Page 1 of 1

The Trump administration announced a proposed rule today that would allow businesses to give employees money to purchase health insurance on the individual marketplace, a move senior officials say will expand choices for employees that work at small businesses.

The proposed rule, issued by the Department of Health and Human Services (HHS), the Department of Labor (DOL) and the Department of Treasury, would restructure Obama-era regulations that limited the use of employer-funded accounts known as health reimbursement arrangements (HRA). The proposal is part of President Donald Trump’s “Promoting Healthcare Choice and Competition” executive order issued last year, which tasked the agencies with expanding the use of HRAs.

Senior administration officials said the proposed change would bring more competition to the individual marketplace by giving employees the chance to purchase health coverage on their own. The rule includes “carefully constructed guardrails” to prevent employers from keeping healthy employees on their company plans and incentivizing high-cost employees to seek coverage elsewhere.

That issue was a primary concern under the Obama administration, which barred the use of HRAs for premium assistance. The 21st Century Cures Act established Qualified Small Employer Health Reimbursement Accounts (QSEHRA), but those are subject to stringent limitations.

Under the new rule, HRA money would remain exempt from federal and payroll income taxes for employers and employees. Additionally, employers with traditional coverage would be permitted to reserve $1,800 for supplemental benefits like vision, dental and short-term health plans.

Officials estimate 10 million people would purchase insurance through HRAs, including 1 million people that were not previously insured. Most of those people would be concentrated in small and mid-sized businesses.

The proposed change would “unleash consumerism” and “spur innovation among providers and insurers that directly compete for consumer dollars,” one senior official said. Officials expect 7 million people will be added to the individual marketplace over the next 10 years.

The rule does not change the Affordable Care Act’s employer mandate, which requires employers with 50 or more employees to offer coverage to 95% of full-time employees. Administration officials expect the proposal will have the biggest impact on small businesses with less than 50 employees.

However, the rule could scale back the use of premium subsidies. If the HRA is considered “affordable” based on the amount provided by the employer, the employee would not be eligible for a premium tax credit. If the HRA fails to meet those minimum requirements, the employee could choose between a premium tax credit and the HRA.

Overall, the rule will “create a greater degree of value in healthcare and the health benefits marketplace than we would otherwise see,” one official said.

The regulation, if finalized, is proposed to be effective for plan years beginning on and after January 1, 2020.

Beginning January 1, 2015, employers have new reporting obligations for health plan coverage, to allow the government to administer the “pay or play” penalties to be assessed against employers that do not offer compliant coverage to their full-time employees.

Even though the penalties only apply if there are 100 or more employees for 2015, employers with 50 or more full-time equivalent employees are required to report for 2015. Also, note this reporting is required even if the employer does not maintain any health plan.

Employers that provide self-funded group health coverage also have reporting obligations, to allow the government to administer the “individual mandate” which results in a tax on individuals who do not maintain health coverage.

These reporting obligations will be difficult for most employers to implement. Penalties for non-compliance are high, so employers need to begin now with developing a plan on how they will track and file the required information.

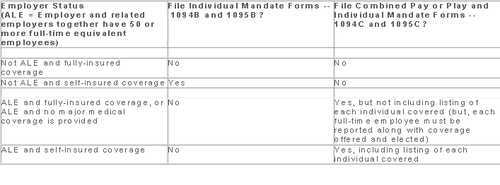

Pay or Play Reporting. Applicable large employers (ALEs) must report health coverage offered to employees for each month of 2015 in an annual information return due early in 2016. ALEs are employers with 50 or more full-time equivalent (FTE) employees. Employees who average 30 hours are counted as one, and those who average less than 30 hours are combined into an equivalent number of 30 hour employees to determine if there are 50 or more FTE employees. All employees of controlled group, or 80% commonly owned employers, are also combined to determine if the 50 FTE threshold is met.

Individual Mandate Reporting. Self-funded employers, including both ALEs and small employers that are not ALEs, must report each individual covered for each month of the calendar year. For fully-insured coverage, the insurance carrier must report individual month by month coverage. The individual mandate reporting is due early in 2016 for each month of 2015.

Which Form? ALE employers have one set of forms to report both the pay or play and the individual mandate information – Forms 1094C and 1095C. Insurers and self-insured employers that are not ALEs use Forms 1094B and 1095B to report the individual mandate information. Information about employee and individual coverage provided on these forms must also be reported by the employer to its employees as well as to COBRA and retiree participants. Forms 1095B and 1095C can be used to provide this information, or employers can provide the information in a different format.

The following chart summaries which returns are filed by employers:

Who Reports? While ALE status is determined on a controlled group basis, each ALE must file separate reports. Employers will need to provide insurance carriers, and third party administrators who process claims for self-funded coverage (if they will assist the employer with reporting), accurate data on the employer for whom each covered employee works. If an employee works for more than one ALE in a controlled group, the employer for whom the highest number of hours is worked does the reporting for that employee.

Due Date for Filing. The due date of the forms matches the due dates of Forms W-2, and employers may provide the required employee statements along with the W-2. Employee reporting is due January 31st and reporting to the IRS is due each February 28th, although the date is extended until March 31st if the forms are filed electronically. If the employer files 250 or more returns, the returns must be filed electronically. Reporting to employees can only be made electronically if the employee has specifically consented to receiving these reports electronically.

Penalties. Failure to file penalties can total $200 per individual for whom information must be reported, subject to a maximum of $3 million per year. Penalties will not be assessed for employers who make a good faith effort to file correct returns for 2015.

What Information is Required? For the pay or play reporting, each ALE must file a Form 1094C reporting the number of its full-time employees (averaging 30 hours) and total employees for each calendar month, whether the ALE is in a “aggregated” (controlled) group, a listing of the name and EIN of the top 30 other entities in the controlled group (ranked by number of full-time employees), and any special transition rules being used for pay or play penalties. ALE’s must also file a 1095C for each employee who was a full-time employee during any calendar month of the year. The 1095C includes the employee’s name, address and SSN, and month by month reporting of whether coverage was offered to the employee, spouse and dependents, the lowest premium for employee only coverage, and identification of the safe-harbor used to determine affordability. This information is used to determine pay or play penalty taxes and to verify the individuals’ eligibility for subsidies toward coverage costs on the Federal and state exchanges.

If the ALE provides self-funded coverage, the ALE must also report on the 1095C the name and SSN of each individual provided coverage for each calendar month. If an employer is not an ALE, but is self-funded, the name and SSN of each covered individual is reported on the 1095B and the 1094B is used to transmit the forms 1095B to the IRS.

A chart is available that sets out what data must be reported on each form, to help employers determine what information they need to track. Click here to access the chart.

Next Steps. Employers will need to determine how much help their insurance carrier or TPA can provide with the reporting, and then the employer’s HR, payroll and IT functions will need to work together to be sure the necessary information is being tracked and can be produced for reporting in January 2016.

Members of the U.S. House of Representatives voted on January 8, 2015 to redefine full-time employment under the Affordable Care Act (ACA) to employees who work at least 40 hours a week rather than 30 hours a week.

The Save American Workers Act, passed the House with a vote of 252-172 with full Republican support and 12 Democratic voters. The legislation would amend the Internal Revenue Code by changing the definition of full-time employee to cover individuals who work, on average, at least 40 hours per week for purposes of the employer mandate to provide minimum essential health care coverage under the ACA.

Despite the bill’s passage in the House, the fate of the bill in the U.S. Senate remains uncertain. In addition, Republicans have not garnered enough support to override the veto promised by President Obama if the bill did pass Congress.

According to Politico, “The House has cleared more than 50 assorted measures to repeal or roll back Obamacare, but this is the first time the House can propel legislation to a GOP-controlled Senate, potentially forcing President Barack Obama to either accept changes to his signature domestic achievement or use his veto power.”

Some supporters of the change, including the U.S. Chamber of Commerce, argue that the current standard deviates from the widely accepted definition of full-time work. It is argued that it provides an incentive for employers to reduce hours, particularly for low-wage workers, to avoid offering healthcare coverage.

This month, employers with 100 or more employees will be required to offer health insurance to at least 70% of employees who works at least 30 hours a week or else pay a penalty.

The NY Times comments:

By adjusting that threshold to 40 hours, Republicans — strongly backed by a number of business groups — said that they would re-establish the traditional 40-hour workweek and prevent businesses cutting costs from radically trimming worker hours to avoid mandatory insurance coverage. They contend that the most vulnerable workers are low-skilled and underpaid, working 30 to 35 hours a week, and now facing cuts to 29 hours or less so their employers do not have to insure them. With passage of the law, those workers would not have to get employer-sponsored health care, and their workweek would remain intact.

Analysis by the Congressional Budget Office found that the bill would increase the U.S. deficit by $53 billion over the course of a decade because fewer employers would pay penalties and one million employees would not have coverage through their job. Democrats cite these reasons as evidence that the bill is simply an attempt to dismantle the ACA.

A central issue of this bill is how far employers would go to avoid mandated coverage. A majority of employees already work 40 hours a week rather than 30. That being said, few employers would cut worker hours from 40 to 29, but many would be willing to cut hours from 40 to 39, the New York Times ventures, “That means raising the definition of a full-time worker under the health care law would put far more workers at risk.”

The Affordable Care Act (ACA) imposes significant information reporting responsibilities on employers starting with the 2015 calendar year. One reporting requirement applies to all employer-sponsored health plans, regardless of the size of the employer. A second reporting requirement applies only to large employers, even if the employer does not provide health coverage. The IRS is currently developing new systems for reporting the required information and recently released draft forms, however instructions have yet to be released.

Information returns

The new information reporting systems will be similar to the current Form W-2 reporting systems in that an information return (Form 1095-B or 1095-C) will be prepared for each applicable employee, and these returns will be filed with the IRS using a single transmittal form (Form 1094-B or 1094-C). Electronic filing is required if the employer files at least 250 returns. Employers must file these returns annually by Feb. 28 (March 31 if filed electronically). Therefore, employers will be filing these forms for the 2015 calendar year by Feb. 28 or March 31, 2016 respectively. A copy of the Form 1095, or a substitute statement, must be given to the employee by Jan. 31 and can be provided electronically with the employee’s consent. Employers will be subject to penalties of up to $200 per return for failing to timely file the returns or furnish statements to employees.

The IRS released drafts of the Form 1095-B and Form 1095-C information returns, as well as the Form 1094-B and Form 1094-C transmittal returns, in July 2014 and is expected to provide instructions for the forms in August 2014. According to the IRS, both the forms and the instructions will be finalized later this year.

Health coverage reporting requirement

The health coverage reporting requirement is designed to identify employees and their family members who are enrolled in minimum essential health coverage. Employees who are offered coverage, but decline the coverage, are not reported. The IRS will use this information to determine whether the employees are exempt from the individual mandate penalty due to having health coverage for themselves and their family members.

Insurance companies will prepare Form 1095-B (Health Coverage) and Form 1094-B (Transmittal of Health Coverage Information Returns) for individuals covered by fully-insured employer-sponsored group health plans. Small employers with self-insured health plans will use Form 1095-B and Form 1094-B to report the name, address, and Social Security number (or date of birth) of employees and their family members who have coverage under the self-insured health plan. However, large employers (as defined below) with self-insured health plans will file Forms 1095-C and 1094-C in lieu of Forms 1095-B and 1094-B.

Large employer reporting requirement

“Applicable large employer members (ALE)” are subject to the reporting requirement if they offer an insured or self-insured health plan, or do not offer any group health plan. ALE members are those employers that are either an applicable large employer on their own or are members of a controlled or affiliated service group with an ALE (regardless of the number of employees of the group member). ALEs are those that had, on average, at least 50 full-time employees (including full-time equivalent “FTE” employees) during the preceding calendar year. Full-time employees are those who work, on average, at least 30 hours per week. Employers with fewer than 50 full-time employees and equivalents are not applicable large employers and, thus, are exempt from this health coverage reporting requirement.

As referenced above, an employer’s status as an ALE is determined on a controlled or affiliated service group basis. For example, if Company A and Company B are members of the same controlled group and Company A has 100 employees and Company B has 20 employees, then A and B are both members of an ALE. Consequently, Company A and Company B must each file the information returns.

Each ALE member must file Form 1095-C (Employer-Provided Health Insurance Offer and Coverage) and Form 1094-C (Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns) with the IRS for each calendar year. The IRS will use this information to determine whether (1) the employer is subject to the employer mandate penalty, and (2) an employee is eligible for a premium tax credit on insurance purchased through the new health insurance exchange. ALEs with fewer than 100 full-time employees are generally eligible for transition relief from the employer mandate penalty for their 2015 plan year. Nonetheless, these employers are still required to file Forms 1095-C and 1094-C for the 2015 calendar year.

The employer mandate penalty can be imposed on any ALE member that does not offer affordable, minimum value health coverage to all of its full-time employees starting in 2015. Health coverage is affordable if the amount that the employer charges an employee for self-only coverage does not exceed 9.5 percent of the employee’s Form W-2 wages, rate of pay, or the federal poverty level for the year. A health plan provides minimum value if the plan is designed to pay at least 60 percent of the total cost of medical services for a standard population. In the case of a controlled or affiliated service group, the employer mandate penalties apply to each member of the group individually.

ALE members must prepare a Form 1095-C for each employee. The return will report the following information:

An ALE member will file with the IRS one Form 1094-C transmitting all of its Forms 1095-C. The Form 1094-C will report the following information:

As noted above, each ALE member is required to file Forms 1095-C and 1094-C for its own employees, even if it participates in a health plan with other employers (e.g., when the parent company sponsors a plan in which all subsidies participate). Special rules apply to multiemployer plans for collectively-bargained employees.

Action required

In light of the complexity of the new information reporting requirements, it is recommended that employers should begin taking steps now to prepare for the new reporting requirements:

Many employers originally thought they could shift health costs to the government by sending their employees to a health insurance Exchange/Marketplace with a tax-free contribution of cash to help pay premiums, but the Obama administration has squashed this idea in a new ruling. Such arrangements do not satisfy requirements under the Affordable Care Act (ACA), the Obama administration said, and employers could now be subject to a tax penalty of $100 a day — or $36,500 a year — for each employee who goes into the individual Marketplace/Exchange for health coverage.

The ruling this month, by the Internal Revenue Service, prevents any “dumping” of employees into the exchanges by employers.

Under a main provision in the health care law, employers with 50 or more employees are required to offer health coverage to full-time workers, or else the employer may be subject to penalties.

Many employers had concluded that it would be cheaper to provide each employee with a lump sum of money to buy insurance on an exchange, instead of providing employer-sponsored health coverage directly to employees as they had in the past.

But the Obama administration has now raised objections in an authoritative Q&A document recently released by the IRS, in consultation with other agencies.

The health law, known as the Affordable Care Act (ACA), was intended to build on the current system of employer-based health insurance. The administration wants employers to continue to provide coverage to workers and their families and do not see the introduction of ACA as an eventual erosion of employer provided coverage.

Employer contributions to sponsored health coverage, which averages more than $5,000 a year per employee, are not counted as taxable income to workers. But the IRS has said employers could not meet their obligations under ACA by simply reimbursing employees for some or all of their premium costs from the marketplace/exchange.

Christopher E. Condeluci, a former tax and benefits counsel to the Senate Finance Committee, said the recent IRS ruling was significant because it made clear that “an employee cannot use tax-free contributions from an employer to purchase an insurance policy sold in the individual health insurance market, inside or outside an exchange.”

If an employer wants to help employees buy insurance on their own, Condeluci said, they can give the employee higher pay, in the form of taxable wages. But in such cases, he said, the employer and the employee would owe payroll taxes on those wages, and the change could be viewed by workers as reducing a valuable benefit.

A tax partner from a large accounting firm has also said the ruling could disrupt reimbursement arrangements used in many industries.

For decades, many employers have been assisting employees by reimbursing them for health insurance premiums and out-of-pocket costs associated with their health coverage. The new federal ruling eliminates many of those arrangements, commonly known as Health Reimbursement Arrangements (HRAs) or employer payment plans, by imposing an unusually punitive penalty. The IRS has said that these employer payment plans are considered to be group health plans, but they do not satisfy requirements of the Affordable Care Act for health coverage.

Under the law, insurers may not impose annual limits on the dollar amount of benefits for any individual, and they must provide certain preventive services, like mammograms and colon cancer screenings, without co-payments or other charges.

But the administration has said that employer payment plans or HRAs do not meet these requirements.

This ruling was released as the Obama administration rushed to provide guidance to employers and insurers who are beginning to review coverage options for 2015.

The Department of Health and Human Services said it would provide financial assistance to certain insurers that experience unexpected financial losses this year. Administration officials hope the payments will stabilize medical premiums and prevent rate increases that are associated with the required policy changes as a result of ACA.

Republicans want to block these payments, however, as they see them as a bailout for insurance companies who originally supported the president’s health care law.

Stay tuned for more updates on ACA as they are released. Should you have any questions, please do not hesitate to contact our office.

One of the ways in which the Affordable Care Act helps bring down costs for small employers is through the tax credit available to eligible small businesses that provide health care insurance to their employees. The credit significantly offsets the cost of providing insurance and with the 2012 corporate tax filing deadline rapidly approaching (March 15th), you don’t want to let this valuable tax break pass you by.

What is the Small Business Health Care Tax Credit?

Currently the maximum tax credit is 35% for small businesses employers and 25% for small tax-exempt employers (i.e. charities and non-profits). This percentage applies to tax years 2010 through 2013. Even better, in 2014 the credit will increase to 50% for eligible small business employers and up to 35% for tax-exempt employers through the new Small Business Health Options Program (SHOP) Marketplace (also known as the Exchange).

The credit can also be carried back or forward to other tax years. Since the amount of the health insurance premium payments are more than the total credit, eligible businesses can still claim a business expense deduction for the premiums in excess of the credit. That equals out to both a credit and a deduction for employee premium payments.

Who Qualifies for the Small Business Health Care Tax Credit?

To qualify for the credit, you must meet the following criteria:

To help determine whether you qualify for the credit, follow this step by step guide from the IRS.

How to Claim the Credit

You must use the IRS Form 8941 to calculate the credit.. Then include the credit amount as part of the general business credit on your income tax return. If you are a tax-exempt organization, include the amount on line 44f of the Form 990-T. You must file the Form 990-T in order to claim the credit even if you do not ordinarily do so. Remember, you may be able to carry the credit back or forward. Be sure to talk to your tax advisor for more assistance.

The Patient Protection and Affordable Care Act (the “ACA”) adds a new Section 4980H to the Internal Revenue Code of 1986 which requires employers to offer health coverage to their employees (aka the “Employer Mandate”). The following Q&As are designed to deal with commonly asked questions. These Q&As are based on proposed regulations and final regulations, when issued, may change the requirements.

Question 1: What Is the Employer Mandate?

On January 1, 2014, the Employer Mandate will requiring large employers to offer health coverage to full-time employees and their children up to age 26 or risk paying a penalty. These employers will be forced to make a choice:

OR

This “play or pay” system has become known as the Employer Mandate. The January 1, 2014 effective date is deferred for employers with fiscal year plans that meet certain requirements.

Only “large employers” are required to comply with this mandate. Generally speaking, “large employers” are those that had an average of 50 or more full-time or full-time equivalent employees on business days during the preceding year. “Full-time employees” include all employees who work at least 30 hours on average each week. The number of “full-time equivalent employees” is determined by combining the hours worked by all non-full-time employees.

To “play” under the Employer Mandate, a large employer must offer health coverage that is:

This includes coverage under an employer-sponsored group health plan, whether it be fully insured or self-insured, but does not include stand-alone dental or vision coverage, or flexible spending accounts (FSA).

Coverage is considered “affordable” if an employee’s required contribution for the lowest-cost self-only coverage option does not exceed 9.5% of the employee’s household income. Coverage provides “minimum value” if the plan’s share of the actuarially projected cost of covered benefits is at least 60%.

If a large employer does not “play” for some or all of its full-time employees, the employer will have to pay a penalty, as shown in following two scenarios.

Scenario #1- An employer does not offer health coverage to “substantially all” of its full-time employees and any one of its full-time employees both enrolls in health coverage offered through a State Insurance Exchange, which is also being called a Marketplace (aka an “Exchange”), and receives a premium tax credit or a cost-sharing subsidy (aka “Exchange subsidy”).

In this scenario, the employer will owe a “no coverage penalty.” The no coverage penalty is $2,000 per year (adjusted for inflation) for each of the employer’s full-time employees (excluding the first 30). This is the penalty that an employer should be prepared to pay if it is contemplating not offering group health coverage to its employees.

Scenario #2- An employer does provide health coverage to its employees, but such coverage is deemed inadequate for Employer Mandate purposes, either because it is not “affordable,” does not provide at least “minimum value,” or the employer offers coverage to substantially all (but not all) of its full-time employees and one or more of its full-time employees both enrolls in Exchange coverage and receives an Exchange subsidy.

In this second scenario, the employer will owe an “inadequate coverage penalty.” The inadequate coverage penalty is $3,000 per person and is calculated, based not on the employer’s total number of full-time employees, but only on each full-time employee who receives an Exchange subsidy. The penalty is capped each month by the maximum potential “no coverage penalty” discussed above.

Because Exchange subsidies are available only to individuals with household incomes of at least 100% and up to 400% of the federal poverty line (in 2013, a maximum of $44,680 for an individual and $92,200 for a family of four), employers that pay relatively high wages may not be at risk for the penalty, even if they fail to provide coverage that satisfies the affordability and minimum value requirements.

Exchange subsidies are also not available to individuals who are eligible for Medicaid, so some employers may be partially immune to the penalty with respect to their low-wage employees, particularly in states that elect the Medicaid expansion. Medicaid eligibility is based on household income. It may be difficult for an employer to assume its low-paid employees will be eligible for Medicaid and not eligible for Exchange subsidies as an employee’s household may have more income than just the wages they collect from the employer. But for employers with low-wage workforces, examination of the extent to which the workforce is Medicaid eligible may be worth exploring.

Exchange subsidies will also not be available to any employee whose employer offers the employee affordable coverage that provides minimum value. Thus, by “playing” for employees who would otherwise be eligible for an Exchange subsidy, employers can ensure they are not subject to any penalty, even if they don’t “play” for all employees.