You did it! Your 1095 forms are ready and going out to employees. Now what?

You guessed it: Employee confusion. You’re going to get some questions. If you’re the one in charge of providing the answers, remember a great offense is the best defense. You’ll want to answer the most common questions before they’re even asked.

We’ve put together a list of some basic things

employees will want to know, along with sample answers. Tailor these Q&As as

needed for your organization. and then send them out to employees using every channel you can (mail, e-mail, employee meetings, company

website, social media, posters). Tell employees how to get more detailed

information if they need it.

1. What is this form I’m receiving?

A 1095 form is a little bit like a W-2 form.

Your employer (and/or insurer) sends one copy to the Internal Revenue Service (IRS)

and one copy to you. A W-2 form reports your annual earnings. A 1095 form

reports your health care coverage throughout the year.

2. Who is sending it to me, when, and how?

Your employer and/or health insurance company should

send one to you either by mail or in person. They may send the form to you

electronically if you gave them permission to do so. You should receive it by

March 31, 2016. (Starting in 2017, you should receive it each year by January

31, just like your W-2.)

3. Why are you sending it to me?

The 1095 forms will show that you and your

family members either did or did not have health coverage with our organization during each month of

the past year. Because of the Affordable Care Act, every person must obtain

health insurance or pay a penalty to the IRS.

4. What am I supposed to do with this form?

Keep it for your tax records. You don’t actually

need this form in order to file your taxes, but when you do file, you’ll have to tell the IRS whether or not

you had health insurance for each month of 2015. The Form 1095-B or 1095-C

shows if you had health insurance through your employer. Since you don’t

actually need this form to file your taxes, you don’t have to wait to receive

it if you already know what months you did or didn’t have health insurance in

2015. When you do get the form, keep it with your other 2015 tax information in

case you should need it in the future to help prove you had health insurance.

5. What if I get more than one 1095 form?

Someone who had health insurance through more

than one employer during the year may receive a 1095-B or 1095-C from each

employer. Some employees may receive a Form 1095-A and/or 1095-B reporting

specific health coverage details. Just keep these—you do not need to send them

in with your 2015 taxes.

6. What if I did not get a Form 1095-B or a 1095-C?

If you believe you should have received one but

did not, contact the Benefits Department by phone or e-mail at this number or

address.

7. I have more questions—who do I contact?

Please contact _____ at ____. You can also go to

our (company) website and find more detailed questions and answers. An IRS website called

Questions and Answers about Health Care Information Forms for

Individuals (Forms 1095-A, 1095-B, and 1095-C)

covers most of what you need to know.

Congress and the IRS were busy changing laws governing employee benefit plans and issuing new guidance under the ACA in late 2015. Some of the results of that year-end governmental activity include the following:

The PATH Act, enacted by Congress and signed into law on December 18, 2015, made some the following changes to federal statutory laws governing employee benefit plans:

On December 16, 2015, the IRS issued Notice 2015-87, providing guidance on employee accident and health plans and employer shared-responsibility obligations under the ACA. Guidance provided under Notice 2015-87 applies to plan years that begin after the Notice’s publication date (December 16th), but employers may rely upon the guidance provided by the Notice for periods prior to that date.

Notice 2015-87 covers a wide-range of topics from employer reporting obligations under the ACA to the application of Health Savings Account rules to rules for identifying individuals who are eligible for benefits under plans administered by the Department of Veterans Affairs. Following are some of the highlights from Notice 2015-87, with a focus on provisions that are most likely to impact non-governmental employers.

Many employers offer affordable health coverage that meets or exceeds the minimum value requirements of the Affordable Care Act (ACA). However, if one or more of their full-time employees claims the coverage offered was not affordable, minimum value health coverage, the employee could (erroneously) get subsidized coverage on the public health exchange. This would cause problems for applicable large employers (ALEs), who potentially face employer shared responsibility penalties, and for employees, which may have to repay erroneous subsidies.

If an employee does receive subsidized coverage on the public exchange, most employers would want to know about it as soon as possible and appeal the subsidy decision if they believed they were offering affordable, minimum value coverage. There are two ways employers might be notified: (1) by the federally facilitated or state-based exchange or (2) by the Internal Revenue Service (IRS).

Employer notices from exchanges

The notices from the exchanges are intended to

be an early-warning system to employers. Ideally, the exchange would notify

employers when an employee receives an advance premium tax credit (APTC) subsidizing

coverage. The notice would occur shortly after the employee started receiving

subsidized coverage, and employers would have a chance to rectify the situation

before the tax year ends.

In a set of Frequently Asked Questions issued September 18, 2015, the Center for Consumer Information and Insurance Oversight (CCIIO) stated the federal exchanges will not notify employers about 2015 APTCs and will instead begin notifying some employers in 2016 about employees’ 2016 APTCs. The federal exchange employer notification program will not be fully implemented until sometime after 2016.

In 2016, the federal exchanges will only send APTC notices to some employers and will use the employer address given to the exchange by the employee at the time of application for insurance on the exchange. CCIIO realizes some employer notices will probably not reach their intended recipients. Going forward, the public exchanges will consider alternative ways of contacting employers.

Employers that do receive the notice have 90 days after receipt to send an appeal to the health insurance exchange.

Employers that do not receive early notice from the exchanges will not be able to address potential errors until after the tax year is over, when the IRS gets involved.

Employer notices from IRS

The IRS, which is responsible for assessing and

collecting shared responsibility payments from employers, will start notifying

employers in 2016 if they are potentially subject to shared responsibility

penalties for 2015. Likewise, the IRS will notify employers in 2017 of

potential penalties for 2016, after their employees’ individual tax returns

have been processed. Employers will have an opportunity to respond to the IRS

before the IRS actually assesses any ACA shared responsibility penalties.

Regarding assessment and collection of the employer shared responsibility payment, the IRS states on its website:

An employer will not be contacted by the IRS regarding an employer shared responsibility payment until after their employees’ individual income tax returns are due for that year—which would show any claims for the premium tax credit.

If, after the employer has had an opportunity to respond to the initial IRS contact, the IRS determines that an employer is liable for a payment, the IRS will send a notice and demand for payment to the employer. That notice will instruct the employer how to make the payment.

Bottom line

For 2015, and quite possibly for 2016 and future years, the

soonest an employer will hear it has an employee who received a subsidy on the

federal exchange will be when the IRS notifies the employer that the employer

is potentially liable for a shared responsibility payment for the prior year.

The employer will have an opportunity to respond to the IRS before any

assessment or notice and demand for payment is made. The “early-warning system”

of public exchanges notifying employers of employees’ APTCs in the year in

which they receive them is not yet fully operational.

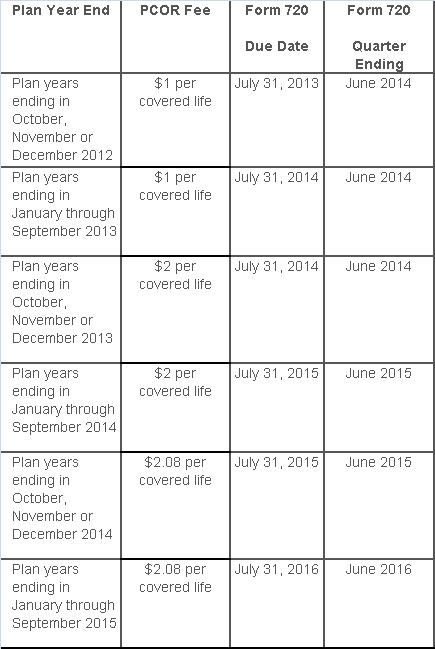

The Patient-Centered Outcomes Research Institute (PCORI) fee was established under the Affordable Care Act (ACA) to advance comparative clinical effectiveness research. The PCORI fee is assessed on issuers of health insurance policies and sponsors of self-insured health plans. The fees are calculated using the average number of lives covered under the policy or plan, and the applicable dollar amount for that policy or plan year. The past PCORI fees were—

The new adjusted PCORI fee is—

Employers and insurers will need to file Internal Revenue Service (IRS) Form 720 and pay the updated PCORI fee by July 31, 2016

Transitional Reinsurance Fee

Like the PCORI fee, the transitional reinsurance fee was established under the ACA. It was designed to reinsure the marketplace exchanges. Contributing entities are required to make contributions towards these reinsurance payments. A “contributing entity” is defined as an insurer or third-party administrator on behalf of a self-insured group health plan. The past transitional reinsurance fees were

The new adjusted transition reinsurance fee is—

The Affordable Care Act (“ACA”), introduced in 2014 the Transitional Reinsurance Fee (“Fee”) in an effort to fund reinsurance payments to health insurance issuers that cover high-risk individuals in the individual market and to stabilize insurance premiums in the market for the 2014 through 2016 years. The Fee has also been instituted to pay administrative costs related to the Early Retiree Reinsurance Program.

BACKGROUND ON TRANSITIONAL REINSURANCE PROGRAM

The ACA established a transitional reinsurance program to provide payments to health insurance issuers that cover high risk individuals in an attempt to evenly spread the financial risk of issuers. The program is designed to provide issuers with greater payment stability as insurance market reforms are implemented and the state-based health insurance exchanges/marketplaces facilitate increased enrollment. It is expected that the program will reduce the uncertainty of insurance risk in the individual market by partially offsetting issuers’ risk associated with high-cost enrollees. In an effort to fund the program, the ACA created the Fee which is a temporary fee that is assessed on health insurance issuers and plan sponsors of self-funded health plans. The Fee is applicable for the 2014, 2015 and 2016 years and is deductible as an ordinary and necessary business expense.

The Fee is generally applicable to all health insurance plans providing major medical coverage including sponsors of self-insured group health plans. Major medical coverage is defined as health coverage for a broad range of services and treatments, including diagnostic and preventive services, as well as medical and surgical conditions in inpatient, outpatient and emergency room settings. Since COBRA continuation coverage generally qualifies as major medical coverage, the Fee will also apply in this instance. It does not, however, apply to employer provided major medical coverage that is secondary to Medicare.

The Fee, as currently structured, does not apply to various other types of plans including (but not limited to) health savings accounts (H.S.A.s), employee assistance plans (EAP) or wellness programs that do not provide major medical coverage, health reimbursement arrangements integrated with a group health plan (HRA), health flexible spending accounts (FSA) and coverage that consists of only excepted benefits (e.g. stand-alone dental and vision).

AMOUNT OF THE FEE

The Fee for the 2015 benefit year is equal to $44 per covered life. It is expected that the Fee for the 2015 benefit year will generate approximately $8 billion in revenue. The Fee for the 2016 year is expected to be $27 per covered life and will raise approximately $5 billion in revenue. Thereafter, the Fee is set to expire and no longer be applicable. The fee for 2014 was $63 per covered life.

REPORTING THE NUMBER OF COVERED LIVES AND PAYING THE FEE

The 2015 ACA Transitional Reinsurance Program Annual Enrollment and Contributions Submission Form will be available on www.pay.gov on October 1, 2015. The form for 2014 is also available on this website. Please note there is a separate form for each benefit year. For the 2015 year, the number of covered lives must be reported to the Department no later than November 16, 2015. The Department will then notify reporting organizations no later than December 15, 2015 the amount of the fee that will be due and payable.

As with the 2014 benefit year, the Department of Health and Human Services has given contributing entities two different options to make the payment. Under the first option, the first portion of the Fee ($33 per covered life) is due and payable no later than January 15, 2016 (30 days after issuance of the notice from the Department). This portion of the Fee will cover reinsurance payments and administrative expenses. The second portion of the Fee ($11 per covered life) will cover Treasury’s administrative costs associated with the Early Retiree Reinsurance Program and will be due no later than November 15, 2016.

Under the second payment option, contributing entities can opt to pay the full amount ($44 per covered life) by January 15, 2016.

As the number of covered lives is due to be reported no later than November 16th of this year, employers should review their types of health coverage and determine which plans are subject to the Fee. Employers that have fully insured plans should be on the lookout for potential increased premiums as the insurance carrier is responsible to report and pay the Fee on behalf of the plan in these instances. Those with self funded medical coverage need to be sure to report and pay the fe

The Affordable Care Act added a patient-centered outcomes research (PCOR) fee on health plans to support clinical effectiveness research. The PCOR fee applies to plan years ending on or after Oct. 1, 2012, and before Oct. 1, 2019. The PCOR fee is due by July 31 of the calendar year following the close of the plan year. For plan years ending in 2014, the fee is due by July 31, 2015.

PCOR fees are required to be reported annually on Form 720, Quarterly Federal Excise Tax Return, for the second quarter of the calendar year. The due date of the return is July 31. Plan sponsors and insurers subject to PCOR fees but not other types of excise taxes should file Form 720 only for the second quarter, and no filings are needed for the other quarters. The PCOR fee can be paid electronically or mailed to the IRS with the Form 720 using a Form 720-V payment voucher for the second quarter. According to the IRS, the fee is tax-deductible as a business expense.

The PCOR fee is assessed based on the number of employees, spouses and dependents that are covered by the plan. The fee is $1 per covered life for plan years ending before Oct. 1, 2013, and $2 per covered life thereafter, subject to adjustment by the government. For plan years ending between Oct. 1, 2014, and Sept. 30, 2015, the fee is $2.08. The Form 720 instructions are expected to be updated soon to reflect this increased fee.

This chart summarizes the fee schedule based on the plan year end and shows the Form 720 due date. It also contains the quarter ending date that should be reported on the first page of the Form 720 (month and year only per IRS instructions). The plan year end date is not reported on the Form 720.

For insured plans, the insurance company is responsible for filing Form 720 and paying the PCOR fee. Therefore, employers with only fully- insured health plans have no filing requirement.

If an employer sponsors a self-insured health plan, the employer must file Form 720 and pay the PCOR fee. For self-insured plans with multiple employers, the named plan sponsor is generally required to file Form 720. A self-insured health plan is any plan providing accident or health coverage if any portion of such coverage is provided other than through an insurance policy.

Since the fee is a tax assessed against the plan sponsor and not the plan, most funded plans subject to ERISA must not pay the fee using plan assets since doing so would be considered a prohibited transaction by the U.S. Department of Labor (DOL). The DOL has provided some limited exceptions to this rule for plans with multiple employers if the plan sponsor exists solely for the purpose of sponsoring and administering the plan and has no source of funding independent of plan assets.

Plans sponsored by all types of employers, including tax-exempt organizations and governmental entities, are subject to the PCOR fee. Most health plans, including major medical plans, prescription drug plans and retiree-only plans, are subject to the PCOR fee, regardless of the number of plan participants. The special rules that apply to Health Reimbursement Accounts (HRAs) and Health Flexible Spending Accounts (FSAs) are discussed below.

Plans exempt from the fee include:

If a plan sponsor maintains more than one self-insured plan, the plans can be treated as a single plan if they have the same plan year. For example, if an employer has a self-insured medical plan and a separate self-insured prescription drug plan with the same plan year, each employee, spouse and dependent covered under both plans is only counted once for purposes of the PCOR fee.

The IRS has created a helpful chart showing how the PCOR fee applies to common types of health plans.

Health Reimbursement Accounts (HRAs) - Nearly all HRAs are subject to the PCOR fee because they do not meet the conditions for exemption. An HRA will be exempt from the PCOR fee if it provides benefits only for dental or vision expenses, or it meets the following three conditions:

Health Flexible Spending Accounts (FSAs) - A health FSA is exempt from the PCOR fee if it satisfies an availability condition and a maximum benefit condition.

Additional special rules for HRAs and FSAs . Once an employer determines that its HRA or FSA is subject to the PCOR fee, the employer should consider the following special rules:

The IRS provides different rules for determining the average number of covered lives (i.e., employees, spouses and dependents) under insured plans versus self-insured plans. The same method must be used consistently for the duration of any policy or plan year. However, the insurer or sponsor is not required to use the same method from one year to the next.

A plan sponsor of a self-insured plan may use any of the following three

methods to determine the number of covered lives for a plan year:

1. Actual count method. Count the covered lives on each day of the plan year and divide by the number of days in the plan year.

Example: An employer has 900 covered lives on Jan. 1, 901 on Jan. 2, 890 on

Jan. 3, etc., and the sum of the lives covered under the plan on each day of

the plan year is 328,500. The average number of covered lives is 900 (328,500 ÷

365 days).

2. Snapshot method. Count the covered lives on a single day in each quarter (or more than one day) and divide the total by the number of dates on which a count was made. The date or dates must be consistent for each quarter. For example, if the last day of the first quarter is chosen, then the last day of the second, third and fourth quarters should be used as well.

Example: An employer has 900 covered lives on Jan. 15, 910 on April 15, 890 on

July 15, and 880 on Oct. 15. The average number of covered lives is 895 [(900 +

910+ 890+ 880) ÷ 4 days].

As an alternative to counting actual lives, an employer can count the number of

employees with self-only coverage on the designated dates, plus the number of

employees with other than self-only coverage multiplied by 2.35.

3. Form 5500 method. If a Form 5500 for a plan is filed before the due date of the Form 720 for that year, the plan sponsor can determine the number of covered lives based on the Form 5500. If the plan offers just self-only coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) and divides by 2. If the plan also offers family or dependent coverage, the plan sponsor adds the participant counts at the beginning and end of the year (lines 5 and 6d on Form 5500) without dividing by 2.

Example: An employer offers single and family coverage with a plan year ending

on Dec. 31. The 2013 Form 5500 is filed on June 5, 2014, and reports 132

participants on line 5 and 148 participants on line 6d. The number of covered

lives is 280 (132 + 148).

To evaluate liability for PCOR fees, plan sponsors should identify all of their plans that provide medical benefits and determine if each plan is insured or self-insured. If any plan is self-insured, the plan sponsor should take the following actions:

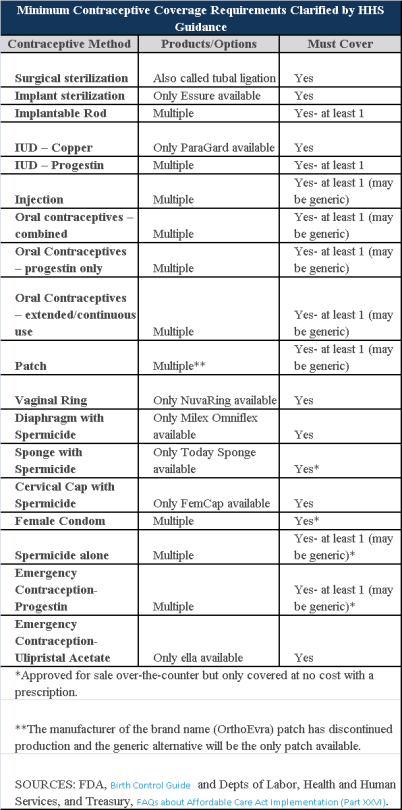

Plans and insurers must cover all 18 contraception methods approved by the U.S. Food and Drug Administration, according to a new set of questions and answers on the Affordable Care Act’s preventive care coverage requirements.

“Reasonable medical management” still may be used to steer members to specific products within those methods of contraception. A plan or insurer may impose cost-sharing on non-preferred items within a given method, as long as at least one form of contraception in each method is covered without cost-sharing.

However, an individual’s physician must be allowed to override the plan’s drug management techniques if the physician finds it medically necessary to cover without cost-sharing an item that a given plan or insurer has classified as non-preferred, according to one of the frequently asked questions from the U.S. Departments of Labor, Health and Human Services and the Treasury.

The ACA mandated all plans and insurers to cover preventive care items, as defined by the Public Health Service Act, without cost-sharing. Eighteen forms of female contraception are included under the preventive care list. The individual FAQs on contraception clarified the following requirements.

The FAQ comes just weeks after reports and news coverage detailed health plan violations of the women coverage provisions of the ACA.

Testing and Dependent Care Answers

In questions separate from contraception, plans and insurers were told they must cover breast cancer susceptibility (BRCA-1 or BRCA-2) testing without cost-sharing. The test identifies whether the woman has genetic mutations that make her more susceptible to BRCA-related breast cancer.

Another question stated that if colonoscopies are performed as preventive screening without cost-sharing, then plans could not impose cost-sharing on the anesthesia component of that service.

During this year, businesses will be hearing a lot about the Affordable Care Act’s (ACA’s) information reporting requirements under Code Sections 6055 and 6056. Information gathering will be critical to successful reporting, and there is one aspect of that information gathering which employers might want to take action on sooner rather than later – collecting Social Security numbers (SSNs), particularly when required to do so from the spouses and dependents of their employees. There are, of course, ACA implications for not taking this step, as well as data privacy and security risks for employer and their vendors.

Under the ACA, providers of “minimum essential coverage” (MEC) must report certain information about that coverage to the Internal Revenue Service (IRS), as well as to persons receiving that MEC. Employers that sponsor self-insured group health plans are providers of MEC for this purpose, and in the course of meeting the reporting requirements, must collect and report SSNs to the IRS. However, this reporting mandate requires those employers (or vendors acting on their behalf) to transmit to the IRS the SSNs of employee and their spouses and dependents covered under the plan, unless the employers either (i) exhaust reasonable collection efforts described below, (ii) or meet certain requirements for limited reporting overall.

Obviously, employers are familiar with collecting, using and disclosing employee SSNs for legitimate business and benefit plan purposes. Collecting SSNs from spouses and dependents will be an increased burden, creating more risk on employers given the increased amount of sensitive data they will be handling, and possibly from vendors working on their behalf. The reporting rules permit an employer to use a dependent’s date of birth, only if the employer was not able to obtain the SSN after “reasonable efforts.” For this purpose, reasonable efforts means the employer was not able to obtain the SSN after an initial attempt, and two subsequent attempts.

From an ACA standpoint, employers with self-insured plans that have not collected this information should be engaged in these efforts during the year (2015) to ensure they are ready either to report the SSNs, or the DOBs. At the same time, collecting more sensitive information about individuals raises data privacy and security risks for an organization regarding the likelihood and scope of a breach. Some of those risks, and steps employers could take to mitigate those risks, are described below.

Employers navigating through ACA compliance and reporting requirements have many issues to be considered. How personal information or protected health information is safeguarded in the course of those efforts is one more important consideration.

The IRS and the Treasury Department issued a notice on the so-called “Cadillac Tax”—a 40 percent excise tax to be imposed on high-cost employer-sponsored health plans beginning in 2018 under the Affordable Care Act (ACA).

Notice 2015-16, released on Feb. 23, 2015, discusses a number of issues concerning the tax and requests comments on the possible approaches that ultimately could be incorporated in proposed regulations. Specifically, the guidance states that the agencies anticipate that pretax salary reduction contributions made by employees to health savings accounts (HSAs) will be subject to the Cadillac tax.

Background

In 2018, the ACA provides that a nondeductible 40 percent excise tax be imposed on “applicable employer-sponsored coverage” in excess of statutory thresholds (in 2018, $10,200 for self-only, $27,500 for family). As 2018 approaches, the benefit community has long awaited guidance on this tax. While many employers have actively managed their plan offerings and costs in anticipation of the impact of the tax, those efforts have been hampered by the lack of guidance. Among other things, employers are uncertain what health coverage is subject to the tax and how the tax is calculated.

Particularly, Notice 2015-16 addresses:

The agencies are requesting comments on issues

discussed in this notice by May 15, 2015. They intend to issue another notice

that will address other areas of the excise tax and anticipates issuing

proposed regulations after considering public comments on both notices.

Applicable Coverage

Of most immediate interest to plan sponsors is the specific type of coverage (i.e., “applicable coverage”) that will be subject to the excise tax, particularly where the statute is unclear.

Employee Pretax HSA

Contributions

The ACA statute provides that employer contributions to an HSA are subject to

the excise tax, but did not specifically address the treatment of employee

pretax HSA contributions. The notice says that the agencies “anticipate that

future proposed regulations will provide that (1) employer contributions to

HSAs, including salary reduction contributions to HSAs, are included in

applicable coverage, and (2) employee after-tax contributions to HSAs are

excluded from applicable coverage.”

Note: This anticipated treatment of employee pretax contributions to HSAs will have a significant impact on HSA programs. If implemented as the agencies anticipate, it could mean many employer plans that provide for HSA contributions will be subject to the excise tax as early as 2018, unless the employer limits the amount an employee can contribute on a pretax basis.

Self-Insured Dental

and Vision Plans

The ACA statutory language specifically excludes fully insured dental and

vision plans from the excise tax. The treatment of self-insured dental and

vision plans was not clear. The notice states that the agencies will consider

exercising their “regulatory authority” to exclude self-insured plans that

qualify as excepted benefits from the excise tax.

Employee Assistance

Programs

The agencies are also considering whether to exclude excepted-benefit employee

assistance programs (EAPs) from the excise tax.

Onsite Medical Clinics

The notice discusses the exclusion of certain onsite medical clinics that offer

only de

minimis care to employees,

citing a provision in the COBRA regulations, and anticipates excluding such

clinics from applicable coverage. Under the COBRA regulations an onsite clinic

is not considered a group health plan if:

The agencies are also asking for comment on

the treatment of clinics that provide certain services in addition to first

aid:

In Closing

With the release of this initial guidance, plan sponsors can gain some insight into the direction the government is likely to take in proposed regulations and can better address potential plan design strategie

Even small employers notsubject to the Affordable Care Act’s (ACA) coverage mandate can’t reimburse employees for nongroup health insurance coverage purchased on a public exchange, the Internal Revenue Service confirmed. But small employers providing premium reimbursement in 2014 are being offered transition relief through mid-2015.

IRS Notice 2015-17, issued on Feb. 18, 2015, is another in a series of guidance from the IRS reminding employers that they will run afoul of the ACA if they use health reimbursement arrangements (HRAs) or other employer payment plans—whether with pretax or post-tax dollars—to reimburse employees for individual policy premiums, including policies available on ACA federal or state public exchanges.

This time the warning is aimed at small employers—those with fewer than 50 full-time employees or equivalent workers. While small organizations are not subject to the ACA’s “shared responsibility” employer mandate to provide coverage or pay a penalty (aka Pay or Play), if they do provide health coverage it must meet a range of ACA coverage requirements.

“The agencies have taken the position that employer payment plans are group health plans, and thus must comply with the ACA’s market reforms,” noted Timothy Jost, J.D., a professor at the Washington and Lee University School of Law, in a Feb. 19 post on the Health Affairs Blog. “A group health plan must under these reforms cover at least preventive care and may not have annual dollar limits. A premium payment-only HRA or other payment arrangement that simply pays employee premiums does not comply with these requirements. An employer that offers such an arrangement, therefore, is subject to a fine of $100 per employee per day. (An HRA integrated into a group health plan that, for example, helps with covering cost-sharing is not a problem).”

Transition Relief

The notice provides transition relief for small employers that used premium payment arrangements for 2014. Small employers also will not be subject to penalties for providing payment arrangements for Jan. 1 through June 30, 2015. These employers must end their premium reimbursement plans by that time. This relief does not extend to stand-alone HRAs or other arrangements used to reimburse employees for medical expenses other than insurance premiums.

No similar relief was given for large employers (those with 50 or more full-time employees or equivalents) for the $100 per day per employee penalties. Large employers are required to self-report their violation on the IRS’s excise tax form 8928 with their quarterly filings.

“Notice 2015-17 recognizes that impermissible premium-reimbursement arrangements have been relatively common, particularly in the small-employer market,” states a benefits brief from law firm Spencer Fane. “And although the ACA created “SHOP Marketplaces” as a place for small employers to purchase affordable [group] health insurance, the notice concedes that the SHOPs have been slow to get off the ground. Hence, this transition relief.”

Subchapter S Corps.

The notice states that Subchapter S closely held corporations may pay for or reimburse individual plan premiums for employee-shareholders who own at least 2 percent of the corporation. “In this situation, the payment is included in income, but the 2-percent shareholder can deduct the premiums for tax purposes,” Jost explained. The 2-percent shareholder may also be eligible for premium tax credits through the marketplace SHOP Marketplace if he or she meets other eligibility requirements.

Tricare

Employers can pay for some or all of the expenses of employees covered by Tricare—a Department of Defense program that provides civilian health benefits for military personnel (including some members of the reserves), military retirees and their dependents—if the payment plan is integrated with a group health plan that meets ACA coverage requirements.

Higher Pay Is Still OK

One option that the IRS will allow employers is to simply increase an employee’s taxable wages in lieu of offering health insurance. “As long as the money is not specifically designated for premiums, this would not be a premium payment plan,” said Jost. “The employer could even give the employee general information about the marketplace and the availability of premium tax credits as long as it does not direct the employee to a specific plan.”

But if the employer pays or reimburses premiums specifically, “even if the payments are made on an after-tax basis, the arrangement is a noncompliant group health plan and the employer that offers it is subject to the $100 per day per employee penalty,” Jost warned.

“Small employers now have just over four months in which to wind down any impermissible premium-reimbursement arrangement,” the Spencer Fane brief notes. “In its place, they may wish to adopt a plan through a SHOP Marketplace. Although individuals may enroll through a Marketplace during only annual or special enrollment periods, there is no such limitation on an employer’s ability to adopt a plan through a SHOP.”

{kind=link}

{kind=link}