits for the employee’s spouse, the DOL finds that “such proof is sufficient to confirm the family relationship for purposes of FMLA leave.” So, employers, no second bites at the apple if you already have this information!

Q. Does the Final Rule Change the Manner in Which Employees Take FMLA leave to care for a child to whom they stand in loco parentis?

A. No. In June 2010, the DOL recognized that eligible employees may take leave to care for the child of the employee’s same-sex partner (married or unmarried) or unmarried opposite-sex partner, provided that the employee meets the in loco parentis requirement of providing day-to-day care or financial support for the child. (You can find more on the in loco parentis rule in DOL Fact Sheet #28B.) In other words, this new rule has no impact on the standards for determining the existence of an in loco parentis relationship.

While waiting for the pending issuance of the proposed Fair Labor Standards Act (FLSA) white-collar regulations, employers can begin taking some steps now to prepare.

Many believe the proposed regulations will be issued in March, although the proposed regs haven’t been sent yet to the Office of Management and Budget.

It is rumored that California’s quantitative duties test may be applied to the FLSA executive exemption, which would require employees to spend at least 50 percent of their time in exempt work in order to be classified as exempt. An adviser stated they would be surprised if thequantitative duties test was limited to the executive exemption and feel it might be applied as well to the administrative and professional exemptions.

Employers may begin doing an analysis now on their exempt population and how this change would affect them.

For many companies, some classes of employees are nonexempt in California, but exempt in the rest of the country. That may change with the new rule as well, if California’s quantitative duties test is applied across the nation.

Five Key Steps

Various legal counsel recommends five key steps employers should take now in anticipation of the revised overtime regulations:

Employers should begin now by talking to the managers or supervisors responsible for these exempt employees to determine the actual job duties for the employees as opposed to the stated job duties, because it’s the facts that matter most.

Employers need to know their workforce and be proactive. They should identify those exempt positions whose classification barely meets the FLSA minimum qualifications for a white-collar exemption under either the duties or compensation components. If either the duty or salary component is affected by regulatory changes, employers will know these identified positions will be targeted first.

The more lead time that a business has to grapple with these issues, the more satisfactory the process and the outcome will be for everyone.

The Department of Labor announced on June 20th a proposed rule that would allow an employee to take FMLA leave to care for their same-sex spouse, regardless of whether the employee lives in a state that recognizes their marital status. As expected, the DOL has adopted a “state of celebration” rule, in which a spousal status for purposes of FMLA is determined not on the state in which the employee currently resides (as currently stated in the FMLA regulations), but based on the law of the state where the employee was married. For example, if the employee was married in New York, but now resides with his same-sex spouse in Indiana, the employee will enjoy FMLA rights to care for his spouse as if he had resided in New York.

DOL’s Interpretation of FMLA after U.S. v. Windsor

The FMLA allows employees to take leave from work to care for a family member with a serious health condition. Before U.S. v. Windsor abolished certain portions of the Defense of Marriage Act (DOMA), same-sex couples were not allowed to take FMLA leave to care for a same-sex spouse, since DOMA did not recognize the relationship. After the Windsor decision but before the recent announcement, employees were eligible to take FMLA leave to care for a same-sex spouse only if they have resided in a state in which same-sex marriage is legal.

According to the DOL’s notification, the proposed new FMLA regulation includes the following highlights:

The proposed rule would mean that eligible employees, regardless of where they live, would be able to:

The DOL announced the proposed changes on Friday in a press release, stating, ”The basic promise of the FMLA is that no one should have to choose between succeeding at work and being a loving family caregiver … Under the proposed revisions, the FMLA will be applied to all families equally, enabling individuals in same-sex marriages to fully exercise their rights and fulfill their responsibilities to their families.”

The Notice is Not Unexpected

It was only a matter of time before this regulatory announcement became reality. In fact, the DOL foreshadowed the move when it issued Technical Release 2013-04 in September 2013, at which time the agency took the position that — at least with respect to employee benefit plans — the terms “spouse” and “marriage” in Title I of ERISA and its implementing regulations “should be read to include same-sex couples legally married in any state or foreign jurisdiction that recognizes such marriages, regardless of where they currently live.”

Next Steps

As with other proposed regulatory changes, the public will be given the chance to provide comment directly to the DOL on the proposed change before the agency issues a final rule on the issue. After the final rule is adopted, employers should review and amend their FMLA policy and procedures, as well as all FMLA-related forms and notices.

President Obama has proposed expanding the availability of overtime pay, which would cause the Department of Labor to do its first overhaul of Fair Labor Standards Act (FLSA) regulations in 10 years.

The President signed a memorandum on March 13, 2014, instructing the Department of Labor to update regulations about who qualifies for overtime pay. In particular, he wants to raise the threshold level for the salary-basis test from the current $455 per week in order to account for inflation. The threshold has been raised just twice in the past 40 years. The President did not specify the exact amount the threshold should be raised though.

“Unfortunately, today, millions of Americans aren’t getting the extra pay they deserve. That’s because an exception that was originally meant for high-paid, white-collar employees now covers workers earning as little as $23,660 a year,” Obama said in his remarks on overtime pay.

The memorandum also suggests that both the primary duties and pay of some exempted employees do not truly fit in the executive, administrative and professional employees exemptions, referred to as the white-collar exemptions under FLSA.

In a fact sheet on the President’s memorandum, the White House said: “Millions of salaried workers have been left without the protections of overtime or sometimes even the minimum wage. For example, a convenience store manager or a fast food shift supervisor or an office worker may be expected to work 50 or 60 hours a week or more, making barely enough to keep a family out of poverty, and not receive a dime of overtime pay.” The FLSA’s minimum wage would not protect a salaried worker because salaried workers’ pay must satisfy the weekly salary-basis test rather than the Federal hourly minimum wage, which is $7.25 per hour. The hourly minimum wage in Florida is currently $7.93 per hour.

The memo also pointed out that “only 12% of salaried workers fall below the threshold that would guarantee them overtime and minimum wage protections.“ The fact sheet also called the current FLSA regulations outdated, noting that states such as New York and California have set higher salary thresholds.

Small businesses will be hit particularly hard by a change in the FLSA regulations.

If the regulations shrink the current white-collar exemptions, employers would have two main options to hold down costs. They would have to either increase workers’ salary above the new salary-basis threshold (to avoid paying overtime) or leave employees in the nonexempt category and pay them overtime. Companies could also hire more employees, but the other two options are more likely.

Implications for HR

Once tightened white-collar exemptions are implemented, which is not likely to happen for months now, it could result in far-reaching implications for HR, including wage and hour audits and layoffs. The money to pay for increased overtime wages has got to come from somewhere which might mean layoffs, reducing overtime and taking a fresh look at the fluctuating workweek.

When asked at a press briefing about the burden on businesses if the Obama administration succeeds in efforts to both increase the federal minimum wage and revise FLSA regulations, Betsey Stevenson, a member of the White House’s Council of Economic Advisers, said, “We think these two items are very different, but, obviously, they do feed into the same thing, which is people should be rewarded for fair work.” She suggested that some workers in the white-collar exemptions aren’t even earning minimum wage for all the work they do at low salaries.

Even though the president did not assign a number for the minimum salary-basis threshold, Stevenson said the overtime “protections have been eroded over time. This threshold in 1975 was nearly $1,000 in today’s dollars; today it’s $455.” Stevenson believes that the rule should be modernized as a matter of the “basic principle of fairness.”

We will continue to keep you abreast of any changes to FLSA as well as other regulations that can impact your business. If you have any questions about the current or proposed FLSA regulations, please contact our office.

As a business owner, it is important to understand how the Affordable Care Act may affect your business. However, with so many misconceptions about about Health Care Reform works, this can be difficult.

A common myth is that business owners will be fined if they do not provide notification to their employees about the new Health Insurance Marketplace.

If your company is covered by the Fair Labor Standards Act (FLSA), you must provide a written notice to your employees about the Health Insurance Marketplace (aka Exchange) by October 1, 2013, however the Department of Labor has announced is no fine or penalty currently under the law for failing to provide this notice.

For more information on the Exchange notice, please contact our office or review a previous post on this topic.

The health insurance Marketplace created by the Affordable Care Act (ACA) will open on October 1st. Most small employers (those with 50 or fewer full-time employees) are not required to offer health insurance coverage under ACA. Businesses with more than 50 full time employees have gotten a one year reprieve from the “pay or play” penalties. But all companies, regardless of size, are required to notify their employees about the Obamacare Marketplaces by October 1st.

The state and federal insurance exchanges are websites on which individuals and small businesses can shop for health plans. Though the deadline is less than a month away, many small businesses may not realize they have to notify employees of the existence of the Marketplace (aka Exchange). Many small business owners are unaware of this requirement or are under the misconception that it does not apply to them because they are too small to be governed by the health care reform law’s mandate. It is not clear how the requirement will be enforced yet, but penalties for businesses that do not comply could reach $100 per worker per day.

Some employers assume that because they are a small business who does not offer health insurance currently that the requirement does not apply to them. The Exchange notification requirement applies to any business regulated under the Fair Labor Standards Act (FLSA), which covers all companies with at least one employee and $500,000 in annual revenue.

The U.S. Department of Labor has posted information about the notification requirement on its website and has provided model notices (in both English & Spanish) to be used by both employers who offer insurance and those who do not offer insurance.

The one to three page model notices can be downloaded, filled out, and printed, either for distribution in the workplace or for mailing to employees’ homes. Employees who are hired after October 1st must be provided the notice within 14 days of their date of hire with the company. Employees must be provided the notice, regardless of their enrollment status in the group’s medical plan. The safest route is to distribute the notice via U.S. mail or follow the instructions for distributing it electronically. Currently there is no requirement that states the employer must obtain signatures from employees confirming their receipt of the notice.

Please contact our office for more information on how to ensure you business is compliant with ACA requirements in 2014.

You may be already aware of the continuing escalation of all forms of whistleblower and retaliation claims, including the 20+ Anti-Retaliation laws enforced by special investigators from OSHA’s Whistleblower group.

On one of OSHA’s recent news releases, they state that the Labor Department filed a federal lawsuit against Duane Thomas Marine Construction and its owner Duane Thomas for terminating an employee who reported workplace violence, which is a violation of Section 11© of the OSH Act. OSHA asserts the employer fired an employee for complaining about unsafe work conditions. It may seem a bit unusual to hear that the alleged unsafe conditions involved fear of workplace violence, but who can blame an employee in today’s current environment. However, as it turns out the hazard the employee complained about was the owner!

The employee alleged that, on numerous occasions between 2009 and 2011, Mr. Thomas committed workplace violence and created hostile working conditions. He allegedly behaved abusively, make inappropriate sexual comments and advanced, yelled, screamed, and made physically threatening gestures, in addition to withholding the employee’s paycheck.

The employee, who worked directly for Mr. Thomas, reported to him that he was creating hostile conditions. On Feb 25, 2011, the employee filed a timely whistleblower compliant with OSHA alleging discrimination by Thomas for having reported the conditions to him.

On March 28, Thomas received notification of the complaint filing. Five days later, Thomas had computer passwords changed to deny the employee remote access to files and then terminated the employee. OSHA’s subsequent investigation found merit to the employee’s compliant.

OSHA is seeking back wages, interest, and compensatory and punitive damages, as well as front pay in lieu of reinstatement for the employee. Additionally, OSHA seeks to have the employee’s personnel records expunged with respect to the matters at issue in this case and bar the employer against future violations of the OSH Act. Wow…. but the usual warning: we may not know all of the facts.

The employer may have behaved badly and gave the employee the ability to make out a viable claim. Or, the employee may have exaggerated, or even made up the whole thing. But while most employee lawsuits are notorious for not being completely accurate, there must be at least some pretty bad facts for OSHA to take the action it did.

This atmosphere may or may not have presented a valid safety hazard, but guess what? Under the law, the violation is the act of terminating the employee for complaining about a safety concern. And the catch is…the concern does not have to be valid! Please note there is a different standard if the employee refuses to work because of an unfounded and unreasonable concern.

For all we know, the employee could have annoyed his boss with unfounded complaints until the boss fired him in a moment of anger…but that too is a potential violation.

The take away advice from this scenario is to eliminate two phrases from your vocabulary: “Boys will be boys” and “You had to be there”. The main problem is that lawyers and Uncle Sam will ultimately be there if one’s conduct is foolish enough.

Be sure to train your supervisors to behave professionally regardless of the setting and remind them of the many behaviors, including some of the offbeat ones, that are protected as Whistleblowing.