Page 1 of 1

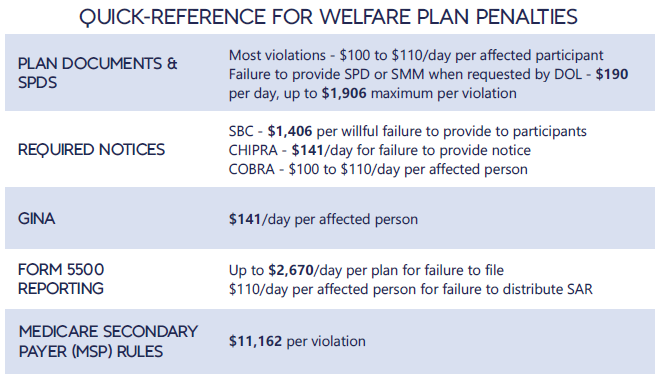

Each year in mid January, the Department of Labor (DOL) adjusts ERISA penalty amounts to account for inflation. This year’s increases are modest and amount to approximately 3%. Below summarizes a few of the penalty amounts that plan sponsors could see imposed on them for various federal law violations. The adjusted amounts apply to ERISA violations that occurred after November 2, 2015, if penalties are assessed after January 15, 2024, and before January 16, 2025.

*Notes: figures in bold are subject to annual adjustment

Below are the current inflation adjusted penalty amounts for failure to file forms 1094 and 1095 with the IRS and failure to provide form 1095 to applicable employees. Both penalties increase to $630 per form if failure is due to “intentional disregard” (criminal penalties may also apply).

In IRS Notice 2018-06, the IRS announced a 30-day automatic extension for the furnishing of 2017 IRS Forms 1095-B (Health Coverage) and 1095-C (Employer-Provided Health Insurance Offer and Coverage), from January 31, 2018 to March 2, 2018. This extension was made in response to requests by employers, insurers, and other providers of health insurance coverage that additional time be provided to gather and analyze the information required to complete the Forms and is virtually identical to the extension the IRS provided for furnishing the 2016 Forms 1094-C and 1095-C. Notwithstanding the extension, the IRS encourages employers and other coverage providers to furnish the Forms as soon as possible.

Notice 2018-06 does not extend the due date for employers, insurers, and other providers of minimum essential coverage to file 2017 Forms 1094-B, 1095-B, 1094-C and 1095-C with the IRS. The filing due date for these forms as it stands today remains February 28, 2018 (April 2, 2018, if filing electronically).

The IRS also indicates that, while failure to furnish and file the Forms on a timely basis may subject employers and other coverage providers to penalties, such entities should still attempt to furnish and file even after the applicable due date as the IRS will take such action into consideration when determining whether to abate penalties.

Additionally, the Notice provides that good faith reporting standards will apply once again for 2017 reporting. This means that reporting entities will not be subject to reporting penalties for incorrect or incomplete information if they can show that they have made good faith efforts to comply with the 2017 Form 1094 and 1095 information-reporting requirements. This relief applies to missing and incorrect taxpayer identification numbers and dates of birth, and other required return information. However, no relief is provided where there has not been a good faith effort to comply with the reporting requirements or where there has been a failure to file an information return or furnish a statement by the applicable due date (as extended).

Finally, an individual taxpayer who files his or her tax return before receiving a 2017 Form 1095-B or 1095-C, as applicable, may rely on other information received from his or her employer or coverage provider for purposes of filing his or her return.

In July 2015, President Obama signed into law the Trade Preferences Extension Act of 2015. Included in the bill was an important provision that affects welfare and retirement benefit plans. The Act sizably increases filing penalties for information return and statement failures under the Internal Revenue Code, effective for filings after December 31,2015. Employers now face significantly larger penalties for failing to correctly file and furnish the ACA forms 1094 and 1095 (shared responsibility reporting requirements) as well as Forms W-2 and 1099-R.

Background

Sections 6721 and 6722 of the IRC impose penalties associated with failures to file- or to file correct- information returns and statements. Section 6721 applies to the returns required to be filed with the IRS, and Section 6722 applies to statements required to be provided generally to employees.These penalty provisions apply to the ACA shared responsibility reporting Forms 1094-B, 1094-C, 1095-B, and 1095-C (Sections 6055 & 6056) failures as well as other information returns and statement failures, like those on Forms W-2 and 1099.

For ACA:

The Sections 6055 & 6056 reporting requirements are effective for medical coverage provided on or after January 1, 2015, with the first information returns to be filed with the IRS by February 29, 2016 (or March 31,2016 if filing electronically) and provided to individuals by February 1, 2016.

Increase in Penalties

The Trade Preferences Extension Act of 2015 (Act) contains several tax provisions in addition to the trade measures that were the focus of the bill. Provided as a revenue offset provision, the law significantly increases the penalty amounts under Sections 6721 and 6722. A failure includes failing to file or furnish information returns or statements by the due date, failing to provide all required information, as well as failing to provide correct information.

The law increases the penalty for:

Other penalty increase also apply, including those associated with timely filing a corrected return. Penalties could also provide a one-two punch under the ACA for employers and other responsible entities. For example, under Sec 6056, applicable large employers (ALE) must file information returns to the IRS (the 1094-B and 1094-C) as well as furnish statements to employees (the 1095-B and 1095-C). So incorrect information shared on those forms could result in a double penalty- one associated with the information return to the IRS and the other associated with individual statements to employees.

Final regulations on the ACA reporting requirements provide short-term relief from these penalties. For reports files in 2016 (for 2015 calendar year info), the IRS will not impose penalties on ALE members that can show they made a “good-faith effort” to comply with the information reporting requirements. Specifically, relief is provided for incorrect or incomplete info reported on the return or statement, including Social Security numbers, but not for failing to file timely.

Many employers originally thought they could shift health costs to the government by sending their employees to a health insurance Exchange/Marketplace with a tax-free contribution of cash to help pay premiums, but the Obama administration has squashed this idea in a new ruling. Such arrangements do not satisfy requirements under the Affordable Care Act (ACA), the Obama administration said, and employers could now be subject to a tax penalty of $100 a day — or $36,500 a year — for each employee who goes into the individual Marketplace/Exchange for health coverage.

The ruling this month, by the Internal Revenue Service, prevents any “dumping” of employees into the exchanges by employers.

Under a main provision in the health care law, employers with 50 or more employees are required to offer health coverage to full-time workers, or else the employer may be subject to penalties.

Many employers had concluded that it would be cheaper to provide each employee with a lump sum of money to buy insurance on an exchange, instead of providing employer-sponsored health coverage directly to employees as they had in the past.

But the Obama administration has now raised objections in an authoritative Q&A document recently released by the IRS, in consultation with other agencies.

The health law, known as the Affordable Care Act (ACA), was intended to build on the current system of employer-based health insurance. The administration wants employers to continue to provide coverage to workers and their families and do not see the introduction of ACA as an eventual erosion of employer provided coverage.

Employer contributions to sponsored health coverage, which averages more than $5,000 a year per employee, are not counted as taxable income to workers. But the IRS has said employers could not meet their obligations under ACA by simply reimbursing employees for some or all of their premium costs from the marketplace/exchange.

Christopher E. Condeluci, a former tax and benefits counsel to the Senate Finance Committee, said the recent IRS ruling was significant because it made clear that “an employee cannot use tax-free contributions from an employer to purchase an insurance policy sold in the individual health insurance market, inside or outside an exchange.”

If an employer wants to help employees buy insurance on their own, Condeluci said, they can give the employee higher pay, in the form of taxable wages. But in such cases, he said, the employer and the employee would owe payroll taxes on those wages, and the change could be viewed by workers as reducing a valuable benefit.

A tax partner from a large accounting firm has also said the ruling could disrupt reimbursement arrangements used in many industries.

For decades, many employers have been assisting employees by reimbursing them for health insurance premiums and out-of-pocket costs associated with their health coverage. The new federal ruling eliminates many of those arrangements, commonly known as Health Reimbursement Arrangements (HRAs) or employer payment plans, by imposing an unusually punitive penalty. The IRS has said that these employer payment plans are considered to be group health plans, but they do not satisfy requirements of the Affordable Care Act for health coverage.

Under the law, insurers may not impose annual limits on the dollar amount of benefits for any individual, and they must provide certain preventive services, like mammograms and colon cancer screenings, without co-payments or other charges.

But the administration has said that employer payment plans or HRAs do not meet these requirements.

This ruling was released as the Obama administration rushed to provide guidance to employers and insurers who are beginning to review coverage options for 2015.

The Department of Health and Human Services said it would provide financial assistance to certain insurers that experience unexpected financial losses this year. Administration officials hope the payments will stabilize medical premiums and prevent rate increases that are associated with the required policy changes as a result of ACA.

Republicans want to block these payments, however, as they see them as a bailout for insurance companies who originally supported the president’s health care law.

Stay tuned for more updates on ACA as they are released. Should you have any questions, please do not hesitate to contact our office.

Can corporations shift targeted workers who have known high medical costs from the company health plan to public exchange (aka Marketplace/SHOP) based coverage created by the Affordable Care Act? Some employers are beginning to inquire about it and some consultants are advocating for it.

Health spending is driven largely by those patients with chronic illness, such as diabetes, or those who undergo expensive procedures such as an organ transplant. Since a large majority of big corporations are self-insured and many more smaller employers are beginning to research this as an option to help control their medical premiums, shifting even one high-cost member out of the company health plan could potentially save the employer hundreds of thousands of dollars a year by shifting the cost for the high-cost member claims to the Marketplace/SHOP plan(s).

It is unclear if the health law prohibits this type of action, which opens a door to the potential deterioration of employer-based medical coverage.

An employer “dumping strategy” can help promote the interests of both employers and employees by shifting health care expenses on to the public through the Marketplace.

It’s unclear how many companies, if any, have moved any of their sicker workers to exchange coverage yet, which just became available January 1, 2014, but even a few high-risk patients could add millions of dollars in claim costs to those Marketplace plans. The costs could be passed on to customers in the next year or two in the form of higher premiums and to taxpayers in the form of higher subsidy expenses.

A Possible Scenario

Here’s an example of how an employer “dumping-situation” it might work:

At renewal, an employer reduces the hospital/doctor network on their medical plan to make the company health plan unattractive to those with chronic illness or high cost medical claims. Or, the employer could raise the co-payments for drugs or physician visits needed by the chronically ill, also making the health plan unattractive and perhaps nudging high-cost workers to examine other options available to them.

At the same time, the employer offers to buy the targeted worker a high-benefit “platinum” plan in the Marketplace. The Marketplace/SHOP plan could cost $6,000 or more a year for an individual in premiums, but that’s still far less than the $300,000 a year in claim costs that a hemophilia patient might cost the company.

The employer could also give the worker a raise so they could buy the Marketplace/SHOP policy directly.

In the end, the employer saves money and the employee gets better coverage. And the Affordable Care Act marketplace plan, which is required to accept all applicants at a fixed price during open enrollment periods, takes over the costs for their chronic illness/condition.

Some consultants feel the concept sounds too easy to be true, but the ACA has set up the ability for employers and employees to voluntarily choose a better plan in the Individual Marketplace which could help save a significant amount of money for both.

Legal but ‘Gray’

The consensus among insurance and HR professionals is that even though the employer “dumping-strategy” is technically legal to date (as long as employees agree to the change and are not forced off the company medical plan), the action is still very gray. This is why many employers have decided this is not something they want to promote at this time.

Shifting high-risk workers out of employer medical plans is prohibited for other kinds of taxpayer-supported insurance. For example, it’s illegal to persuade an employee who is working and over 65 to drop company coverage and rely entirely on the government Medicare program. Similarly, employers who dumped high-cost patients into temporary high-risk pools established originally by the ACA health law are required to repay those workers’ claims back to the pools.

One would think there would be a similar type of provision under the Affordable Care Act for plans sold through the Marketplace portals, but there currently is not.

The act of moving high-cost workers to a Marketplace plan would not trigger penalties under ACA as long as an employer offers an affordable medical plan to all eligible employees that meets the requirements of minimum essential coverage, experts said. If workers are offered a medical plan by their employer that is affordable coverage and meets the minimum essential coverage requirements, workers cannot use tax credits to help pay for the Marketplace-plan premiums.

Many benefits experts say they are unaware of specific instances where employers are shifting high-cost workers to exchange plans and the spokespeople for AIDS United and the Hemophilia Federation of America, both advocating for patients with expensive, chronic conditions, said they didn’t know of any, either.

But employers are becoming increasingly interested in this option.

This practice, however, could raise concerns about discrimination and could cause decreased employee morale and even resentment among employees who are not offered a similar deal, which could end up causing the employer more headaches and even potential discrimination lawsuits.

Many believe that even though this strategy is currently an option for employers, in the end, it may not be a good idea. This type of strategy has to operate as an under-the-radar deal between the employer and targeted employee and these type of deals never work out. Most legal experts who focus on employee benefits do not recommend this strategy either as it just opens the door of discrimination claims from employees.

Please contact our office for assistance in reviewing all of the benefit options available to your company and employees under ACA.

If you currently have an individual health insurance plan, you will be in for a big change when you sign up for your coverage in 2014.

Approximately 50% of the individual health plans that are currently being sold in the marketplace do not meet the standards of Obamacare to be sold in 2014. The reason for this is because the Affordable Care Act (ACA) sets new minimums for the basic coverage every individual health care plan must provide effective on renewals on or after January 1, 2014.

About 15 million Americans (or about 6% of non-elderly adults) currently have coverage in the individual health market. Beginning in the fall of 2013, they will be able to shop for and enroll in health insurance through state-based exchanges (aka SHOP or The Exchange) with coverage taking effect in January. By 2016, it is projected that around 24 million people will get their insurance through the exchanges, while another 12 million will continue to obtain individual coverage outside of the exchange.

Beginning in 2014, nearly all plans, both group and individual, will be required to cover an array of “essential” services regardless of if they are purchased within the exchange or not. These “essential” services will include medication, maternity, and mental health care. Many individual plans do not currently offer these benefits.

What will happen to the plans that do not meet the new minimum standards? They will more than likely disappear and you will not be allowed to renew your existing coverage on the plan you currently have. A handful of existing plans will be grandfathered in, but the qualifying criteria for a grandfathered plan is hard to meet. In order for your existing individual plan to be considered “grandfathered”, (1) you have to have been enrolled on this plan before the ACA was passed in 2010 and (2) the plan has to have maintained fairly steady co-pay, deductible and coverage rates until now.

Many insurers in the individual marketplace have already acknowledged that the majority of their existing individual plans do not meet Obamacare standards for 2014 and they are currently working to ready new product lineups for 2014.

In the future, consumers buying individual plans will be able to choose between four levels of coverage: platinum, gold, silver, and bronze.

Platinum plans will carry the highest premiums but will offer the lowest out of pocket expenses, with enrollees paying no more than 10%, on average. At the other end of the spectrum are the bronze plans, which will have the lowest monthly premiums but will have higher deductibles and copayments totaling up to 40% of the out of pocket costs on average.

Starting also in 2014, all Americans will be required to carry health care coverage or face fines. Those penalties will start at $95 per adult or 1% of the adjusted family income, whichever is greater, and will escalate in later years.

Individuals will annual incomes of up to 400% of the poverty line (or roughly $45,000 for an individual and about $92,000 for a family of four) will get federal subsidies to help defray the premium costs.

Most individual plans sold next year, even the lowest level bronze plans, are likely to charge higher premiums than today’s most “bare-bones” individual insurance plans. Many consumers feel the costs will be offset by having lower out of pocket costs and more comprehensive coverage than their current “bare-bones” plan offers.

In today’s marketplace, with deductibles of $10,000, an individual can buy a policy and then when they get sick, they may go broke because the policy leaves them with such a high level of out of pocket expenses to pay. Many insurance industry experts feel, however, that consumers may now wind up with more coverage–and higher monthly costs– than they want. As a result, some individuals may just choose to simply pay the fine instead of obtaining health insurance coverage they will not use or can not afford.

Our topic this month covers the Final Rule from HHS and the Exchanges.

Areas discussed include:

Contact us today for more information on this topic.