IRS has begun notifying employers of their potential liability for an ACA employer shared responsibility payment in connection with the 2015 calendar year. It recently released Forms 14764 and 14765, which employers can use to dispute the assessment.

The Affordable Care Act (ACA) imposes employer shared responsibility requirements that are commonly referred to as the “employer mandate.” Beginning in 2015, applicable large employers (ALEs) – generally, employers with at least 50 full-time employees – are required to offer minimum essential coverage to substantially all full-time employees and their dependents, or pay a penalty if at least one full-time employee enrolls in marketplace coverage and receives a premium tax credit. Even if they offer employees coverage, ALEs may still be subject to an employer shared responsibility payment if the coverage they offer to full-time employees does not meet affordability standards or fails to provide minimum value.

The IRS announced their plans in Fall of 2017 to notify employers of their potential liability for an employer penalty for the 2015 calendar year. It released FAQs explaining that Letter 226J will note the employees by month who received a premium tax credit, and provide the proposed employer penalty. Additionally, the IRS promised to release forms for an employer’s penalty response and the employee premium tax credit (PTC) list respectively.

IRS subsequently issued Form 14764, the employer penalty Response, and Form 14765, the Employee PTC Listing. Together, these forms are the vehicle for employers to respond to a Letter 226J.

On Form 14764, employers indicate full or partial agreement or disagreement with the proposed employer penalty, as well as the preferred employer penalty payment option. An employer that disagrees with the assessment must include a signed statement explaining the disagreement, including any supporting documentation. This form also allows employers to authorize a representative, such as an attorney, to contact the IRS about the proposed employer penalty.

On Form 14765, the IRS lists the name and last four digits of the social security number of any full-time employee who received a premium tax credit for one or more months during 2015 and where the employer did not qualify for an affordability safe harbor or other relief via Form 1095-C. Each monthly box has a row reflecting any codes entered on line 14 and line 16 of the employee’s Form 1095-C. If a given month is not highlighted, the employee is an assessable full-time employee for that month – resulting in a potential employer assessment for that month.

If information reported on an employee’s Form 1095-C was not accurate or was incomplete, an employer wishing to make changes must use the applicable indicator codes for lines 14 and 16 described in the Form 1094-C and 1095-C instructions. The employer should enter the new codes in the second row of each monthly box by using the indicator codes for lines 14 and 16. The employer can provide additional information about the changes for an employee by checking the “Additional Information Attached” column. As mentioned:

Employers: Carefully Consider 226J Letter Responses

Miscoding can happen for different reasons, including vendor errors and inaccurate data. To minimize risk of additional IRS exposure, employers should carefully consider how best to respond to a 226J letter given circumstances surrounding the disputed assessments. For example, changing the coding on the 1095-C of an employee from full-time to part-time could trigger further review or questions by the IRS on the process for determining who is a full-time employee – and may increase the likelihood of IRS penalties for reporting errors on an employer’s Form 1095-Cs.

In its October FAQs, the IRS stated that it “plans to issue Letter 226J informing ALEs of their potential liability for an employer shared responsibility payment, if any, in late 2017.” If the IRS sticks to that timing, all notices should be sent out by the end of this calendar year. However, because the IRS has not indicated that it will inform employers that they have no employer penalty due, it is impossible to say that an employer not receiving a Letter 226J in 2017 is home free for 2015 employer penalties.

Employers should review the newly released forms so they are prepared to respond within 30 days of the date on the Letter 226J. They should also ensure processes are in place to make these payments, as necessary. Even employers who are not expecting any assessments will need to prepare to respond to the IRS within the limited timeframe to dispute any incorrect assessments.

As we near closer to Thanksgiving, it’s safe to say we are in “late 2017” territory. Last week, the IRS issued new FAQ guidance informing employers that they can expect notice of any potential ACA employer mandate pay or play penalties in late 2017.

What Will the Letter Look Like?

The IRS recently posted a copy of the Letter 226J here: https://www.irs.gov/pub/notices/ltr226j.pdf

Letters Will Look Back to 2015

The ACA employer mandate pay or play rules first took effect in 2015. The IRS Letters 226J at issue will relate only to potential penalties in that first year, and therefore they will be relevant only to employers that were applicable large employers (ALEs) in 2015.

In general, an employer was an ALE in 2015 if it (along with any members in its controlled group) employed an average of at least 50 full-time employees, including full-time equivalent employees, on business days during the preceding calendar year (2014).

Note that a special 2015 transition rule provided that certain “mid-sized” employers between 50 and 100 full-time employees could have reported an exemption from potential pay or play penalties.

What Are the Potential 2015 Penalties?

a) §4980H(a)—The “A Penalty” aka No Coverage Offered

This is the big “sledge hammer” penalty for failure to offer coverage to substantially all full-time employees. In 2015, this standard required an offer of coverage to at least 70% of the ALE’s full-time employees. (For 2016 forward, this standard has been increased to 95%).

The 2015 A Penalty was $173.33/month ($2,080 annualized) multiplied by all full-time employees then reduced by the first 80 full-time employees (reduced by the first 30 full-time employees for 2016 forward). It was triggered by at least one full-time employee who was not offered group coverage enrolling in subsidized coverage on the Exchange.

The reduced 70% threshold for the 2015 penalty should be sufficient for virtually all ALEs in 2015 to avoid the A Penalty, provided they offered a group health plan with eligibility set at 30 hours per week or lower. It would be very unlikely for a surprise A Penalty to arise for 2015.

b) §4980H(b)—The “B Penalty” aka Coverage Not Affordable

This is the much smaller “tack hammer” penalty that will apply where the ALE is not subject to the A Penalty (i.e., the ALE offered coverage to at least 70% of full-time employees in 2015, or 95% thereafter). It applies for each full-time employee who was not offered coverage, offered unaffordable coverage, or offered coverage that did not provide minimum value and was enrolled in subsidized converge on the Exchange.

The 2015 B Penalty was $260/month ($3,120 annualized). Unlike the A Penalty, the B Penalty multiplier is only those full-time employees not offered coverage (or offered unaffordable or non-minimum value coverage) who actually enrolled in the Exchange. The multiple is not all full-time employees.

What Happened to My Section 1411 Certification?

In the vast majority of states, they never came!

In short, the 1411 Certification (typically referred to as Employer Exchange Notices) informs the employer that one or more of their employees have been conditionally approved for subsidies (the Advance Premium Tax Credit) to pay for coverage on the exchange.

One important purpose of the notice is it provides employers with the chance to contemporaneously challenge the employee’s subsidy approval. Near the time of the employee’s subsidy approval, the ALE can show that it made an offer of minimum essential coverage to the full-time employee that was affordable and provided minimum value.

In other words, the notices provide the ALE with the opportunity to prevent the employee from incorrectly receiving the subsidies, and the ALE from ever receiving the Letter 226J from the IRS (because all ACA pay or play penalties are triggered by a full-time employee’s subsidized Exchange enrollment).

CMS admitted in a September 2015 FAQ that they were not able to send the notices for 2015 for federal exchange enrollment (most state exchanges took the same approach), but the potential penalties will nonetheless still apply.

The result is that ALEs will for be receiving their first notice of potential 2015 penalties via IRS Letter 226J in “late 2017.”

How Does the IRS Determine Potential Penalties?

The 2015 ACA reporting via Forms 1094-C and 1095-C (as well as the employee’s subsidized exchange enrollment data for 2015) serve as the primary basis for the IRS determination.

What Do I Need to Do?

First of all, review the information carefully.

The first-year ACA reporting for 2015 was a particularly difficult one, and one in which the IRS provided extended deadlines and a good faith efforts standard. It is very possible that the numerous challenging systems issues that made the first-year (and, frankly, all subsequent years) ACA reporting so difficult resulted in certain inaccuracies on the 2015 Forms 1094-C and 1095-C.

Be sure to review any potential penalties carefully with your systems records to confirm the reporting was correct.

a) If You Agree with the Penalty Determination – You will complete and return a Form 14764 that is enclosed with the letter, and include full payment for the penalty amount assessed (or pay electronically via EFTPS).

b) If You Disagree with the Penalty Determination – The enclosed Form 14764 will also include a “ESRP Response” form to send to the IRS explaining the basis for your disagreement. You may include any documentation (e.g., employment or offer of coverage records) with the supporting statement.

The response statement will also need to include what changes the ALE would like to make to the Forms 1094-C and/or 1095-C on the enclosed “Employee PTC Listing,” which is a report of the subsidized Exchange enrollment for all of the ALE’s full-time employees. The Letter 226J includes specific instructions on completing this process.

The IRS will respond with a Letter 227 that acknowledges the ALE’s response to Letter 226J and describes any further actions the ALE may need to take. If you disagree with the Letter 227, you can request a “pre-assessment conference” with the IRS Office of Appeals within 30 days from the date of the Letter 227.

If the IRS determines at the end of the correspondence and/or conference that the ALE still owes a penalty, the IRS will issue Notice CP 220J. This is the notice and demand for payment, with a summary of the pay or play penalties due.

Under the Affordable Care Act, (ACA) a fund for a new nonprofit corporation to assist in clinical effectiveness research was created. To aid in the financial support for this endeavor, certain health insurance carriers and health plan sponsors are required to pay fees based on the average number of lives covered by welfare benefits plans. These fees are referred to as either Patient-Centered Outcome Research Institute (PCORI) or Clinical Effectiveness Research (CER) fees.

The applicable fee was $2.26 for plan years ending on or after October 1, 2016 and before October 1, 2017. For plan years ending on or after October 1, 2017 and before October 1, 2018, the fee is $2.39. Indexed each year, the fee amount is determined by the value of national health expenditures. The fee phases out and will not apply to plan years ending after September 30, 2019.

As a reminder, fees are required for all group health plans including Health Reimbursement Arrangements (HRAs), but are not required for health flexible spending accounts (FSAs) that are considered excepted benefits. To be an excepted benefit, health FSA participants must be eligible for their employer’s group health insurance plan and may include employer contributions in addition to employee salary reductions. However, the employer contributions may only be $500 per participant or up to a dollar for dollar match of each participant’s election.

HRAs exempt from other regulations would be subject to the CER fee. For instance, an HRA that only covered retirees would be subject to this fee, but those covering dental or vision expenses only would not be, nor would employee EAPs, disease management programs and wellness programs be required to pay CER fees.

In a recent statement released by the IRS it advised that it would not accept individual 2017 tax returns that did not indicate whether the individual had health coverage, had an exemption from the individual mandate, or will make a shared responsibility payment under the individual mandate. Therefore, for the first time, an individual must complete line 61 (as shown in previous iterations) of the Form 1040 when filing his/her tax return. This article explains what the new IRS position means for the future of ACA compliance from an employer’s perspective.

First, it will be critical (more so this year than in year’s past) that an employer furnish its requisite employees the Form 1095-C by the January 31, 2018 deadline. In previous years, this deadline was extended (to March 2, 2017 last year). However, with the IRS now requiring the ACA information to be furnished by individual tax day, April 17, 2018, employers will almost certainly have to furnish the Form 1095-C to employees by the January 31, 2018 deadline. This is a tight deadline and will require employers to be on top of their data as the 2017 calendar year comes to a close.

An employee who is enrolled in a self-insured plan will need the information furnished in part III of the Form 1095-C to complete line 61 on his/her tax return. It is reasonable to assume that an employee is more likely to inquire as to the whereabouts of the Affordable Care Act information necessary to complete his/her 2017 tax return. Therefore, the possibility of word getting back to the IRS that an employer is not furnishing the Form 1095-C statements to employees is also likely greater in 2017 compared to past years. Remember, an employer can be penalized $260 if it fails to furnish a Form 1095-C that is accurate by January 31, 2018 to the requisite employees. This penalty is capped at $3,218,500. The $260 per Form penalty and the cap amount can be increased if there is intentional disregard for the filing requirements.

The IRS statement continues the IRS’ trend of being more strenuous with ACA requirements. Many employers have received correspondence from the IRS about missing Forms 1094-C and 1095-C for certain EINs. Frequently, this has been caused by the employer incorrectly filing one Form 1094-C for the aggregated ALE group as opposed to a Form 1094-C for each Applicable Large Employer member (ALE member). While the IRS’ latest statement does not ensure that enforcement of the employer mandate (the section 4980H penalties) is coming soon, one could infer that the IRS will soon be sending out penalty notices with respect to the employer mandate.

With the actions taken by the IRS in 2017, all employers need to be taking the reporting of the Forms 1094-C and 1095-C seriously. As of the date of this publication, the Form 1095-C must be furnished to an employer’s requisite employees by January 31, 2018.

With the Republicans’ failure to pass a bill to repeal and replace the Affordable Care Act (ACA), employers should plan to remain compliant with all ACA employee health coverage and annual notification and information reporting obligations.

Even so, advocates for easing the ACA’s financial and administrative burdens on employers are hopeful that at least a few of the reforms they’ve been seeking will resurface in the future, either in narrowly tailored stand-alone legislation or added to a bipartisan measure to stabilize the ACA’s public exchanges. Relief from regulatory agencies could also make life under the ACA less burdensome for employers.

“Looking ahead, lawmakers will likely pursue targeted modifications to the ACA, including some employer provisions,” said Chatrane Birbal, senior advisor for government relations at the Society for Human Resource Management (SHRM). “Stand-alone legislative proposals have been introduced in previous Congresses, and sponsors of those proposals are gearing up to reintroduce bills in the coming weeks.”

These legislative measures, Birbal explained, are most likely to address the areas noted below.

(more…)

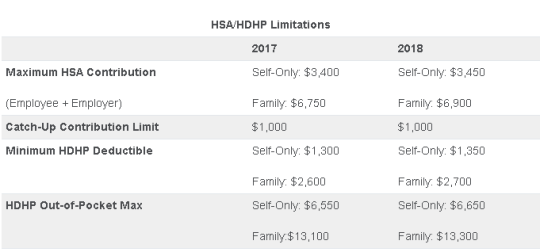

On May 4, 2017, the IRS released Revenue Procedure 2017-37 setting dollar limitations for health savings accounts (HSAs) and high-deductible health plans (HDHPs) for 2018. HSAs are subject to annual aggregate contribution limits (i.e., employee and dependent contributions plus employer contributions). HSA participants age 55 or older can contribute additional catch-up contributions. Additionally, in order for an individual to contribute to an HSA, he or she must be enrolled in a HDHP meeting minimum deductible and maximum out-of-pocket thresholds. The contribution, deductible and out-of-pocket limitations for 2018 are shown in the table below (2017 limits are included for reference).

Note that the Affordable Care Act (ACA) also applies an out-of-pocket maximum on expenditures for essential health benefits. However, employers should keep in mind that the HDHP and ACA out-of-pocket maximums differ in a couple of respects. First, ACA out-of-pocket maximums are higher than the maximums for HDHPs. The ACA’s out-of-pocket maximum was identical to the HDHP maximum initially, but the Department of Health and Human Services (which sets the ACA limits) is required to use a different methodology than the IRS (which sets the HSA/HDHP limits) to determine annual inflation increases. That methodology has resulted in a higher out-of-pocket maximum under the ACA. The ACA out-of-pocket limitations for 2018 were announced are are $7350 for single and $14,700 for family.

Second, the ACA requires that the family out-of-pocket maximum include “embedded” self-only maximums on essential health benefits. For example, if an employee is enrolled in family coverage and one member of the family reaches the self-only out-of-pocket maximum on essential health benefits ($7,350 in 2018), that family member cannot incur additional cost-sharing expenses on essential health benefits, even if the family has not collectively reached the family maximum ($14,700 in 2018).

The HDHP rules do not have a similar rule, and therefore, one family member could incur expenses above the HDHP self-only out-of-pocket maximum ($6,650 in 2018). As an example, suppose that one family member incurs expenses of $10,000, $7,350 of which relate to essential health benefits, and no other family member has incurred expenses. That family member has not reached the HDHP maximum ($14,700 in 2018), which applies to all benefits, but has met the self-only embedded ACA maximum ($7,350 in 2018), which applies only to essential health benefits. Therefore, the family member cannot incur additional out-of-pocket expenses related to essential health benefits, but can incur out-of-pocket expenses on non-essential health benefits up to the HDHP family maximum (factoring in expenses incurred by other family members).

Employers should consider these limitations when planning for the 2018 benefit plan year and should review plan communications to ensure that the appropriate limits are reflected.

Yesterday (May 4, 2017) , the House of Representatives narrowly passed the American Health Care Act of 2017 (AHCA), which contains major parts that would repeal and replace the Affordable Care Act (commonly referred to as Obamacare or ACA). The next obstacle the bill faces is making it through the Senate, which proves to be a formidable challenge.

The nonpartisan Congressional Budget Office has not had time yet to analyze the current version of the bill, but this is expected next week. The bill must now pass the Senate and could get pushed back to the House if it sees changes in the upper chamber.

In the meantime, here are some highlights we know about the bill based on how it is written today and how it would work:

We will continue to keep you up to date on the bill as it progress through legislation.

Until very recently, employers were at risk of receiving steep fines if they reimbursed employees for non-employer sponsored medical care – the Affordable Care Act (ACA) included fines of up to $36,500 a year per employee for such an action. Late in 2016, however, President Obama signed the 21st Century Cures Act and established Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs). As of January 1, 2017, small employers can offer these tax-free medical care reimbursements to eligible employees.

If an employee incurs a medical care expense, such as health insurance premiums or eligible medical expenses under IRC Section 213(d), the employer can reimburse the employee up to $4,950 for single coverage or $10,000 for family coverage. Employees may not make any contributions or salary deferrals to QSEHRAs.

The maximum amount must

be prorated for those not eligible for an entire year. For example, an employer

offering the maximum reimbursement amount should only reimburse up to $2,475 to

an employee who has been working for the company for six months. For a complete

list of medical expenses covered under IRC 213(d), see https://www.irs.gov/pub/irs-pdf/p502.pdf.

Employers may tailor which expenses they will reimburse to a certain extent,

and do not have to reimburse employees for all eligible medical expenses.

Much like other healthcare reimbursement arrangements, employees may have to provide substantiation before reimbursement. The IRS has discretion to establish requirements regarding this process, but has not yet done so. Although reimbursements may be provided tax-free, they must be reported on the employee’s W-2 in Box 12 using the code “FF.”

To offer QSEHRAs, an employer cannot be an applicable large employer (ALE) under the ACA. Only employers with fewer than 50 full-time equivalent employees can offer this benefit. Further, a group cannot offer group health plans to any employees to qualify.

Typically, an employer that chooses to offer a QSEHRA must offer it to all employees who have completed at least 90 days of work. The few exceptions to this rule include part-time or seasonal employees, non-resident aliens, employees under the age of 25, and employees covered by a collective bargaining agreement.

Employers may offer differing reimbursement amounts based on employee age or family size. However, such variances must be based on the cost of premiums of a reference policy on the individual market. It is currently unclear which reference policy will be selected or how permitted discrepancies will be calculated.

To be eligible for a tax-free reimbursement, employees must have proof of minimum essential coverage. It is uncertain how closely employers will have to scrutinize such proof, although guidance will hopefully be available soon.

Eligible employees must disclose to health exchanges the amount of QSEHRA benefits available to them. The exchanges will account for the reported amount, even if the employee does not utilize it, and will likely reduce the amount of the subsidies available. Employers should take this into account before adopting a QSEHRA.

In order to establish a QSEHRA, employers will have to set up and administer a plan. Group health plan requirements, such as ACA reporting and COBRA requirements, do not apply to QSEHRAs. But in order to properly provide reimbursements to employees, employers will likely have to establish reimbursement procedures.

Additionally, any eligible employees must be notified of the arrangements in writing at least 90 days before the first day they will be eligible to participate. For the current year, the IRS is giving employers who implement QSEHRAs an extension until March 13, 2017 to provide a notice. The notice must provide the amount of the maximum benefit, and that eligible employees inform health insurance exchanges this benefit is available to them. It also must inform eligible employees they may be subject to the individual ACA penalties if they do not have minimum essential coverage.

On February 23, 2017, the Centers for Medicare and Medicaid Services released an insurance standards bulletin allowing states once again to extend the life of “grandmothered” (aka transitional health insurance or non-ACA) medical policies to policy years beginning on or before October 1, 2018, as long as the policies do not extend beyond December 31, 2018. These plans will continue to be exempt from most of the ACA’s insurance reform provisions which otherwise became effective on January 1, 2014.

On November 14, 2013, facing political pressure from millions of consumers who were receiving cancellation notices for their 2013 coverage, the Obama administration announced in guidance that states could allow insurers to extend noncompliant coverage for policy years beginning before October 1, 2014, free from certain of the ACA reforms. In March of 2014, the administration extended the life of these “grandmothered” or “transitional” plans to coverage renewed by October 1, 2016 and eventually until the end of 2017.

While the original transitional decision could perhaps have been justified by the inherent authority in the executive to reasonably delay the implementation of new legal requirements, the extension of the original delay looked increasingly political and was harder to justify legally. It also likely did serious damage to the ACA-compliant individual market. Insurers had set their 2014 premiums in the expectation that the entire non-grandfathered market would transfer to ACA-compliant plans. Instead, healthier individuals likely remained with their earlier, health-status-underwritten coverage, making the pool of consumers that actually bought 2014 coverage less healthy than expected. The transitional policy very likely played a significant role in the large insurer losses in the individual market for 2014, and played a role in raising premiums going forward.

As of today, there are probably a little fewer than a million Americans still in individual market transitional plans, although the percentage of the individual market in transitional plans varies greatly from state to state, and many remain covered in small group transitional plans. It has been thought that consumers and employers prefer transitional plans because they cost less or have lower cost-sharing.

The Trump administration’s guidance states that it is based on a commitment to “smoothly bringing all non-grandfathered coverage in the individual and small group market into compliance with all applicable” ACA requirements. One must wonder, however, why four years will be enough for a smooth transition if three years was not.

The guidance gives states the option of extending the transition for a shorter (but not longer) period of time and also of applying it to both the small group and individual markets or to either market separately. States also have the option of authorizing part-year policies if necessary to ensure that coverage ends at the end of 2018.