Page 1 of 3

Thanks in part to persistent high inflation, employees will be able to sock away a lot more money in their health savings accounts (HSAs) next year.

Annual health savings account contribution limits for 2024 are increasing in one of the biggest jumps in recent years, the IRS announced May 16: The annual limit on HSA contributions for self-only coverage will be $4,150 in 2023, a 7.8 percent increase from the $3,850 limit in 2023. For family coverage, the HSA contribution limit jumps to $8,300 in 2023, up 7.1 percent from $7,750 in 2023.

Participants 55 and older can still contribute an extra $1,000 to their HSAs.

Meanwhile, for 2024, a high-deductible health plan (HDHP) must have a deductible of at least $1,600 for self-only coverage, up from $1,500 in 2023, or $3,200 for family coverage, up from $3,000, the IRS noted. Annual out-of-pocket expense maximums (deductibles, co-payments and other amounts, but not premiums) cannot exceed $8,050 for self-only coverage in 2024, up from $7,500 in 2023, or $16,100 for family coverage, up from $15,000.

The increases are detailed in IRS Revenue Procedure 2023-23 and take effect in January 2024.

While expected, the increase in 2024 HSA limits is significant for passing certain symbolic financial thresholds. For the first time, including catch-up contributions for those age 55 and older, a couple on family coverage can now contribute more than $10,000, and a single person on self-only coverage can now contribute more than $5,000.

Many industry experts tout health savings accounts as a smart way for employees to save for medical expenses, even in retirement, citing their triple tax benefits: Contributions are made pretax, the money in the accounts grows tax free and withdrawals for qualified medical expenses are tax free. This is very good news to help more Americans understand and use HSAs as a powerful tool in their healthcare spending and long-term savings.

HSA enrollment continues to grow, and more employers also are offering contributions to employees’ accounts. At the end of 2022, Americans held $104 billion in 35.5 million health savings accounts, according to HSA advisory firm Devenir.

Despite the benefits, most holders aren’t taking full advantage of their accounts and are missing out on substantial rewards, according to the Employee Benefit Research Institute. The average account holder has a modest balance, contributes far less than the maximum and does not invest their HSA, recent EBRI data found.

It has been previously discussed that President Biden announced an end to the COVID-19 Public Health Emergency (PHE) and National Emergency (NE) periods on May 11, 2023, and the practical ramifications for employer group health plan sponsors as they administer COBRA, special enrollment, and other related deadlines tied to the end of the NE. As discussed, this action generally meant that all applicable deadlines were tolled until the end of the NE plus 60 days, or July 10, 2023, with all regular (non-extended) deadlines taking effect for applicable events occurring after that.

A Change in the National Emergency End Date

A new wrinkle recently added a potential complication to calculating these deadlines. President Biden signed H.R. Res. 7 into law on April 10, 2023, after Congress jointly introduced H.R. Res. 7 as a one-line action to end the NE, effective immediately. The consequence is that the applicable end of the transition relief is now June 9, 2023 (60 days following April 10, 2023) instead of July 10, 2023, as previously anticipated. The Department of Labor (DOL), however, has informally announced that despite the statutory end of the NE being 30 days earlier than expected, to avoid potential confusion and changes to administrative processes already in progress, the deadline of July 10, 2023, will remain the relevant date for COBRA, special enrollment, and other related deadlines under previous guidance. Prophetically, updated FAQs, released March 29, 2023, by the DOL, Department of Treasury, and Department of Health and Human Services (the Agencies), provide, “the relief generally continues until 60 days after the announced end of the COVID-19 National Emergency or another date announced by DOL, the Treasury Department, and the IRS (the “Outbreak Period”). [emphasis added]” Further clarification and formal guidance are still expected.

Updated DOL FAQ Guidance

Most employers rely on third-party vendors and consultants to help administer COBRA, special enrollments, claims, appeals, etc. All should be aware of the impact the end of the NE and PHE has on all applicable deadlines. The FAQs provide at Q/A-5 specific examples to help employers, consultants, and administrators apply the end of NE and PHE deadlines and different scenarios related to COBRA elections and payments before and after the end of the Outbreak Period, special enrollment events, Medicaid election changes, etc. The FAQs also make clear that employers are encouraged to consider extending these deadlines for the current plan year. Employers should discuss the impact of this guidance with their vendors and consultants to ensure all parties comply with the upcoming transitional periods.

The FAQs also confirm (at Q/A 1-4) the impact of the end of the PHE on COVID-19-related testing and diagnostic procedures, noting that as of the end of the PHE on May 11, 2023, group health plans are no longer required to provide certain COVID-19 related coverage at 100 percent under the plan, but can revert to previous cost-sharing and deductible limitations that existed before the COVID-19 pandemic. Note that President Biden’s recent action approving the end of the NE on April 10, 2023, has no impact on the previously communicated end to the PHE on May 11, 2023. Employers should review changes in coverage of COVID-19 testing and other related treatment or procedures with their insurance carriers, consultants, and advisors, including any notices that may be required in connection with those changes. The DOL confirmed that while encouraged to do so, employers do not have to provide any separate notification of any changes in current coverage limits before the PHE end date unless the employer had previously disclosed a different level of coverage in its current Summary of Benefits and Coverage (SBC) provided during the most recent open enrollment period.

COVID-19 Testing and Treatment Under High Deductible Health Plan/Health Savings Accounts

Q/A-8 of the FAQs provides interim clarification regarding the impact of the end of the PHE on high-deductible health plans (HDHPs) that are tied to health savings accounts (HSAs) and the ability to provide medical coverage for COVID-19 testing or treatment without requiring an employee to satisfy applicable HDHP deductibles for HSA contribution purposes. Even though IRS Notice 2020-15 provided relief from general deductible limitations under Code Section 223(c)(1) through the end of the PHE, the Agencies have determined this relief will remain in effect after the end of the PHE and until the IRS issues further guidance.

Employees can put an extra $200 into their health care flexible spending accounts (health FSAs) next year, the IRS announced on Oct. 18, as the annual contribution limit rises to $3,050, up from $2,850 in 2022. The increase is double the $100 rise from 2021 to 2022 and reflects recent inflation.

If the employer’s plan permits the carryover of unused health FSA amounts, the maximum carryover amount rises to $610, up from $570. Employers may set lower limits for their workers.

The limit also applies to limited-purpose FSAs that are restricted to dental and vision care services, which can be used in tandem with health savings accounts (HSAs).

The IRS released 2023 HSA contribution limits in April, giving employers and HSA administrators plenty of time to adjust their systems for the new year. The individual HSA contribution limit will be $3,850 (up from $3,650) and the family contribution limit will be $7,750 (up from $7,300).

CARRYOVER AMOUNTS OR GRACE PERIOD

Health or dependent care FSA funds that are not spent by the employee within the plan year can include a two-and-a-half-month grace period to spend down remaining FSA funds, if employees are enrolled in FSAs that have adopted the grace period option.

Health FSAs have an additional option of allowing participants to carry over unused funds at the end of the plan year, up to an inflation-adjusted limit set by the IRS, and still contribute up to the maximum in the next plan year. Health FSA plans can elect either the carryover or grace period option but not both.

Dependent Care FSAs

A dependent care FSA (DC-FSA) is a pretax benefit account used to pay for dependent care services such as day care, preschool, summer camps and non-employer-sponsored before or after school programs. Funds may be used for expenses relating to children under the age of 13 or incapable of self-care who live with the account holder more than half the year.

These plans may also be referred to as dependent care assistance plans (DCAPs) or dependent care reimbursement accounts (DCRAs).

In general, an FSA carryover only applies to health FSAs, although COVID-19 legislation permitted a carryover of unused balances for DC-FSAs into the next plan year for plan years 2020 and 2021 only.

The dependent care FSA maximum annual contribution limit is not indexed and did not change for 2022 or for 2023. It remains $5,000 per household for single taxpayers and married couples filing jointly, or $2,500 for married people filing separately. Married couples have a combined $5,000 limit, even if each has access to a separate DC-FSA through his or her employer.

Maximum contributions to a DC-FSA may not exceed these earned income limits:

Employers can also choose to contribute to employees’ DC-FSAs. However, unlike with a health FSA, the combined employer and employee contributions to a DC-FSA cannot exceed the IRS limits noted above.

A separate tax code child and dependent care tax credit cannot be claimed for expenses paid through a DC-FSA, as “double dipping” is not permitted.

The new 2023 limits are:

HSA – Single $3,850 / Family $7,750 per year

HDHP (self-only coverage) – $1,500 minimum deductible / $7,500 out-of-pocket limit

HDHP (family coverage) – $3,000 minimum deductible / $15,000 out-of-pocket limit

The IRS has released the 2022 contribution limits for FSA and several other benefits in Revenue Procedure 2021-45. The limits are effective for plan years that begin on or after January 1, 2022.

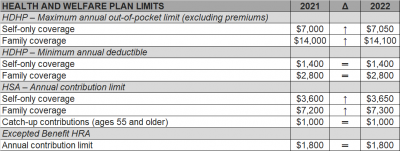

The Internal Revenue Service (IRS) recently announced (See Revenue Procedure 2021-25) cost-of-living adjustments to the applicable dollar limits for health savings accounts (HSAs), high-deductible health plans (HDHPs) and excepted benefit health reimbursement arrangements (HRAs) for 2022. Many of the dollar limits currently in effect for 2021 will change for 2022. The HSA catch-up contribution for individuals ages 55 and older will not change as it is not subject to cost-of-living adjustments.

The table below compares the applicable dollar limits for HSAs, HDHPs and excepted benefit HRAs for 2021 and 2022.

This week the IRS released two new sets of rules impacting Section 125 Cafeteria Plans. Notice 2020-33 provides permanent rule changes that include an increase in the amount of unused benefits that Health FSA plans may allow plan participants to rollover from one plan year to the next. Notice 2020-29 provides temporary rules designed to improve employer sponsored group health benefits for eligible employees in response to the coronavirus pandemic. The relief provided under each notice is optional for employers. Employers who choose to take advantage of any of the offered plan options will be required to notify eligible employees and will eventually be required to execute written plan amendments.

Notice 2020-33 modifies the amount of annual rollover of unused benefits that Health FSA plans may offer to Plan participants. Up until now, rollovers have been limited to $500 per Plan Year. The new rule sets the annual rollover limit to 20% of the statutory maximum annual employee Health FSA contribution for the applicable Plan Year. Because the statutory maximum is indexed for inflation, most years it increases (in mandated increments of $50).

The notice provides that the increased rollover amount may apply to Plan Years beginning on or after January 1, 2020. Because the corresponding annual Health FSA employee contribution limit for those Plan Years is $2,750, the annual rollover limit may be increased up to $550.

The relief provided under Notice 2020-29 falls into two major categories, both of which apply only for calendar year 2020. First, the IRS introduces several significant exceptions to the mid-year change of election rules generally applicable to Section 125 Cafeteria Plans. Second, the notice contains a special grace period which offers Health Flexible Spending Arrangement (FSA) and Dependent Care Assistance Program (DCAP) Participants additional time to incur eligible expenses during 2020.

The temporary exceptions to mid-year participant election change rules for 2020 authorize employers to allow employees who are eligible to participate in a Section 125 Cafeteria Plan to:

None of the above described election changes require compliance with the consistency rules which typically apply for mid-year Section 125 Cafeteria Plan election changes. They also do not require a specific impact from the coronavirus pandemic for the employee.

Employers have the ability to limit election changes that would otherwise be permissible under the exceptions permitted by Notice 2020-29 so long as the limitations comply with the Section 125 non-discrimination rules. For allowable Health FSA or DCAP election changes, employers may limit the amount of any election reduction to the amount previously reimbursed by the plan. Interestingly, even though new elections to make Health FSA and DCAP contributions may not be retroactive, Notice 2020-29 provides that amounts contributed to a Health FSA after a revised mid-year election may be used for any medical expense incurred during the first Plan Year that begins on or after January 1, 2020.

For the election change described in item 3 above, the enrolled employee must make a written attestation that any coverage being dropped is being immediately replaced for the applicable individual. Employers are allowed to rely on the employee’s written attestation without further documentation unless the employer has actual knowledge that the attestation is false.

The special grace period introduced in Notice 2020-29 allows all Health FSAs and DCAPs with a grace period or Plan Year ending during calendar year 2020 to allow otherwise eligible expenses to be incurred by Plan Participants until as late as December 31, 2020. This temporary change will provide relief to non-calendar year based plans. Calendar year Health FSA plans that offer rollovers of unused benefits will not benefit from this change.

The notice does clarify that this special grace period is permitted for non-calendar year Health FSA plans even if the plan provides rollover of unused benefits. Previous guidance had prohibited Health FSA plans from offering both grace periods and rollovers but Notice 2020-29 provides a limited exception to that rule.

The notice raises one issue for employers to consider before amending their plan to offer the special grace period. The special grace period will adversely affect the HSA contribution eligibility of individuals with unused Health FSA benefits at the end of the standard grace period or Plan Year for which a special grace period is offered. This will be of particular importance for employers with employees who may be transitioning into a HDHP group health plan for the first time at open enrollment.

As mentioned above, employers wishing to incorporate any of the allowable changes offered under Notices 2020-29 and 2020-33 will be required to execute written amendments to their Plan Documents and the changes should be reflected in the Plan’s Summary Plan Description and/or a Summary of Material Modification. Notice 2020-29 requires that any such Plan Amendment must be executed by the Plan Sponsor no later than December 31, 2021.

The Coronavirus Aid, Relief, and Economic Security Act (CARES ACT) was signed into law by the President on Friday.

There are three direct inclusions that immediately expand the usage of health savings accounts (HSA), flexible spending accounts (FSA), and health reimbursement arrangements (HRA) for employees.

1. Telehealth services can now be covered pre-deductible under a High Deductible Health Plan. The end date of this provision is Dec 21, 2021.

2. Over the counter (OTC) drugs and medicines are now eligible for reimbursement from an HSA, FSA or HRA. This is a permanent change.

3. Menstrual products are now eligible for reimbursement from an HSA, FSA or HRA. This is a permanent change.

The IRS has recently issued Notice 2019-45, which increases the scope of preventive care that can be covered by a high deductible health plan (“HDHP”) without eliminating the covered person’s ability to maintain a health savings account (“HSA”).

Since 2003, eligible individuals whose sole health coverage is a HDHP have been able to contribute to HSAs. The contribution to the HSA is not taxed when it goes into the HSA or when it is used to pay health benefits. It can for example be used to pay deductibles or copays under the HDHP. But it can also be used as a kind of supplemental retirement plan to pay Medicare premiums or other health expenses in retirement, in which case it is more tax-favored than even a regular retirement plan.

As the name suggests, a HDHP must have a deductible that exceeds certain minimums ($1,350 for self-only HDHP coverage and $2,700 for family HDHP coverage for 2019, subject to cost of living changes in future years). However, certain preventive care (for example, annual physicals and many vaccinations) is covered without having to meet the deductible. In general, “preventive care” has been defined as care designed to identify or prevent illness, injury, or a medical condition, as opposed to care designed to treat an existing illness, injury, or condition.

Notice 2019-45 expands the existing definition of preventive care to cover medical expenses which, although they may treat a particular existing chronic condition, will prevent a future secondary condition. For example, untreated diabetes can cause heart disease, blindness, or a need for amputation, among other complications. Under the new guidance, a HDHP will cover insulin, treating it as a preventative for those other conditions as opposed to a treatment for diabetes.

The Notices states that in general, the intent was to permit the coverage of preventive services if:

The Notice is in general good news for those covered by HDHPs. However, it has two major limitations:

Given the expansion of the types of preventive coverage that a HDHP can cover, and the tax advantages of an HSA to employees, employers who have not previously implemented a HDHP or HSA may want to consider doing so now. However, as with any employee benefit, it is important to consider both the potential demand for the benefit and the administrative cost.