Page 1 of 2

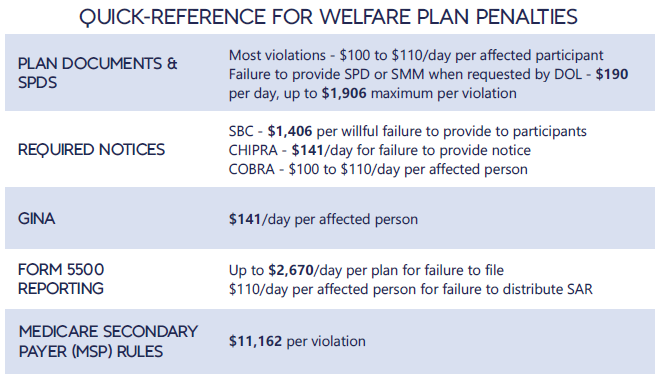

Each year in mid January, the Department of Labor (DOL) adjusts ERISA penalty amounts to account for inflation. This year’s increases are modest and amount to approximately 3%. Below summarizes a few of the penalty amounts that plan sponsors could see imposed on them for various federal law violations. The adjusted amounts apply to ERISA violations that occurred after November 2, 2015, if penalties are assessed after January 15, 2024, and before January 16, 2025.

*Notes: figures in bold are subject to annual adjustment

Below are the current inflation adjusted penalty amounts for failure to file forms 1094 and 1095 with the IRS and failure to provide form 1095 to applicable employees. Both penalties increase to $630 per form if failure is due to “intentional disregard” (criminal penalties may also apply).

In much-anticipated guidance, the Internal Revenue Service has offered its insight on the implementation of the COBRA temporary premium subsidy provisions of the American Rescue Plan Act of 2021 (ARPA) in Notice 2021-31.

Spanning more than 40 pages, the IRS-answered frequently asked questions (FAQs) finally resolve many issues relating to temporary premium assistance for COBRA continuation coverage left unanswered in the Department of Labor’s publication of model notices, election forms, and FAQs.

The practical implications of the guidance for employers are many. Significantly, employers must take action prior to May 31, 2021, to ensure compliance with some of the requirements under ARPA and related agency guidance.

Notice 2021-31 provides comprehensive guidance on the ARPA subsidy and tax credit implementation issues (although it acknowledges there are many issues that still need to be addressed). Some of the key topics addressed include:

For employers, there are some immediate takeaways:

As expected, the IRS expansively defines an “involuntary termination.” For purposes of the ARPA COBRA subsidy, involuntary terminations include employee-initiated terminations due to good reason as a result of employer action (or inaction) resulting in a material adverse change in the employment relationship.

The guidance provides helpful COVID-19-specific examples. Employees participating in severance window programs meeting specified regulatory requirements could qualify. Voluntary employee terminations due to an involuntary material reduction in hours also could qualify. Further, voluntary terminations due to daycare challenges or concerns over workplace safety may constitute an involuntary termination, but only in the narrow circumstances in which the employer’s actions or inactions materially affected the employment relationship in an adverse way, analogous to a constructive discharge.

Employer action to terminate the employment relationship due to a disability also will constitute an involuntary termination, but only if there is a reasonable expectation before the termination the employee will return to work after the end of the illness or disability. This requires a specific analysis of the surrounding facts and circumstances. The guidance notes that a disabled employee alternatively may be eligible for the subsidy based on a reduction in hours if the reduction in hours causes a loss of coverage.

A number of the circumstances that meet the involuntary termination definition in the guidance may not be coded in payroll or HRIS systems as involuntary terminations. As employers have an affirmative obligation to reach out to employees who could be AEIs, employers will need to look behind the codes to understand the circumstances of the terminations.

Further, to identify all potential AEIs, employers may need to sweep involuntary terminations or reductions in hours occurring prior to the October 1, 2019, date referenced in the Department of Labor’s FAQs. The IRS makes clear that COBRA-qualified beneficiaries who qualified for extensions of COBRA coverage due to disability (up to 29 months), a second qualifying event (up to 36 months), or an extension under state mini-COBRA potentially can qualify for the subsidy if their coverage could have covered some part of the ARPA COBRA subsidy period (April 1, 2021–September 30, 2021).

An involuntary termination is not the only event that can make an employee potentially eligible for the subsidy. Employees who lose coverage due to a reduction in hours (regardless of the reason for the reduction) can be eligible for premium assistance as well. This can include employees who have been furloughed, experienced a voluntary or involuntary reduction of hours, or took a temporary leave of absence to facilitate home schooling during the pandemic or care for a child.

The IRS explains that, if an employer subsidizes COBRA premiums for similarly situated covered employees and qualified beneficiaries who are not AEIs, the employer may not be able to claim the full ARPA tax credit. In this case, the amount of the credit the employer can receive is the premium that would have been charged to the AEI in the absence of the premium assistance and does not include any amount of subsidy the employer would otherwise have provided. For example, if a severance plan covering all regular full-time employees provides that the employer will pay 100 percent of the COBRA premium for three months following separation, this employer could not take a tax credit for the subsidy provided during this three-month period.

Notice 2021-31 does not elaborate on this issue beyond providing specific examples involving a company severance plan. Thus, ambiguity remains as to whether this guidance would prohibit an employer from claiming a tax credit where an employer has agreed to provide a COBRA subsidy in a negotiated separation or settlement agreement and not pursuant to an existing severance plan or policy. Further IRS guidance on this point may be forthcoming. In light of this guidance, employers should re-evaluate their COBRA premium subsidy strategies.

On April 7, 2021, the U.S. Department of Labor (DOL) issued eagerly anticipated guidance on administering COBRA subsidies under the American Rescue Plan Act of 2021 (ARPA). The guidance includes Frequently Asked Questions (FAQs) and various Model Notices and election forms implementing the COBRA Premium Assistance provisions under ARPA, while also announcing the launch of a page dedicated to COBRA Premium Subsidy guidance on its website.

Since ARPA was enacted, employers have been preparing to comply, albeit with many open questions. ARPA requires that full COBRA premiums be subsidized for “Assistance Eligible Individuals” for periods of coverage between April 1, 2021, through September 30, 2021. While this guidance answers important questions on the administration of the subsidies, it does not address many other details on the minds of employers. For example, this guidance does not cover important nuances such as what is an “involuntary termination” in order to qualify for subsidized coverage, how existing separation agreement commitments to subsidize COBRA should be viewed, or details on how the corresponding payroll tax credit will work.

The FAQs are largely directed to individuals and focus on how to obtain the subsidy and how subsidized coverage fits with other types of health coverage that may be available, including Marketplace, Medicaid, and individual plan coverage. We hope that employer directed guidance will follow to fill in the gaps.

Employers will be happy to know that the FAQs confirm a few points that will impact administration. First, eligibility for coverage under another group health plan, including that of a spouse’s employer, will disqualify the employee from the subsidy. Employees must certify on election forms that they are not eligible for such coverage and will notify the employer if they subsequently become eligible for coverage (individual coverage, such as through the Marketplace or Medicaid, will not disqualify an otherwise eligible individual from subsidized COBRA). Failure to do so will subject the individual to a tax penalty of $250, or if the failure is fraudulent, the greater of $250 or 110% of the premium subsidy. The availability of other coverage (which the employer may not know about) does not impact the employer’s initial obligation to identify potential Assistance Eligible Individuals and provide the required notices and election forms.

Soon after enactment, there were also questions circling about whether ARPA applied to small employer plans not subject to COBRA, but rather state “mini-COBRA” laws. The FAQs confirm that the subsidy also applies to any continuation coverage required under state mini-COBRA laws but also notes that ARPA does not change time periods for elections under State law. Further guidance would be welcome on obligations related to small insured plans. The FAQs also confirm that plans sponsored by State or local governments subject to similar continuation requirements under the Public Health Service Act are covered by the ARPA subsidies.

One area that has caused great confusion is how the right to retroactively elect COBRA coverage (to the date active coverage was lost) due to the DOL’s extended deadlines fits with this new election right. While there is more to come on this, the DOL helpfully confirmed that these are two separate rights and thankfully, the FAQs note that the extended deadlines do not apply to the 60-day notice or election periods related to the ARPA subsidies.

The most significant part of the guidance (that we knew was coming but are still happy to see sooner rather than later) are the Model Notices and election materials. The guidance package confirms that employers have until May 31, 2021, to provide the notices of the opportunity to elect subsidized coverage and individuals have 60 days following the date that notice is provided to elect subsidized coverage. Individuals can begin subsidized coverage on the date of their election, or April 1, 2021, as long as the involuntary termination or reduction in hours supporting the election right occurred before April 1, 2021. As previously noted, in no way do these timeframes extend the otherwise applicable 18-month COBRA period.

The Notices include an ARPA General Notice and COBRA Continuation Coverage Election Notice, to be provided to all individuals who will lose coverage due to any COBRA qualifying event between April 1 and September 30, 2021, and a separate Model COBRA Continuation Coverage Notice in Connection with Extended Election Periods, to be provided to anyone who may be eligible for the subsidy due to involuntary termination or reduction in hours occurring before April 1, 2021 (i.e., generally involuntary terminations or reductions in hours occurring on or after October 1, 2019).

Plans will also have to provide individuals with a Notice of Expiration of Period of Premium Assistance 15-45 days before the expiration of the subsidy — essentially explaining that subsidies will soon expire, the ability to continue unsubsidized COBRA for any period remaining under the original 18-month coverage period and describing the coverage opportunities available through other avenues such as the Marketplace or Medicaid. Employers are highly encouraged to use the DOL’s model notices without customization except where required to insert plan or employer specific information.

With the release of the model notices, employers and COBRA administrators now largely have the tools to administer this new election right. The FAQs remind us that the DOL will ensure ARPA benefits are received by eligible individuals and employers will face an excise tax for failing to comply, which can be as much as $100 per qualified beneficiary (no more than $200 per family) for each day the employer is in violation for the COBRA rules. Accordingly, employers will want to begin or continue conversations with COBRA administrators to ensure notices are timely provided to the right group of individuals.

One of Congress’s goals in the American Rescue Plan Act of 2021 (ARPA) was to provide enhanced unemployment benefits and continued healthcare coverage to employees who lose their jobs as a consequence of the COVID pandemic. The latter goal was achieved by the federal government agreeing to pick up the cost of such individuals’ COBRA coverage for up to six months beginning April 1, 2021. Individuals who voluntarily terminate their employment are not entitled to the COBRA subsidy.

Administering and communicating the new COBRA subsidy will pose challenges to employers. Here are the key features of the subsidy:

The subsidy automatically commences on April 1 for eligible individuals who are receiving COBRA coverage on that date. If a qualified beneficiary paid for COBRA coverage during the subsidy period, they must be reimbursed for such payment within 60 days after making the payment.

Employers, at their option, can elect to give qualified beneficiaries the opportunity to change their current coverage and choose different coverage as long as the cost of the new coverage does not exceed the cost of their current coverage. There is no requirement that employers provide this option to eligible individuals currently receiving COBRA coverage.

In contrast, employers must give former qualified beneficiaries who previously waived or dropped their COBRA rights but would be eligible for the subsidy if they had elected and maintained such coverage (i.e., those qualified beneficiaries who as of April 1, 2021, would still have time left in their original COBRA coverage period) the opportunity to take advantage of the subsidy. This will be an administrative challenge because it means employers will have to (i) identify such qualified beneficiaries, (ii) notify them of the availability of the subsidy, and (iii) provide a window for them to elect COBRA coverage. Unlike the current COBRA rules, which generally would require the coverage to commence retroactively to the date coverage was lost, this special election allows qualified beneficiaries to commence their coverage on April 1. The period for making this special election begins on April 1 and ends 60 days after the date the qualified beneficiary is provided the notification.

The COBRA subsidy ends before the expiration of the six-month period if the individual’s maximum COBRA coverage period ends earlier or the individual becomes eligible for other group health coverage or Medicare. Individuals receiving the COBRA subsidy must notify the plan administrator when they become eligible for other group health or Medicare coverage, and might be subject to penalties if they fail to do so. The ARPA does not explain whether eligibility for other coverage requires actual enrollment in, or mere eligibility to enroll in, other coverage.

The ARPA requires employers to update their current COBRA forms to explain the special subsidy rights and include other specified information. In addition to using the updated forms for those who become eligible for COBRA on or after April 1, the new forms have to be provided to qualified beneficiaries who became eligible for COBRA coverage before April 1 (assuming their original COBRA coverage period did not end before April 1). The Department of Labor (DOL) is required to provide model language for the election notice by April 10.

In addition, the ARPA creates a new notification requirement. Specifically, qualified beneficiaries who qualify for the subsidy must be provided a “Notice of Expiration of Period of Premium Assistance” that explains the date when their subsidy will end and certain other specified information. Generally, this new notice must be provided no more than 45 days before and no less than 15 days before the date the subsidy will end. The notice does not have to be provided to qualified beneficiaries whose subsidies end because their COBRA period ends. The DOL is required to provide a model notice for this requirement by April 25.

Penalties apply if these notices are not provided, so employers should be careful to ensure their notices are updated to include all of the required information and are distributed in a timely manner.

In sum, employers will have to develop a game plan for complying with the new COBRA subsidy. Challenges include identifying all of the eligible individuals who are entitled to the subsidy, updating COBRA forms, and providing timely notifications. Employers’ communication strategy also should take into account the extended election periods individuals have for electing COBRA coverage under prior DOL and Treasury guidance.

The COVID-19 extensions that the DOL and IRS had issued last year as part of their “Joint Notice” were set to expire at midnight on February 28th. For weeks, many have been asking the DOL and IRS for guidance on how to handle the statutorily-mandated expiration, and as a result of the lack of guidance, most plans, TPAs, insurers, and COBRA administrators had to make a judgment call as to how to proceed.

But – with 2 days to spare – DOL finally issued Disaster Relief Notice 2021-01 on February 26th.

Notice 2021-01 sets forth the DOL and IRS’ position that the COVID-19 extensions will continue past February 28th, and that all such extensions must be measured on a person-by-person basis – which was not clear from the prior guidance. Plans, TPAs, insurers, and COBRA administrators may have to reconsider their administrative practices in light of this new direction.

The original Joint Notice (85 Fed. Reg. 26351 (May 4, 2020) required that health and retirement plans toll a number of deadlines for individuals during the COVID-19 National Emergency, plus a 60-day period (the “Outbreak Period”) starting March 1, 2020.

But, as described in Footnote 4 of the Joint Notice, ERISA and the Code limit DOL and Treasury’s ability to toll deadlines to one year (“Tolling Period”).

The deadlines impacted in the Joint Notice are:

When there has been disaster relief guidance in the past, these periods have not bumped up against the statutorily-imposed one-year limit, so this COVID-19 extension is new territory – hence all the requests for the agencies to issue guidance regarding the expiration date.

In this late-breaking Notice 2021-01, DOL says it coordinated with HHS and IRS, and the agencies are interpreting the Tolling Period to be read on a person-by-person basis.

Specifically, DOL says that the Tolling Period ends the earlier of:

This means that each individual has his or her own Tolling Period!

For example, a COBRA Qualified Beneficiary (QB) has 60 days to elect COBRA, counted from the later of their loss of coverage or the date their COBRA election notice is provided. Under the Joint Notice, a QB’s 60-day deadline was tolled as of March 1, 2020, until the end of the Outbreak Period (that is, until the end of the National Emergency + 60 days).

At the end of the Outbreak Period, the deadlines would start running again, and the QB would have their normal 60-day COBRA election period (or the balance of their election period if it started before March 1, 2020).

BUT – with the 1-year expiration, DOL’s new Notice 2021-01 says that the one-year period does not end on February 28, 2021 for all individuals, but rather each individual has his/her own one-year Tolling Period.

Examples:

For all of these examples, the tolling would end earlier if the National Emergency ends. In that case, the election period would end 60 days after the end of the National Emergency.

Notice 2021-01 also says that DOL recognizes that enrollees may continue to encounter COVID issues, even after the one-year Tolling Period expiration. DOL says that the “guiding principle” is for plans to act reasonably, prudently, and in the interest of the workers and their families. DOL says that plan fiduciaries should make “reasonable accommodations to prevent the loss of or undue delay in payment of benefits . . . and should take steps to minimize the possibility of individuals losing benefits because of a failure to comply with pre-established time frames.”

Notice 2021-01 does not provide any direction regarding what would constitute a “reasonable accommodation.” It sounds like plans may need a process to consider whether to continue to waive deadlines on a case-by-case basis, but without any guidance as to what parameters to apply. And DOL suggests that failure to do so could be a fiduciary issue.

Regarding communicating these changes to enrollees, DOL says:

DOL seems to be saying that plans may need to notify each individual when his or her one-year extension is about to be up and should include information about the Health Insurance Marketplace. In addition, plans may need to update prior communications that did not anticipate this new DOL interpretation.

DOL says it acknowledges that there may be instances when plans or service providers themselves may not be able to fully and timely comply with pre-established timeframes and disclosure requirements. DOL says that where fiduciaries have acted in “good faith and with reasonable diligence under the circumstances,” DOL’s approach to enforcement will be “marked by an emphasis on compliance assistance,” including grace periods or other relief.

Days before his inauguration, President-elect Joe Biden outlined an agenda for COVID-19 relief and economic recovery that includes federal aid for health care expenses, such as providing subsidized COBRA coverage.

The relief and stimulus proposals in Biden’s $1.9 trillion American Rescue Plan package range from asking Congress for additional $1,400 checks for low- and middle-income wage earners to reimbursing employers with 500 or fewer employees for providing paid leave. Other provisions focus on helping consumers with health care expenses.

According to a Jan. 14 fact sheet from the Biden-Harris transition team, the new administration will immediately ask Congress to:

“Roughly two to three million people lost employer-sponsored health insurance between March and September, and even families who have maintained coverage may struggle to pay premiums and afford care,” according to the transition team’s fact sheet. “Together, these policies would reduce premiums for more than 10 million people and reduce the ranks of the uninsured by millions more.”

Employers may require terminated workers who choose to continue coverage under the employer-sponsored health plan for up to 18 months to pay for COBRA coverage, with premiums limited to the full cost of the coverage plus a 2 percent administration charge. That cost, however, is not affordable for many newly unemployed workers.

During the pandemic, some employers are choosing to pay for the COBRA coverage of former employees who were laid off, or to do so for current employees who lost group health plan coverage when they were furloughed or had their hours reduced.

Last April, the Department of Labor and the IRS issued regulations extending the deadlines for COBRA notices, elections and premium payments from March 1, 2020, until 60 days after the end of the ongoing COVID-19 national emergency. “While the usual statutory penalties for COBRA violations should not apply [for now], failing to notify COBRA-qualified beneficiaries of their rights may increase the likelihood of a breach of fiduciary duty claim,” Emily Meyer, an attorney with Cohen & Buckman in New York City, wrote in November.

Among other health care-related agenda items, the new administration will ask Congress to:

The fate of the health care provisions is uncertain at this time. Congressional Democrats welcomed Biden’s proposals. Rep. Steven Horsford, D-Nev., for instance, issued a statement saying he was “glad to see that the plan provides critical subsidies [for COBRA and ACA plans] to help American families access health care during this critical time.”

Republicans have criticized the extent of the new proposals, estimated to cost an addition $1.9 trillion over existing relief. Efforts by Congress “should be strategic, focusing on families and small businesses in need,” said Sen. Rick Scott, R-Fla.

Last week the Department of Health and Human Services, DOL and the IRS extended deadlines for multiple items related to health plan administration. We don’t expect a huge influx of issues from the changes. However, you should be aware so you don’t inadvertently misinform your employees.

There were changes made regarding COBRA premium payments and election timeframes but since we have addressed those in a previous post, we won’t address it here. COBRA administration is outsourced and those impacted are no longer employees so you can direct their questions to your COBRA administrator or to our office. We’ll also skip the changes made to claims and appeals as that won’t apply to everyone. That leaves the changes to your benefit program.

As you are aware, most of the carriers have reduced or even eliminated the minimum number of hours a previously full-time employee must work to be covered by your plan. Meaning, we can offer coverage to furloughed employees or those that have otherwise reduced hours to below the full-time requirements.

In addition, the agencies, have decided to disregard the Outbreak Period (the time period between March 1st and at least 60 days after the announced end of the COVID 19 National Emergency) when establishing a deadline to request enrollment in coverage for certain qualifying events. Meaning, the agencies, added a “pause” to the time frame required for employees to notify you about special enrollment periods, such as marriage or birth of a child. We are not able to determine the exact end date of the Outbreak Period yet as that is based on an end to the National Emergency (and that had yet to be determined).

For our examples, we’ll assume the COVID 19 National Emergency ends for the country on June 30th. This would make the Outbreak Period March 1st to August 29th (60 days following June 30).

Example 1 – Sally has a baby on March 3rd. Normally, she would have 30 days to notify us that she would like to add the baby. However, you are being instructed to disregard the Outbreak Period, therefore she has until September 28th (30 days from the end of the Outbreak Period) to let us know her desire to add her child.

Example 2 – Tom gets married June 1st. He will have until September 28th to let us know if he intends to enroll his spouse.

Under these examples, the dependents would be enrolled back to their original eligibility date and the employee would owe those back premiums. I don’t expect this to become a big issue, however, depending on the employees circumstances it could. The drawback to employers, other than the inconvenience, is this could have an impact on the group claims. Normally Tom and Sally would only have 30 days to enroll their dependents. With the extensions, employees have information about any issues or medical expenditures that have already happened along the way. Carriers will be responsible to back up, enroll the dependent, and pay any claims incurred.

Please let us know of any questions you have.

On April 29, 2020, the Department of Labor (DOL) and the Internal Revenue Service (IRS) announced in a Notice a “pause” in the timelines that affect many COBRA and HIPAA Special Enrollment Period timelines during the National Emergency due to the COVID-19 pandemic.

The National Emergency declaration for COVID-19 was issued on March 13, 2020, and as of the date of this writing, is still in effect. However, for purposes of COBRA in the eyes of the DOL, the “pause” date is set to begin on March 1, 2020. According to the Notice, the period from March 1 through 60 days after the date the National Emergency is declared ended is known as the “Outbreak Period.”

Normally, group health plan Qualified Beneficiaries (QBs) have 60 days from the date of a COBRA qualifying event to elect COBRA coverage, or in the case of a second COBRA qualifying event, to make a new COBRA election. Once a COBRA election is made, the first payment (going back to the date of the COBRA qualifying event) is due no more than 45 days later. After that, plan sponsors must allow at least a 30 day grace period for late COBRA payments.

According to the Notice, all of these timelines are affected. The 60-day election “clock” is paused beginning March 1, 2020 or later until the the end of the Outbreak Period. Similarly, the 45-day first payment “clock” is also paused during the Outbreak Period, as is the 30-day grace period for making COBRA payments.

Example

ABC Company’s group health plan is subject to COBRA continuation coverage. Jane Jetson and her family are covered under ABC’s group health plan. On February 1, 2020 Jane terminates employment at ABC, and on February 5th, Jane receives her COBRA election notice informing her she has 60 days from February 1st to make an election. Normally, that election period would end on April 1, 2020, 60 days from February 1st.

However, with the new DOL/IRS Notice, the “pause” button on the 60 day election period was hit on March 1st, the beginning of the Outbreak Period, so the 60 day clock stops at 29 days and doesn’t resume until the end of the Outbreak Period. For sake of this example, let’s assume the National Emergency declaration is lifted on May 31, 2020. On July 30, 2020, 60 days after May 31st and thus the end of the Outbreak Period, the “pause” button is lifted and the COBRA election clock restarts for another 31 days to complete the 60 day COBRA election period, which now would end on August 30, 2020.

Continuing with the example and assumptions, if Jane did make her COBRA election to continue coverage on August 30th (the last day to do so), the 45 day clock to make the first payments back to February 1st would begin, and she would have to make all seven months’ payments by October 14, 2020. Of course, by that date she’d also owe payments for September and October as well, although she’d be in the middle of the grace period for October.

Similarly, the 30 day HIPAA Special Enrollment Period (SEP) for qualified changes of status that impacts group health plan enrollment changes is also “paused” until after the end of the Outbreak Period.

Example

Homer Simpson also works for ABC Company, and has elected not to participate in ABC’s group health plan since he has coverage through his spouse Marge’s employer’s group health plan at XYZ Company. On March 15, 2020, Homer and Marge have a baby named Bart, and decide that Homer would like to cover his entire family under ABC’s plan. In normal times, Homer would have 30 days from the date of Bart’s birth to enroll in ABC’s group health plan utilizing the HIPAA SEP.

However, under the DOL/IRS Notice, that 30-day clock is on “pause” until the end of the Outbreak Period. Using the same assumption in the example above, that clock would start on July 30th, and Homer would have until August 30th to enroll his entire family.

Plan sponsors will need to pay close attention to this Notice and make proper adjustments in their established COBRA and HIPAA procedures to accommodate it.

Until very recently, employers were at risk of receiving steep fines if they reimbursed employees for non-employer sponsored medical care – the Affordable Care Act (ACA) included fines of up to $36,500 a year per employee for such an action. Late in 2016, however, President Obama signed the 21st Century Cures Act and established Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs). As of January 1, 2017, small employers can offer these tax-free medical care reimbursements to eligible employees.

If an employee incurs a medical care expense, such as health insurance premiums or eligible medical expenses under IRC Section 213(d), the employer can reimburse the employee up to $4,950 for single coverage or $10,000 for family coverage. Employees may not make any contributions or salary deferrals to QSEHRAs.

The maximum amount must

be prorated for those not eligible for an entire year. For example, an employer

offering the maximum reimbursement amount should only reimburse up to $2,475 to

an employee who has been working for the company for six months. For a complete

list of medical expenses covered under IRC 213(d), see https://www.irs.gov/pub/irs-pdf/p502.pdf.

Employers may tailor which expenses they will reimburse to a certain extent,

and do not have to reimburse employees for all eligible medical expenses.

Much like other healthcare reimbursement arrangements, employees may have to provide substantiation before reimbursement. The IRS has discretion to establish requirements regarding this process, but has not yet done so. Although reimbursements may be provided tax-free, they must be reported on the employee’s W-2 in Box 12 using the code “FF.”

To offer QSEHRAs, an employer cannot be an applicable large employer (ALE) under the ACA. Only employers with fewer than 50 full-time equivalent employees can offer this benefit. Further, a group cannot offer group health plans to any employees to qualify.

Typically, an employer that chooses to offer a QSEHRA must offer it to all employees who have completed at least 90 days of work. The few exceptions to this rule include part-time or seasonal employees, non-resident aliens, employees under the age of 25, and employees covered by a collective bargaining agreement.

Employers may offer differing reimbursement amounts based on employee age or family size. However, such variances must be based on the cost of premiums of a reference policy on the individual market. It is currently unclear which reference policy will be selected or how permitted discrepancies will be calculated.

To be eligible for a tax-free reimbursement, employees must have proof of minimum essential coverage. It is uncertain how closely employers will have to scrutinize such proof, although guidance will hopefully be available soon.

Eligible employees must disclose to health exchanges the amount of QSEHRA benefits available to them. The exchanges will account for the reported amount, even if the employee does not utilize it, and will likely reduce the amount of the subsidies available. Employers should take this into account before adopting a QSEHRA.

In order to establish a QSEHRA, employers will have to set up and administer a plan. Group health plan requirements, such as ACA reporting and COBRA requirements, do not apply to QSEHRAs. But in order to properly provide reimbursements to employees, employers will likely have to establish reimbursement procedures.

Additionally, any eligible employees must be notified of the arrangements in writing at least 90 days before the first day they will be eligible to participate. For the current year, the IRS is giving employers who implement QSEHRAs an extension until March 13, 2017 to provide a notice. The notice must provide the amount of the maximum benefit, and that eligible employees inform health insurance exchanges this benefit is available to them. It also must inform eligible employees they may be subject to the individual ACA penalties if they do not have minimum essential coverage.

Earlier this week, President Obama signed the 21st Century Cures Act (“Act”). This Act contains provisions for “Qualified Small Business Health Reimbursement Arrangements” (“HRA”). This new HRA would allow eligible small employers to offer a health reimbursement arrangement funded solely by the employer that would reimburse employees for qualified medical expenses including health insurance premiums.

The maximum reimbursement that can be provided under the plan is $4,950 or $10,000 if the HRA provided for family members of the employee. An employer is eligible to establish a small employer health reimbursement arrangement if that employer (i) is not subject to the employer mandate under the Affordable Care Act (i.e., less than 50 full-time employees) and (ii) does not offer a group health plan to any employees.

To be a qualified small employer HRA, the arrangement must be provided on the same terms to all eligible employees, although the Act allows benefits under the HRA to vary based on age and family-size variations in the price of an insurance policy in the relevant individual health insurance market.

Employers must report contributions to a reimbursement arrangement on their employees’ W-2 each year and notify each participant of the amount of benefit provided under the HRA each year at least 90 days before the beginning of each year.

This new provision also provides that employees that are covered by this HRA will not be eligible for subsidies for health insurance purchased under an exchange during the months that they are covered by the employer’s HRA.

Such HRAs are not considered “group health plans” for most purposes under the Code, ERISA and the Public Health Service Act and are not subject to COBRA.

This new provision also overturns guidance issued by the Internal Revenue Service and the Department of Labor that stated that these arrangements violated the Affordable Care Act insurance market reforms and were subject to a penalty for providing such arrangements.

The previous IRS and DOL guidance would still prohibit these arrangements for larger employers. The provision is effective for plan years beginning after December 31, 2016. (There was transition relief for plans offering these benefits that ends December 31, 2016 and extends the relief given in IRS Notice 2015-17.)