Page 1 of 1

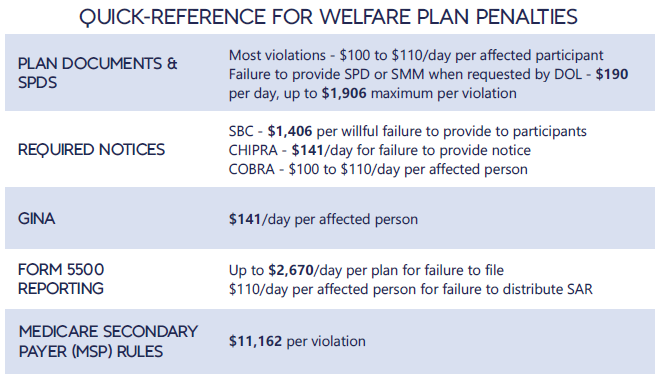

Each year in mid January, the Department of Labor (DOL) adjusts ERISA penalty amounts to account for inflation. This year’s increases are modest and amount to approximately 3%. Below summarizes a few of the penalty amounts that plan sponsors could see imposed on them for various federal law violations. The adjusted amounts apply to ERISA violations that occurred after November 2, 2015, if penalties are assessed after January 15, 2024, and before January 16, 2025.

*Notes: figures in bold are subject to annual adjustment

Below are the current inflation adjusted penalty amounts for failure to file forms 1094 and 1095 with the IRS and failure to provide form 1095 to applicable employees. Both penalties increase to $630 per form if failure is due to “intentional disregard” (criminal penalties may also apply).

In furtherance of the Biden Administration’s January 28, 2021, Executive Order 14009 and April 5, 2022, Executive Order 14070 to protect and strengthen the ACA, the Treasury Department and IRS published a proposed rule on April 7, 2022, advancing an alternative interpretation of Internal Revenue Code Section 36B. Employers can breathe a sigh of relief as the proposed changes do not alter the Employer Shared Responsibility Payment (ACA penalty) construct. Employers can continue to offer affordable employee-only coverage and spousal or dependent coverage that is unaffordable. However, the potential indirect effects of the proposed regulations on employers are noteworthy.

At its core, the proposed regulation eliminates the current regulatory concept that the cost of coverage for a spouse and dependent children is deemed affordable if the lowest-cost silver plan for employee-only coverage is affordable. Citing studies addressing the “family glitch” that disqualifies employees from subsidized Marketplace coverage if the employee-only coverage is affordable and finding this inconsistent with the purpose of the ACA of expanding access to affordable care, the Treasury Department and IRS have reinterpreted Section 36B as permitting a Premium Tax Credit to individuals if the only coverage available to them is unaffordable spousal or dependent coverage.

In an attempt to calm employers’ concerns that this proposed rule will affect their cost-sharing schedules, the Preamble to the proposed rule notes:

The proposed regulations would make changes only to the affordability rule for related individuals; they would make no changes to the affordability rule for employees. As required by statute, employees continue to have an offer of affordable employer coverage if the employee’s required contribution for self-only coverage of the employee does not exceed the required contribution percentage of household income. Accordingly, under the proposed regulations, a spouse or dependent of an employee may have an offer of employer coverage that is unaffordable even though the employee has an affordable offer of self-only coverage.

The proposed rule also modifies the minimum value regulations to include the entire family and addresses multiple offers of coverage.

Although not directly affecting employer-sponsored plans, employers may experience indirect effects of the changes if the proposed rule is finalized. For example, in order for the Internal Revenue Service to make Premium Tax Credit determinations involving family coverage, they may require further information reporting from employers. The IRS Forms 1094 and 1095 might be modified to require separate affordability reporting regarding both employee-only coverage and other coverage offers.

Further, employer-sponsored plans may see an uptick in enrollment if the Premium Tax Credit becomes available to families when employer-sponsored coverage is unaffordable for spouses and dependent children. The Premium Tax Credit would help offset the high cost of coverage in employer-sponsored plans.

With the protection and strengthening of the Affordable Care Act being a focus of the current Administration, employers should prepare for further changes.

The IRS has issued relief from certain Form 1094-C and 1095-C reporting requirements under the Affordable Care Act relating to employee health plans, as well as relief from certain reporting-related penalties.

As a refresher, the ACA generally requires four forms to be produced each year, and the names are anything but intuitive:

Which form your plan would be required to file or furnish depends on whether you are an ALE, and how you fill out the form and whether you offer fully insured or self-insured coverage.

The IRS has extended the deadline for furnishing Forms 1095-B and 1095-C to individuals. The typical deadline to report 2020 plan information is January 31, 2021. However, the new relief extends the deadline to March 2, 2021. The extension is automatic, and the IRS has indicated that no further extensions will be granted, and it will not respond to such requests.

Be aware that this extension does not apply to the 1094-B and 1094-C filings with the IRS. The deadline for submitting these filings to the IRS will remain March 1, 2021 (since the original due date of February 28 falls on a Sunday), for paper filings and March 31, 2021, for those filing electronically. However, while the automatic extension does not apply to these deadlines, filers may still request an extension from the IRS.

Recognizing that the main purpose of Forms 1095-B and 1095-C was to allow an individual to compute his or her tax liability relating to the individual mandate, and because the individual mandate has been reduced to zero, the IRS has granted relief from furnishing certain documents to individuals.

The IRS indicated that it will not assess penalties for failure to furnish a Form 1095-B if two conditions are met. First, the reporting entity must post a prominent notice on its website stating that individuals may receive a copy of their 2020 Form 1095-B upon request, along with an email address, physical address, and phone number. Second, the reporting entity must furnish the 2020 Form 1095-B to the responsible individual within 30 days of receipt of the request. The statements may be furnished electronically if certain additional requirements are met.

The same reporting relief does not extend to ALEs that are required to furnish Form 1095-C. This form must continue to be furnished to full-time employees, and penalties will continue to be assessed for a failure to furnish Form 1095-C. However, the relief does generally apply to furnishing the Form 1095-C to participants who were not full-time employees for any month of 2019 if the requirements above are met. This would typically include part-time employees, COBRA continuees, or retirees.

Note that while these requirements for furnishing the 1095-B and 1095-C to individuals has been modified, these forms must still be transmitted to the IRS along with their Form 1094 counterparts.

In the final piece of good news from the IRS, it announced relief from penalties for incorrect or incomplete information on any of these forms. This relief applies to both missing and inaccurate taxpayer identification numbers and birthdays, as well as other required information.

The reporting entity must be able to show that it made a good faith effort to comply with the reporting requirements. A successful showing of good faith will show that an employer made reasonable efforts to prepare for the reporting requirements and the furnishing to employees, such as gathering and transmitting the necessary information to the person preparing the forms.

However, the relief does not apply to reporting entities that completely fail to file or furnish the forms at all.

Finally, and importantly, the IRS has indicated that this will be the last year that it will provide this good faith reporting relief.